Download

1 / 3

30 likes | 48 Views

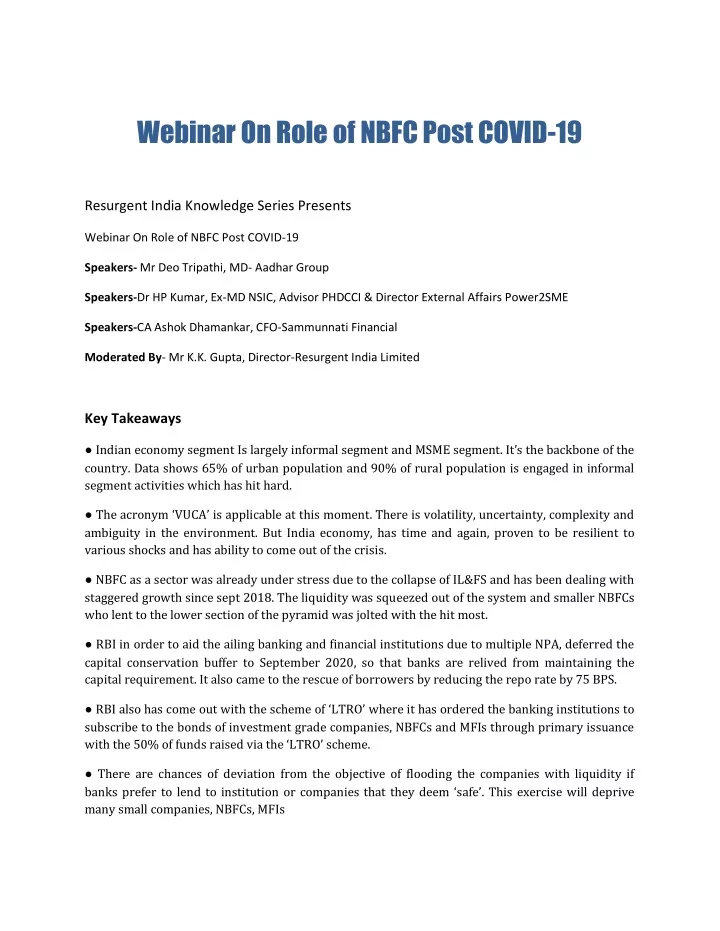

Indian economy segment Is largely informal segment and MSME segment. Itu2019s the backbone of the country. Data shows 65% of urban population and 90% of rural population is engaged in informal segment activities which has hit hard.

E N D

Webinar On Role of NBFC Post COVID-19 Resurgent India Knowledge Series Presents Webinar On Role of NBFC Post COVID-19 Speakers- Mr Deo Tripathi, MD- Aadhar Group Speakers-Dr HP Kumar, Ex-MD NSIC, Advisor PHDCCI & Director External Affairs Power2SME Speakers-CA Ashok Dhamankar, CFO-Sammunnati Financial Moderated By- Mr K.K. Gupta, Director-Resurgent India Limited Key Takeaways ●Indian economy segment Is largely informal segment and MSME segment. It’s the backbone of the country. Data shows 65% of urban population and 90% of rural population is engaged in informal segment activities which has hit hard. ●The acronym ‘VUCA’ is applicable at this moment. There is volatility, uncertainty, complexity and ambiguity in the environment. But India economy, has time and again, proven to be resilient to various shocks and has ability to come out of the crisis. ● NBFC as a sector was already under stress due to the collapse of IL&FS and has been dealing with staggered growth since sept 2018. The liquidity was squeezed out of the system and smaller NBFCs who lent to the lower section of the pyramid was jolted with the hit most. ● RBI in order to aid the ailing banking and financial institutions due to multiple NPA, deferred the capital conservation buffer to September 2020, so that banks are relived from maintaining the capital requirement. It also came to the rescue of borrowers by reducing the repo rate by 75 BPS. ●RBI also has come out with the scheme of ‘LTRO’ where it has ordered the banking institutions to subscribe to the bonds of investment grade companies, NBFCs and MFIs through primary issuance with the 50% of funds raised via the ‘LTRO’ scheme. ● There are chances of deviation from the objective of flooding the companies with liquidity if banks prefer to lend to institution or companies that they deem ‘safe’. This exercise will deprive many small companies, NBFCs, MFIs

Webinar On Role of NBFC Post COVID-19 ● RBI, under its circular on 27th March, clearly quoted that all banks, MFIs, HFCs and NBFCs, are mandated by default to grant 3 months moratorium, and its interpreted that status of accounts under bucket 2 will be determined after this period of 3 months. But there has been ambiguity in regards to the interpretation circling within the industries which RBI yet to has clarify and address. ● NBFCs have been playing an important role as financier and intermediary by extending limits to MSMEs. The success rate of the NBFCs in the country has been commendable. ● For NBFCs to perform their role efficiently, banks have to be liberal in extending loans and RBI should come out providing details on the clarity of the said circular. ● In the past two years, total of 175 BPS has been reduced by the RBI which has not been effectively passed down to the borrowers. We expect that this further reduction will be passed down to industry, commerce and NBFCs too.

● SIDBI has exposure of around 25.2 lakh to MSME sector, which is about 99% of country’s entire industrial sector. RBI has to consider providing the concessions expected by the MSME sector. ● Earlier assistance to MSME sector through NBFC was classified as priority sector which was later withdrawn. Just recently it had been restated again to classify lending up to Rs 20 lakh to MSME as priority lending ● Majority of the NBFCs have been facing the brunt of increase in lending rates by banks due to their reservations about the sector. Banks pass down the lowering of interest rates to individuals but not to the NBFCs. Logically, institutional NBFCs are more secured than individual customers. But the concept in the past 1.5 years has reversed. ● Banks inhouse HFCs lend at 7.5% but lend at higher rate to other HFCs. It becomes difficult for those HFCs to lend at any rate lower than 11% due to operational cost to the informal customers. ● There are no as such insurance cover for NBFC if creditor defaults, but there are two schemes by the GoI ,Credit guarantee fund trust for small loans and credit guarantee fund trust for low income house, whereby in the event of default GoI will cover 50-80% of the sanctioned amount. This facility is available to member lending institutions. This facility is although unable to availed by most of the NBFC due to strict closures. ● NBFC has to adjust their software to reflect the new extended, restructured repayment schedule. There has to be clarification whether the restructuring has to happen in entirety or the installments have to be shifted by 3 months. NPA schedules also have to be worked out internally. ● SEBI likely has allowed unlisted NCDs and CPs to be treated as ‘term loans’ and get protection umbrella under RBI circular. ►Watch the webinar here :https://www.youtube.com/watch?v=-zEBwx04iA4