Download

1 / 20

200 likes | 337 Views

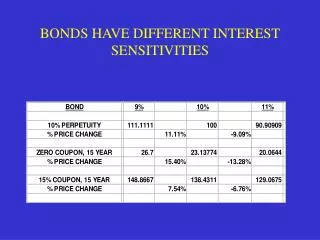

BONDS HAVE DIFFERENT INTEREST SENSITIVITIES. BOND PRICE-YIELD RELATIONSHIP. MEASURES OF INTEREST SENSITIVITY. Price Value of a Basis Point (PVBP) Change in bond price given a one basis point change in yield Yield Value of a 32nd (YV32) Change in yield given a price change of 1/32 Duration

E N D

MEASURES OF INTEREST SENSITIVITY • Price Value of a Basis Point (PVBP) Change in bond price given a one basis point change in yield • Yield Value of a 32nd (YV32) Change in yield given a price change of 1/32 • Duration Macaulay: Price elasticity w.r.t. (1+y/2) Modified: % price change given yield change

PROPERTIES OF DURATION • DURATION: • Decreases with coupon rate • Decreases with yield • Usually increases maturity (but watch out for long-term deep discount bonds)

MODIFIED DURATION • Used more in practice because of easier interpretation • Calculate as shown, using closed form solution for DMAC or use built-in Excel function

CALCULATING DURATION • A. Program Closed-Form Solution into a spreadsheet • B. Use Excel functions DURATION and MDURATION (in Analysis ToolPak) • C. Approximate: DMOD (P- - P+)/[2(P0)(y)]

APPLICATION: HEDGING • For our portfolio, given a change in yield, P/P - DMOD(p) y • To hedge the portfolio against yield changes, set DMOD(p) = 0 • This implies: WA = - WB [DMOD(A)/ DMOD(B)]

APPROXIMATING BOND PRICE CHANGES • But what if P/P - DMOD(p) y isn’t a very good approximation? • A better approximation comes from carrying the Taylor’s Series one more term:

WHAT DOES CONVEXITY MEASURE? • Note that convexity is a second derivative measure • It tells us about the degree of curvature in the price-yield relationship

APPROXIMATING CONVEXITY A closed form solution exists, but convexity can be approximated quite accurately by measuring the change in the change in price, given a change in yield (including between coupon dates)

CONVEXITY PROPERTIES • As yield increases, convexity decreases • For a given yield and maturity, as coupon rate increases, convexity decreases • e.g., zeros have greatest convexity among bonds of given yield and maturity • For a given yield and modified duration, as coupon rate increases, convexity increases • e.g., zeros have least convexity among bonds of given yield and DMOD

IMMUNIZATION CAVEATS • The immunization technique protects us only against a small, one-time shift in rates • need to rebalance after yield shifts occur • For portfolios, immunization only works for parallel yield curve shifts • in fact, the yield curve often flattens or steepens • Why not just use zeros to immunize?