Download

1 / 12

0 likes | 4 Views

Term insurance and SIP (Systematic Investment Plan) are distinct financial tools serving different purposes. Term insurance is a pure risk protection plan that provides financial security to your family in case of your untimely demise. SIP, on the other hand, is an investment method in mutual funds, allowing wealth accumulation over time through regular contributions. While term insurance ensures financial protection, SIP focuses on disciplined investment and growth for future goals.

E N D

Introduction There's financial planning and securing a future that's stable, and one hears the conversation with two quite common tools—the term insurance and SIPs. These two are absolutely invaluable, yet they serve a totally different purpose. Understanding the same financial products in Canada has helped make people informed about their decisions so they fit well into their financial goals. This blog delves deep into the crux of comparison, advantages, and scenarios in which each of them makes sense, with more emphasis on when they make the most sense for Ontario and Canada investors in Term Life Insurance Investments.

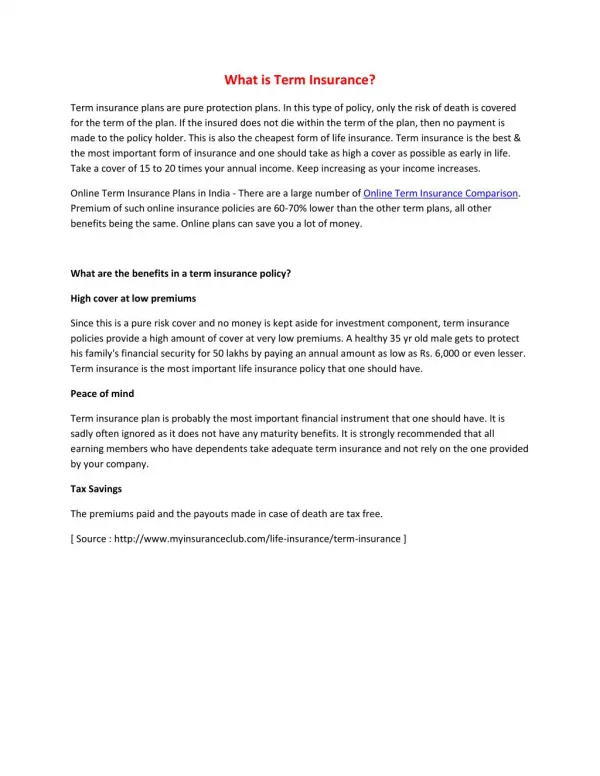

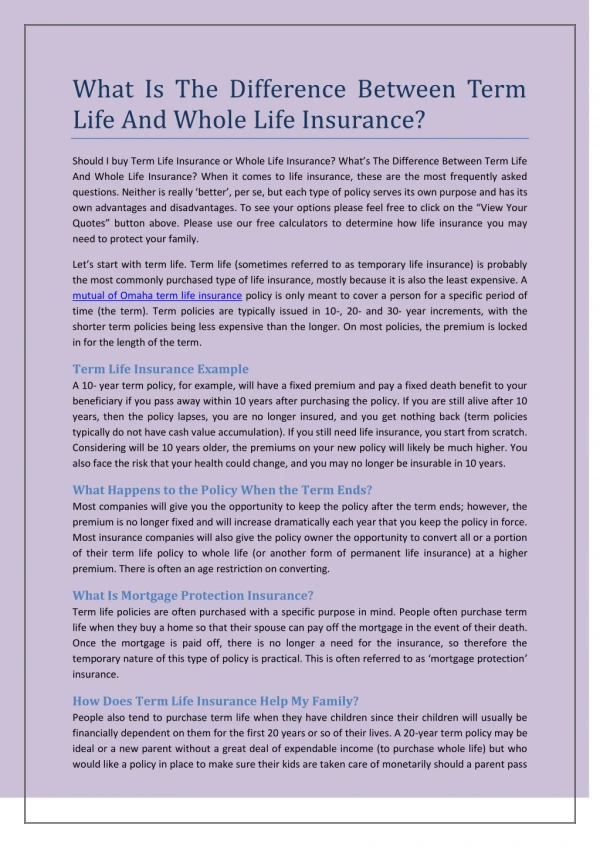

What is Term Insurance? Term insurance is one of the most common life insurance products that pays out in case the policyholder dies within a given term. When the policyholder dies during the term, the death benefit goes to the beneficiary. It is one of the easiest ways of securing your loved ones' financial future, as it is relatively inexpensive. Key Features of Term Insurance • Affordably premium priced: Term Life Insurance policies are not as expensive as Permanent Life Insurance Policies. • Pure Risk Coverage: Pure risk coverage is a pure coverage product purely involving financial risks, without the elements of saving or investment. • Flexible Terms: The policies can be taken for a variety of periods, for instance, 10, 20, or 30 years. • No Maturity Benefit on Survival: If the policyholder survives the term, there is no maturity benefit. Relevance in Canada In Ontario, it is more often for younger families along with any single person or groups of people who can look forward to receiving effective financial coverage at low-cost means and terms of life.

What is a Systematic Investment Plan (SIP)? SIP refers to a type of investment in mutual funds by which a fixed amount is invested at regular intervals. SIPs assist investors in creating wealth over time through disciplined and consistent investments. Key Features of SIPs • Investment Growth: SIPs allow your money to grow with the market over time. • Flexibility: You can decide how often and how much you invest. • Compounding Benefits: Consistent Term Life Insurance Investments accrue greater returns through the compounding power. • Market Risks: Returns are tied to market risks and vary with the performance of funds. Relevance in Canada People in Canada generally choose SIPs for financial goals like retirement savings, education, and wealth. When such long-term savings accounts are combined with tax benefits through accounts like RRSPs and TFSAs, the investment SIPs become even stronger.

When to Choose Term Insurance This policy best fits a situation in which the purpose of financial protection is to be served. Some common circumstances that drive Term Life Insurance Agents to endorse Term Life Insurance include: • Income Replacement: Term insurance will definitely ensure that the income which was mainly reliant on you is not hindered in the event of you being absent. • Debt Coverage: It can pay off mortgages, car loans, or other debts so that your loved ones aren't burdened. • Cost-Effectiveness: If it's a case of finding an affordable policy, then Term Life Insurance in Ontario, Canada, is cost-effective. • Temporary needs: If one wants to cover him or herself for a certain number of years, say, till the children are economically independent, then term insurance is quite ideal.

When to Choose SIPs SIPs are perfect for those people who save or invest to garner money or accomplish a specific financial goal. Here are a few instances where SIPs work well: • Retirement Planning: Retirement Planning Retirement Planning Long-term SIPs kept in registered accounts, such as RRSP, grow significantly over a period of time. • Education Savings: SIPs can be done to save for the education of your children. • Wealth Accumulation: SIPs are attractive to investors seeking market-linked returns. • Disciplined Investment: An SIP encourages regular contributions and helps in forming a habit of savings and investment.

Term Insurance Investments: Can They Work Together? Term insurance and SIPs can complement each other in a complete financial plan. The following are how: • Protection Plus Growth: It gives protection plus growth. SIPs help increase wealth over time, but term insurance is for financial protection. • Balancing risk: There is a market risk associated with SIPs. The balance in this portfolio is maintained through guaranteed term insurance. • Financial Goals: Pay term insurance against liabilities and SIPs to save towards long-term goals such as retirement or education savings.

Term Insurance in Ontario, Canada In Ontario, Term Life Insurance ranges with options available for the different needs of the people residing there. In Ontario, many agents maintain that their Term Life Insurance policies are inexpensive and versatile enough to be utilized by an individual or family. Key Features of Term Life Insurance in Ontario • Reasonably priced premiums: premium is reasonably priced, yet competitive enough to be affordable for most individuals. • Customizable coverage: coverage that can be changed according to requirements. • Local Expertise: Agents provide advice specific to Ontario's local financial environment. What About Permanent Life Insurance Policies? The cheapest type is term insurance, but permanent life insurance covers life and offers a savings feature. Permanent Life Insurance Quotes are more expensive because of the added benefits, including protection and cash value accumulation.

Making the Right Choice Depending upon the financial objective, the option of term insurance, SIP, or even Permanent Life Insurance Policies is to be exercised. It may be simplified thus: • Choose Term Insurance If: You want low-cost financial protection for a definite term. • Invest in SIPs If: Your focus is on wealth creation over the long term with market-sensitive investments. • Choose Permanent Life Insurance If: You desire lifetime coverage that includes a savings component, and you are willing to pay more.

Final Thoughts When you understand how term insurance is different from SIPs, then the creation of a balance can be done for your financial planning. Term insurance meets the short-term needs of your family's financial security, while SIPs ensure investment in the right long-term order. More particularly, for a Canadian and Ontarian, the shape of many choices is that investments in Term Life Insurance, SIPs, and permanent life insurance will work according to varied requirements. So, know your financial status, get in touch with the experts, and use tools according to what best fits your plan.