Download

1 / 4

40 likes | 75 Views

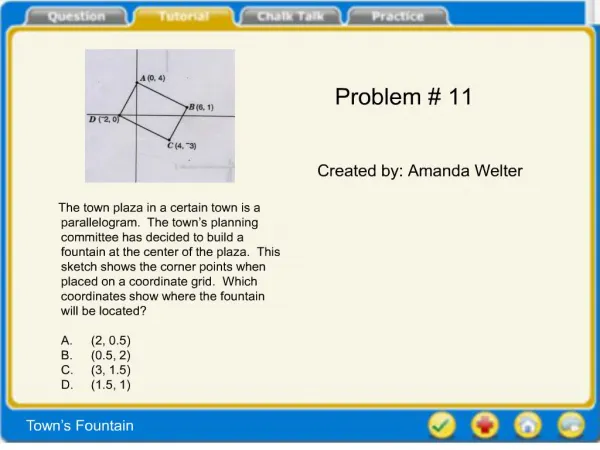

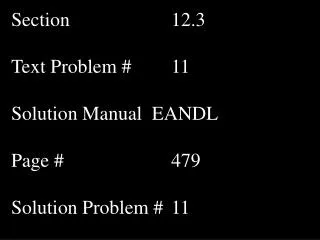

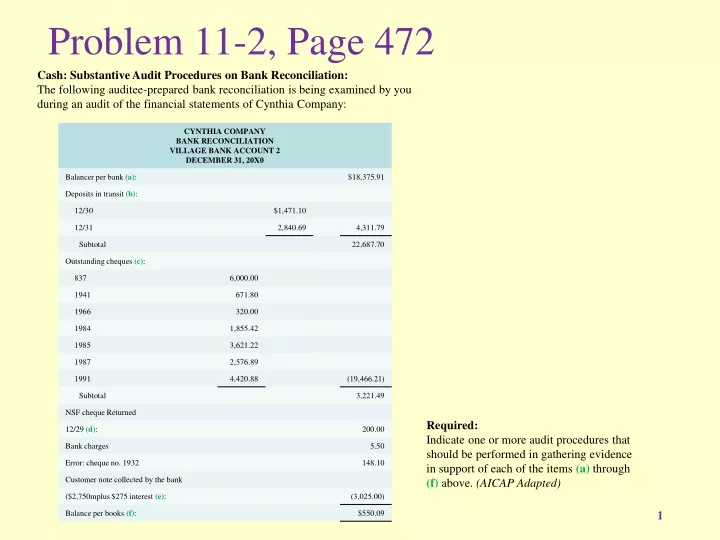

Problem 11-2, Page 472. Cash: Substantive Audit Procedures on Bank Reconciliation: The following auditee-prepared bank reconciliation is being examined by you during an audit of the financial statements of Cynthia Company:. Required:

E N D

Problem 11-2, Page 472 Cash: Substantive Audit Procedures on Bank Reconciliation: The following auditee-prepared bank reconciliation is being examined by you during an audit of the financial statements of Cynthia Company: Required: Indicate one or more audit procedures that should be performed in gathering evidence in support of each of the items (a) through (f) above. (AICAP Adapted)

Basic audit procedures that should be performed in gathering evidence in support of each of the items (a) through (f) of the CYNTHIA COMPANY bank reconciliation are as follows: • Balance per bank • Confirmation by direct written communication with bank (see Standard Bank Confirmation). • Obtain and inspect a January cutoff bank statement obtained directly from the bank (examine opening balance). • Deposit in transit • Verify that the deposit was listed in the January cutoff bank statement on a timely basis. • Trace to the cash receipts journal. • Inspect the auditee's copy of the deposit slip for the date of the deposit. • Outstanding cheques • Examine cheques accompanying the January cutoff bank statement and trace all 20x0, or prior, cheques to the outstanding cheque list. • Trace outstanding cheques to the cash disbursements journal. • Examine all supporting documents for those outstanding cheques that were not returned with the cutoff bank statement. • Ascertain why cheque number 837 has been outstanding for so long. • NSF cheque return • Follow up on the ultimate disposition of the NSF cheques. • Examine all supporting documents. • Note collected • Examine the bank credit memo. • Trace to accounting records. • Balance per books • Foot the bank reconciliation to this total and compare with the general ledger balance.

Problem 11-4, Page 473 Alternative Accounts Receivable Procedures. Several accounts receivable confirmations have been returned with the notation “verification of vendor statements is no longer possible because our data processing system does not accumulate each vendor’s invoices.” Required: What alternative auditing procedures could be used to audit these accounts receivable? (AICPA Adapted)

The auditor can consider alternative confirmation methods to test the accounts receivable balance, such as confirming individual invoices in the balance. Auditing procedures other than confirmation which may be used to verify an account receivable include: • Examination of evidence of subsequent payment of the account including: • The customer's remittance advice accompanied by the payment. • The cheque sent in by the customer. • An authenticated bank deposit ticket listing a deposited cheque for the outstanding account. • An entry in the cash receipts book. • A credit posted to the customer's account. • Examination of other evidence including: • Shipping department's notice of shipment, accompanied possibly by a receipted copy of the bill of lading, the customer's purchase order, sales invoices, and any correspondence referring to the shipment of the goods. • Entries removing the goods from inventory. • Time records and work orders, if appropriate. • External inquiries as to the existence and credit rating of the debtor. • Discussion of the account with the auditee's credit manager, examination of credit department records, and records of merchandise returned, and such other investigation as may lead to better understanding of the nature of the account and its collectability.