Download

1 / 14

140 likes | 158 Views

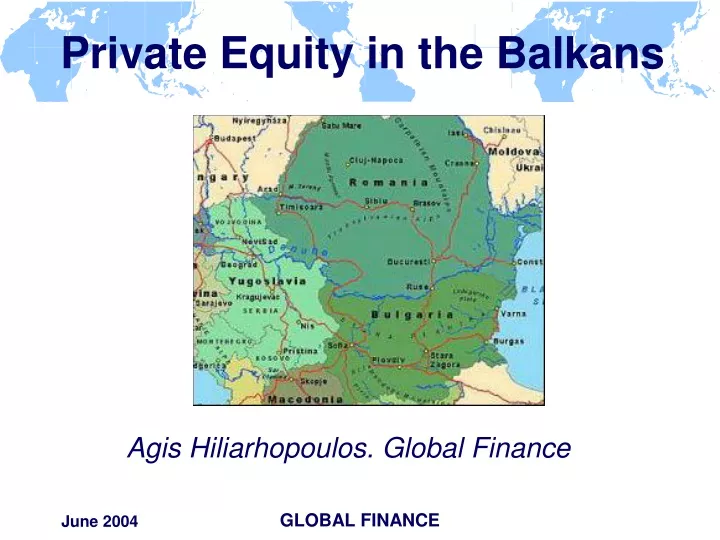

Private Equity in the Balkans. Agis Hiliarhopoulos. Global Finance. Private Equity in the Balkans. Bulgaria and Romania. Both catching up with other CEE countries Both on the right track, although still some ground to be covered Both offered a target date (2007) for EU membership

E N D

Private Equity in the Balkans Agis Hiliarhopoulos. Global Finance GLOBAL FINANCE

Private Equity in the Balkans GLOBAL FINANCE

Bulgaria and Romania • Both catching up with other CEE countries • Both on the right track, although still some ground to be covered • Both offered a target date (2007) for EU membership • Pre-accession status should accelerate growth • NATO membership was also seen as potential catalyst A textbook growth play GLOBAL FINANCE

Bulgaria Key indicators 1999 2000 2001 2002 2003 Real GDP growth (%) 2.3 5.4 4.1 4.2 4.3 CPI (%) 6.2 11.4 4.8 3.8 5.6 Unemployment rate (%) 16.0 17.9 17.3 16.3 13.5 FDI ($bn) 0.8 1.0 0.8 0.9 1.4 Source: Foreign Investment Agency • Population 8 million • Consistent growth • Healthy macro-economics • Currency pegged to the Euro • Pro-business environment • FDI recovering GLOBAL FINANCE

Romania • Population 22 million – biggest market in the region • Growing over the past four years • Improving macro-economics • Recent signs of stabilisation Key indicators 1999 2000 2001 2002 2003 Real GDP growth (%) -3.2 1.6 5.3 4.9 4.9 CPI (%) 55 45.7 34.5 22 14 Unemployment rate (%) 11.5 10.5 8.6 14.0 9.0 FDI ($bn) 1.0 1.1 1.2 1.0 1.5 Source: National Statistics Agency GLOBAL FINANCE

Private Equity Advantage • A window of opportunity for Private Equity: • Most banks still quite conservative, • Stock markets effectively closed to new issues, • Local conglomerates and wealthy entrepreneurs opportunistic rather than long-term. • Increasing presence of private equity funds, either with or without local presence, follows period during which early movers pulled-off or remained on the sidelines. GLOBAL FINANCE

Investment Focus • Companies in need of expansion capital, which have significant potential for growth • Companies building strong brand names and distribution networks, taking strong positions in the local markets as those emerge • Companies taking advantage of local resources to successfully compete in niche segments in the region • Companies which could be attractive acquisition targets a few years down the road • Companies with strong and sustainable cashflows. GLOBAL FINANCE

Private Equity in the Balkans GLOBAL FINANCE

Environment still difficult • Purchasing power remains low – price competition stiff – margins squeezed. • Currency depreciation in Romania eats into assets. • Lots of unfair competition in many sectors. But it’s getting better by the day GLOBAL FINANCE

Investing remains challenging • Widespread practices of non-recording revenue and expenses to avoid VAT an obstacle to private equity investors. • Entrepreneurs are more often than not unfocused or unsophisticated. • Shortage of experienced professional management. • Private equity often competes with “grey” money. But it’s getting better by the day GLOBAL FINANCE

Private Equity in the Balkans GLOBAL FINANCE

Some background • Global Finance invested in April 2003 in what was then a EUR 12m dairy company. • UMC was loss-making with declining sales and overdue payments to milk suppliers. • Global Finance invested EUR 5m through a Share Capital Increase for a majority stake and embarked on an effort to turnaround the company. • In the first 5 months of 2004 UMC grew 56% with focus product lines growing even more. GLOBAL FINANCE

Key lessons – before the deal • Need to be extremely patient and persistent in discussions and negotiations. • Personal relationships matter as much as everywhere. • “Accounting gymnastics” are to be expected (as much as everywhere). • It’s of paramount importance to bring value to the company (and the other shareholders). GLOBAL FINANCE

Key lessons – after the deal • Maintaining a good relationship with partners is key. • It pays off to have more funds than originally envisaged. • Striving for efficiency is negatively influenced by an environment of largely inefficient business partners (suppliers, banks, media agencies, etc.) – Time and close supervision (and lots of patience) are needed. • Building a strong and coherent management team is a challenge. GLOBAL FINANCE