Download

1 / 21

210 likes | 302 Views

Price Responsive Load Programs: Framing Paper #1. Charles Goldman E. O. Lawrence Berkeley National Laboratory CAGoldman@lbl.gov NEDRI Meeting Boston, MA April 2, 2002. Outline of Presentation. Benefits (and Costs) of PRL Programs Summary of Recent Experience with PRL programs

E N D

Price Responsive Load Programs: Framing Paper #1 Charles Goldman E. O. Lawrence Berkeley National Laboratory CAGoldman@lbl.gov NEDRI Meeting Boston, MA April 2, 2002

Outline of Presentation • Benefits (and Costs) of PRL Programs • Summary of Recent Experience with PRL programs • Innovative PRL programs offered by LSEs • Potential & Actual Market Response • ISO experience and program design • Types of Wholesale Market DR Programs • Overview of Key Policy Issues

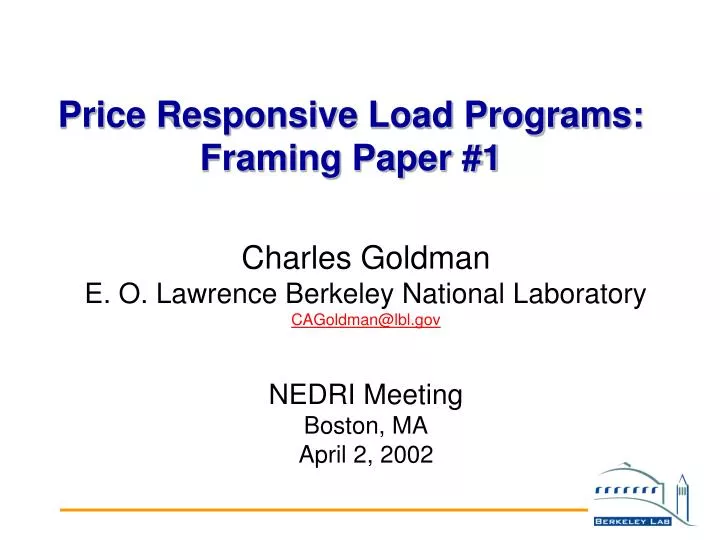

Benefits of PRL Programs Price Price 2 3 P2 P2 Collateral Savings Participants Demand P 4 PL P1 P1 1 Supply Q0 Q2 Q1 Load Q2 Q1 Load 1 Demand (Q1) at Retail rate (P1) Retail demand supplied at higher wholesale price (P2) 2 Reduction in participants demand due to higher price 3 LBMP after scheduled load reduction Source: Neenan Associates, NYISO PRL Evaluation 4

Costs and Benefits of NYISO Programs: Summer 2001 Results • Estimated market benefits to all consumers are large relative to incentive costs • Need standardized methods to evaluate market benefits Source: Neenan Associates, NYISO PRL Evaluation, 2001

Characteristics of Innovative LSE PRL Programs • Substantial customer response at high offer prices • Multiple program options & features offered under a single “brand” • LSE/customer share benefits (often not transparent to customer) • Lots of customer care & education • Use of customer-specific baselines • Variety of forward contracting options • Motivated or “incented” LSEs

Portland General Electric’s Demand Buy Back Program • Successful Demand Bidding Program with three variants: day-ahead, week-ahead, and term events (i.e., demand buy-back) • Eligible to customers with >250 kW demand and interval meters • Participation in 2001: 26 customers, 230 MW potential load reduction • Prior to FERC price caps: 122 events (July 2000 – May 2001), 162 MW average load reduction • After FERC price caps: No more day ahead bidding; 75 MW through term events procured prior to caps

Portland General Electric’s Demand Buy Back Program (cont.) • High level of demand response to market opportunities • 230 MW (>50% of participants’ summer peak demand) reduced at $300/MWh incentive • Minimum incentive level for customer response was ~ $70/MWh • Worked with each customer to identify load reduction goal and specific load reduction strategies • E.g., cross-referenced maintenance schedules with facility meter data to determine MW reduction for specific processes, machinery

Cinergy’s PowerShare Pricing Program • Broad Menu of DR offerings under 1 Umbrella • CallOption (three strike prices, two payment plans, four options to reduce Summer usage) • QuoteOption (day-of program; no risk; all year) • Utility Motivation & Role • Financial hedge against wholesale price volatility & physical hedge against supply uncertainty • Advisor for every customer • Programs require significant upfront investment in E-commerce

Cinergy’sPower Share Pricing Program (cont.) • High Market Penetration: • over 90% of large C/I loads (>500 kW) enrolled in 2000 • ~300 small and medium customers enrolled in 2001 • Market response • Large C/I Load: ~2500 MW • Year 2000: ~440-600 MW of potential curtailable load with high prices (but mild summer; no operations) • Year 1999: 200 MW of actual load reductions with prices as high as $850/MWh

Market Activity of PRL Programs: Summer 2001 • Areas with most active PRL Programs: Pac NW,NY • Market activity is relatively low with notable exceptions

Actual Performance of PRL Programs: Summer 2001 • Several programs successfully enrolled ~300-400 MW • Most PRL programs achieved modest actual reductions (Average = 19 MW)

Eligibility and Potential Use of Backup Generators (BUGs) in PRL Programs • Diesel-fired BUGs precluded or limited in some PRL programs/areas • In “emergency” DR programs, BUGs account for 31% of subscribed load (not shown)

Types of Wholesale Market PRL Programs • Program Types: • Day Ahead Price-Capped Load Bidding • Load Reduction Bidding as Generation • Transitional Load Reduction Pricing • Voluntary Response to Market Price • Discuss merits relative to criteria and goals • Program Types are not mutually exclusive; can be complementary

Day Ahead Price-Capped Load Bidding (#1) • A basic structural feature likely to be included in SMD for day-ahead energy market (DAM) • LSEs bid price points at which specific MW would be reduced – i.e., they bid a “demand curve” • “No program” or “base case” approach • Pros: fully integrated into DAM; no additional ISO uplift charges; no need for customer baseline load (CBL) estimate • Cons: small DR market impact; participation limited to LSEs

Load Reduction Bidding as Generation (#2) • Separate load reduction “product” that can compete with generation in the day ahead energy market – e.g., NYISO DADRP • Potential to fully incorporate load reduction bids into ISO scheduling and settlement processes • Payments and penalties based on difference between CBL and metered load • Pros: potential for significant DR impact; can be fully integrated into wholesale market; non-LSEs or customers can participate directly • Cons: increased ISO uplift; additional admin. & transaction costs; CBL

Transitional Load Reduction Pricing (#3) • Incentives decoupled from wholesale market • Provides opportunity for simpler program structure and more predictable incentives • Can be achieved through any number of specific program designs - e.g., load bids with price floors, call-option programs with reservation payments, etc. • Pros: potential for significant DR impact from risk averse customers • Cons: less direct impact on market than Options 1 and 2; additional uplift charges; seen as “preferential” to loads

Voluntary Response to Market Price (#4) • Customers are paid the real time market clearing price for voluntary curtailments • Based on ISO-NE Price Response Program • Customers must be able to respond without knowing where the price will settle • No penalties • Load reductions not integrated into ISO scheduling • Pros: few risks to customers; may provide potential for additional load reductions to DAM • Cons: less direct impact on market; no price certainty for customers; difficult to predict response

Key Policy Questions • What market mechanisms are needed or desired by end users and other market participants in the PRL area? • Should PRL programs be administered and supported by ISOs or only at the state PUC/retail level? • Under what conditions are ISO-supported PRL programs appropriate – e.g., are PRL programs necessary if RTP was widespread? • Relative magnitude of demand response resources (DRR) needed to ensure efficient wholesale markets? • Will PCLB provide sufficient DRR resources or will other types of PRL programs be necessary?

Key Policy Questions (cont) • How do you pay for the enabling DR technology infrastructure necessary to capture consumer market benefits of PRL? • Is the provision of demand response resources an attractive business opportunity for load aggregators? • Is it a viable “stand-alone” business”? • Are there disincentives that limit interest of potential load aggregators? • What types of DRR should be eligible to participate in PRL programs • Role of and/or limits on use of diesel-fired BUGs

Program Design Issues • ISO/End User relationship and eligible entities • Financial Incentives for PRL Programs • Methods for estimating Customer Baseline Loads (CBL) • Relationship between Emergency DR Programs and PRL Programs