Download

1 / 4

60 likes | 236 Views

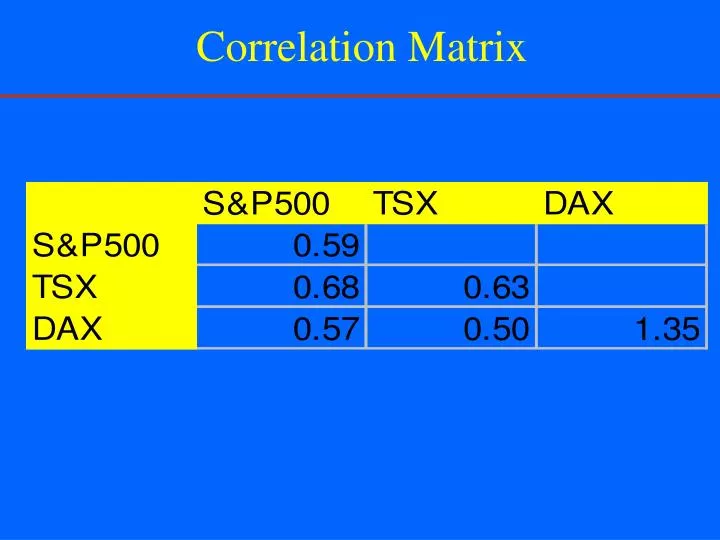

Correlation Matrix. Solution. The portfolio variance is: The first order conditions are:. Constrained Optimization. Foreign content restriction: X+Y< 30% The Lagrangian: FOC:. Solution. FOC:.

E N D

Solution • The portfolio variance is: • The first order conditions are:

Constrained Optimization • Foreign content restriction: X+Y<30% • The Lagrangian: • FOC:

Solution • FOC: