Download

1 / 4

130 likes | 888 Views

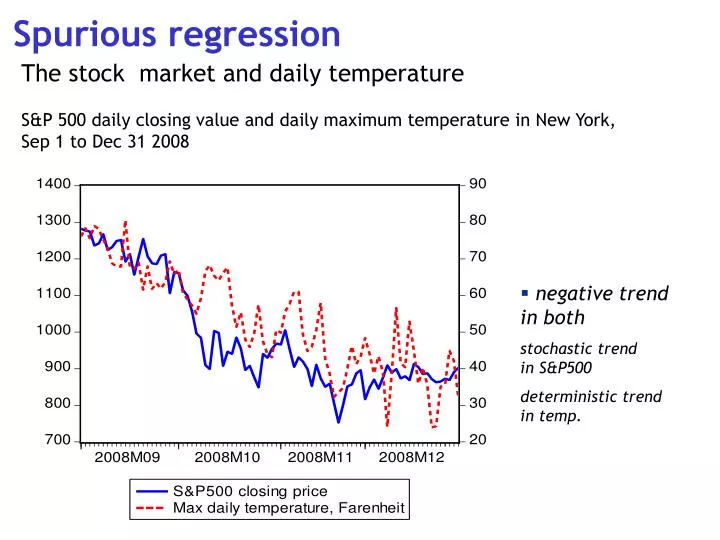

Spurious regression. The stock market and daily temperature S&P 500 daily closing value and daily maximum temperature in New York, Sep 1 to Dec 31 2008. negative trend in both stochastic trend in S&P500 deterministic trend in temp. Spurious: ln(SP) and ln(Temperature).

E N D

Spurious regression The stock market and daily temperature S&P 500 daily closing value and daily maximum temperature in New York, Sep 1 to Dec 31 2008 • negative trend in both stochastic trend in S&P500 deterministic trend in temp.

Spurious: ln(SP) and ln(Temperature) Spurious regression: ln(SPt) = α + βln(temperaturet) + ut Another spurious regression would be: SPt = α + βtemperaturet + ut

Correct: Δln(SP) and Δln(Temperature) Spurious regression: Δln(SPt) = α + βΔln(temperaturet) + Δut

Spurious: two simulated RW series Xt = Xt-1 + ωtωt~WN Yt = Yt-1 + εt εt~WN ωtand εt independent Spurious regression: Yt = α + βXt + ut Correct regression: ΔYt = α + βΔXt + vt