Download

1 / 11

110 likes | 132 Views

This paper analyzes the high level of outward foreign direct investment (OFDI) from Hungary, focusing on the characteristics and motivations of Hungarian multinational companies. It examines four distinct groups of companies and their investment patterns. The research also explores the impact of privatization methods on OFDI in transition economies, as well as the paradox of expansion for avoiding acquisition. The study concludes by highlighting the importance of comparing EMNEs based on ownership structure and distinguishing between regional and global EMNEs.

E N D

Emerging multinationals: the case of Hungary Katalin Antalóczy, Finance Research Ltd., Budapest, Hungary Magdolna Sass, Institute of Economics of HAS, Budapest, Hungary Emerging Multinationals conference, 9-10 October 2008, Copenhagen Business School

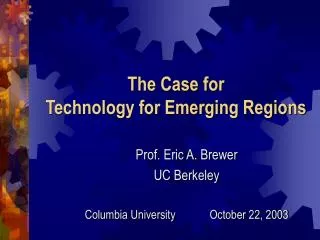

Hungary as a leading outward investor among Visegrad countries Graph 1 FDI outward stock (USD millions) Graph 2 FDI outward stock per capita (2006, USD) Emerging Multinationals conference, 9-10 October 2008, Copenhagen Business School

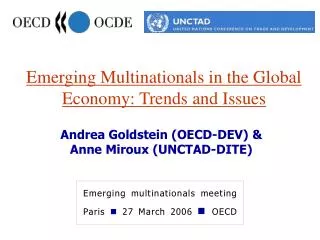

Host country and sectordistribution of Hungarian OFDI Graph 3 FDI outward stock by countries, 2005 (%) Graph 4 FDI outward stock by sector (Millions of Euro) Graph 5 FDI outward stock in manufacturing by sector Emerging Multinationals conference, 9-10 October 2008, Copenhagen Business School

Analysis of OFDI from Hungary Why is OFDI from Hungary so high in Visegrad/NMS comparison? Explanations in theory? (IDP, OLI) Methodology: because of the very concentrated nature of Hungarian OFDI (few big companies): company level investigation, based on detailed company case studies Groups of companies investing abroad: distinctive features – based on these: 4 company groups (mainly based on Aykut and Goldstein, 2006) Emerging Multinationals conference, 9-10 October 2008, Copenhagen Business School

Comparison of the 4 groups of companies investing abroad 1 Emerging Multinationals conference, 9-10 October 2008, Copenhagen Business School

Comparison of the 4 groups of companies investing abroad 2 Emerging Multinationals conference, 9-10 October 2008, Copenhagen Business School

Main findings 1 Group 1 and 2 („indirect” OFDI) • At least 2/3 of total OFDI from Hungary connected to Group 2 (MOL, OTP, Richter, Danubius), formerly state owned companies privatised in the stock exchange with dispersed ownership (high foreign share) and thus the management acting as controlling owner • Firm specific advantages important (OA) • „push factor”: OFDI: a mean for them to strengthen their position reason for expanding • „pull factor”: capability of expanding interntionally successfully: 1. organisational and management advantages in privatising former SOEs in their (or related) sector and restructuring them, helped by specific knowledge, familiarity 2. capital for expansion available due to (former) quasi monopoly position in the domestic market (or at least in some niches) • Distinction in the literature (e.g. Altzinger et al, 2003; Svetlicic and Jaklic, 2006) and related conclusion about the dominance of indirect FDI from Hungary: not acceptable, „real” indirect FDI (Group 1) is maximum 15 % of total Hungarian OFDI • Group 2 can be called „virtual” indirect OFDI, where the controlling owner is not foreign Emerging Multinationals conference, 9-10 October 2008, Copenhagen Business School

MOL shareholder structure (30 June, 2008) Source: MOL Plc Emerging Multinationals conference, 9-10 October 2008, Copenhagen Business School

Main findings 2 Group 3 and 4 („direct” FDI) – more similar than Groups 1 and 2 • Around 20-25% of total Hungarian OFDI • Medium-big and small sized investors distinguished, differing mainly in their geographic targets (Group 4 to closer destinations), motivation (Group 3 more efficiency seeking), and entry modes, mainly as a consequence of their financial strength and means • Relocation from Hungary (not disinvestment): mainly Group 3 Emerging Multinationals conference, 9-10 October 2008, Copenhagen Business School

Concluding questions for further research Importance examining former transition economies – they basically start from zero in terms of FDI and OFDI. What is the impact of privatisation methods on OFDI in former transition economies? The paradox of expanding for escaping acquisition, but thus becoming an even more attractive acquisition target. (E.g. management controlled Hungarian companies introduced on the stock exchange and later acquired: Zalakerámia, TVK, Pannonplast, Borsodchem) More general questions, requiring country comparisons: Difference between EMNEs according to their ownerhsip structure/controlling owner Difference between regional and global EMNEs. Emerging Multinationals conference, 9-10 October 2008, Copenhagen Business School

Thank you for your attention! Emerging Multinationals conference, 9-10 October 2008, Copenhagen Business School