Download

1 / 0

10 likes | 226 Views

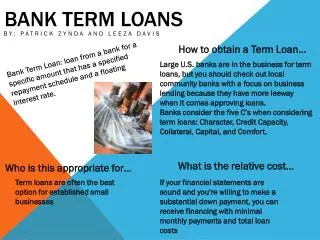

How to obtain a Term Loan…. Bank Term Loan: loan from a bank for a specific amount that has a specified repayment schedule and a floating interest rate.

E N D