Download

1 / 5

50 likes | 85 Views

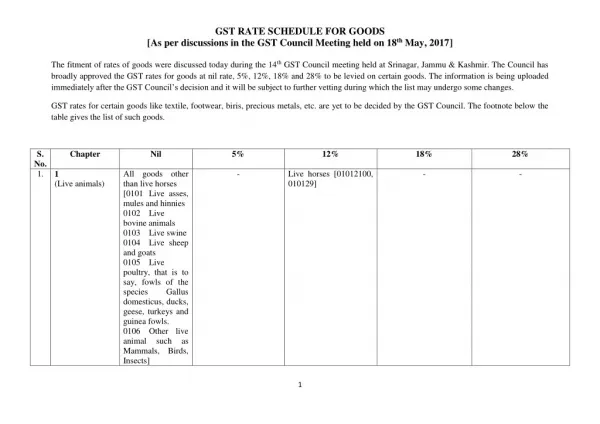

The Goods and Services Tax (GST) Council, during its meeting held on 19 May 2017, broadly approved the GST rates for services at nil, 5%, 12%, 18% and 28%.For more information, please contact your EY advisor. http://www.ey.com/in/en/services/ey-goods-and-services-tax-gst

E N D

24 May 2017 EY – GST News Alert GST Council finalizes tax rates for services under GST regime Executive summary The Goods and Services Tax (GST) Council, during its meeting held on 19 May 2017, broadly approved the GST rates for services at nil, 5%, 12%, 18% and 28%. This Alert provides an insightful coverage of news related to GST and recent developments that are likely to impact trade. It will act as a summary to keep you on top of the latest GST news. For more information, please contact your EY advisor. The Council finalized the classification of various services into different tax slabs, while proposing to continue with exemptions in respect of most of the services that are currently exempt. The list of services that will be under reverse charge and the exemption list have been released in the public domain for general information. There could be some changes in these lists on further vetting. Rail transport and economy class air travel would attract GST at the rate of 5%. Construction of a complex, building and civil structure would be taxed at 12%. Services by way of admission to entertainment events, access to amusement facilities and supply of food/drinks in air-conditioned restaurants in five-star or above rated hotels would attract a higher GST rate of 28%. Services of transfer of right to use goods would attract the same GST rate as applicable to the supply of such goods. While the partial reverse charge mechanism has been done away with, services of GTA, legal services, cab aggregator services, sponsorship services etc. will be covered under reverse charge mechanism. The next meeting of the Council is scheduled on 3 June 2017 to decide on the rates with respect to gold, textiles and a few other goods.

Background ►The Goods and Services Tax Council (GST Council), during its meeting held on18-19 May 2017, finalized the classification of goods and services into different tax slabs of GST and released schedules in public domain. ►The Council proposed to continue with the exemptions on most of the services that are currently exempt. ►Services that will be taxed under reverse charge have been also approved by GST Council. ►The next meeting of Council is scheduled on 3 June 2017, mainly to decide rate of tax for gold, textile and few other goods. Services covered under reverse charge mechanism as approved by GST Council ►Taxable services provided by any person located in a non-taxable territory to any person located in the taxable territory other than non-assessee online recipient (for Online Information and Data Retrieval services). ►Services provided by a goods transport agency (GTA) in respect of transportation of goods by road. ►Services provided by an advocate or firm of advocates by way of legal services. ►Services provided by an arbitral tribunal. ►Sponsorship services. ►Services provided by Government or local authority. The same will not include: ►renting of immovable property, services provided to a person other than Government; ►services in relation to an aircraft or a vessel, inside or outside the precincts of a port or an airport; ►Transport of goods or passengers. ►Services provided by a director of a company to the said company. ►Services provided by an insurance agent to person carrying on insurance business. ►Services provided by a recovery agent to a banking company, financial institution or NBFC. ►Services by way of transportation of goods by a vessel from a place outside India up to the customs station of clearance in India. ►Transfer or permitting use or enjoyment of a copyright covered under clause (a) of section 13(1) of the Copyright Act, 1957 relating to the original literary, dramatic, musical or artistic works. ►Radio taxi or passenger transport services provided through electronic commerce operator. ►In all the above mentioned services, GST shall be payable by a person other than service provider. The list is similar to the existing list of services covered under reverse charge mechanism barring certain additional services. Services classified under 5% GST rate with availability of ITC of input services ►Transport of goods by rail ►Transport of passengers by air in economy class ►services by the Department of Posts by way of speed post, express parcel post, life insurance, and agency

►Transport of passengers by rail1 places meant for residential or lodging purposes having room tariff of Rs.1000 or more but less than Rs.2500 per room per day ►Transport of goods in a vessel2 ►Leasing of aircrafts by a scheduled airlines for scheduled operations. ►Construction of a complex, building, civil structure or a part thereof, intended for sale to a buyer, wholly or partly4 Services with 5% GST rate and full ITC ►Selling of space for advertisement in print media ►Temporary transfer or permitting the use or enjoyment of any Intellectual Property (IP) to attract the same rate as in respect of permanent transfer of IP. ►Services by way of job work in relation to printing of newspapers Services attracting 12% GST rate with ITC available on input services Services with 5% GST rate without ITC ►Services of GTA relating to transportation of goods ►Services provided by foreman of chit fund in relation to chit ►Renting of motorcab3 Services classified under 18% GST rate with full ITC ►Transport of passenger by ►Supply of food/drinks in restaurant having license to serve liquor ►Air conditioned contract/stage carrier other than motorcab ►Supply of food/drinks in restaurant having facility of air-conditioning or central heating at any time during the year ►Radio taxi ►Tour operator services ►Supply of food/drinks in outdoor catering Services with 12% GST rate and full ITC ►Renting of hotels, inns, guest houses, clubs, or other commercial places meant for residential or lodging purposes with room tariff of INR 2500 and above but less than Rs.5000 per room per day. ►Transport of goods in containers by rail by any person other than Indian Railways ►Transport of passengers by air in other than economy class ►Bundled service by way of supply of food of human consumption or any drink, in a premises together with renting of such premises. ►Supply of Food/drinks in restaurant not having facility of air-conditioning or central heating at any time during the year and not having license to serve liquor ►Composite supply of Works contract as defined in sec. 2(119) of CGST Act. ►Renting of hotels, inns, guest houses, clubs, campsites or other commercial ►All other services not specified elsewhere 1 Other than sleeper class 2 includes services provided by a person located in a non-taxable territory to a person located in non-taxable territory by way of transportation of goods by a vessel from a place outside India upto customs station of clearance in India 3 If fuel cost is borne by the service recipient, then 18% GST will apply 4 The value of land is included in the amount charged from the service recipient

Services with 28% GST rate with full ITC Comments The Council’s decision on the services rate structure reflects the logic applied for goods, to stay close to the current effective rates. However, classifying services in different tax slabs may lead to classification challenges, resulting in unwarranted litigation. Applying the rate of 18% to banking, insurance and telecom services is likely to increase the cost of such services. While grandfathering the existing exemptions of various services is a positive step, some of them could be phased out over a period of time in line with the objective of GST. On the flip side, litigation around such exemptions under the current regime might continue even under GST. The development on the GST front gives a strong signal for the July 1 implementation, which now looks imminent. The industry should brace up for the last lap in next few weeks by assessing not only the impact of GST rates but also the overall strategy for transition into the new tax regime. ►Admission to entertainment events or access to amusement facilities5 ►Services provided by a race club by way of totalisator or a licensed bookmaker in such club; ►Gambling ►Supply of Food/drinks in air-conditioned restaurant in 5-star or above rated Hotel ►Accommodation in hotels including 5 star and above rated hotels, inns, guest house, clubs, or other commercial places meant for residential or lodging purposes, where room rent is Rs.5000/- and above per night per room. GST rate and Compensation Cess to be the same as on supply of similar goods ►Transfer of the right to use any goods for any purpose for cash, deferred payment or other valuable consideration. ►Any transfer of right in goods or of undivided share in goods without transfer of title thereof. ►Supply consisting of transfer of title in goods under an agreement which stipulates that property in goods shall pass at a future date upon payment of full consideration as agreed (value of leasing services shall be included in the value of goods supplied) 5 Including exhibition of cinematograph films, theme parks, water parks, joy rides, merry-go rounds, go- carting, casinos, race-course, ballet, any sporting event such as IPL and the like

Our offices Ahmedabad 2nd floor, Shivalik Ishaan Near C.N. Vidhyalaya Ambawadi Ahmedabad - 380 015 Tel: Fax: + 91 79 6608 3900 Bengaluru 6th, 12th & 13th floor “UB City”, Canberra Block No.24 Vittal Mallya Road Bengaluru - 560 001 Tel: Fax: + 91 80 2210 6000 Ground Floor, ‘A’ wing Divyasree Chambers # 11, O’Shaughnessy Road Langford Gardens Bengaluru - 560 025 Tel: Fax: +91 80 2222 9914 Chandigarh 1st Floor, SCO: 166-167 Sector 9-C, Madhya Marg Chandigarh - 160 009 Tel: Fax: +91 172 331 7888 Chennai Tidel Park, 6th & 7th Floor A Block (Module 601,701-702) No.4, Rajiv Gandhi Salai Taramani, Chennai - 600 113 Tel: Fax: + 91 44 2254 0120 Delhi NCR Golf View Corporate Tower B Sector 42, Sector Road Gurgaon - 122 002 Tel: Fax: + 91 124 464 4050 3rd & 6th Floor, Worldmark-1 IGI Airport Hospitality District Aerocity, New Delhi - 110 037 Tel: Fax + 91 11 6671 9999 4th & 5th Floor, Plot No 2B Tower 2, Sector 126 NOIDA - 201 304 Gautam Budh Nagar, U.P. Tel: Fax: + 91 120 671 7171 Hyderabad Oval Office, 18, iLabs Centre Hitech City, Madhapur Hyderabad - 500 081 Tel: Fax: + 91 40 6736 2200 Jamshedpur 1st Floor, Shantiniketan Building Holding No. 1, SB Shop Area Bistupur, Jamshedpur – 831 001 Tel: BSNL: +91 657 223 0441 Kochi 9th Floor, ABAD Nucleus NH-49, Maradu PO Kochi - 682 304 Tel: Fax: + 91 484 270 5393 Kolkata 22 Camac Street 3rd Floor, Block ‘C’ Kolkata - 700 016 Tel: Fax: + 91 33 2281 7750 Mumbai 14th Floor, The Ruby 29 Senapati Bapat Marg Dadar (W), Mumbai - 400 028 Tel: Fax: + 91 22 6192 1000 5th Floor, Block B-2 Nirlon Knowledge Park Off. Western Express Highway Goregaon (E) Mumbai - 400 063 Tel: Fax: + 91 22 6192 3000 Pune C-401, 4th floor Panchshil Tech Park Yerwada (Near Don Bosco School) Pune - 411 006 Tel: Fax: + 91 20 6601 5900 Ernst & Young LLP + 91 79 6608 3800 EY | Assurance | Tax | Transactions | Advisory + 91 40 6736 2000 About EY EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. + 91 80 4027 5000 + 91 80 6727 5000 + 91 80 2224 0696 +91 657 663 1000 EY refers to the global organization and may refer to one or more of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com. + 91 484 304 4000 +91 80 6727 5000 + 91 33 6615 3400 Ernst & Young LLP is one of the Indian client serving member firms of EYGM Limited. For more information about our organization, please visit www.ey.com/in. +91 172 331 7800 Ernst & Young LLP is a Limited Liability Partnership, registered under the Limited Liability Partnership Act, 2008 in India, having its registered office at 22 Camac Street, 3rd Floor, Block C, Kolkata – 700016. + 91 22 6192 0000 © 2017 Ernst & Young LLP. Published in India. All Rights Reserved. + 91 44 6654 8100 ED None This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither Ernst & Young LLP nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor. + 91 22 6192 0000 + 91 124 464 4000 + 91 11 6671 8000 + 91 20 6603 6000 + 91 120 671 7000 EY refers to global organization, and/or one or more of the independent member firms of Ernst & Young Global Limited Join India Tax Insights from EY on