Download

1 / 52

520 likes | 693 Views

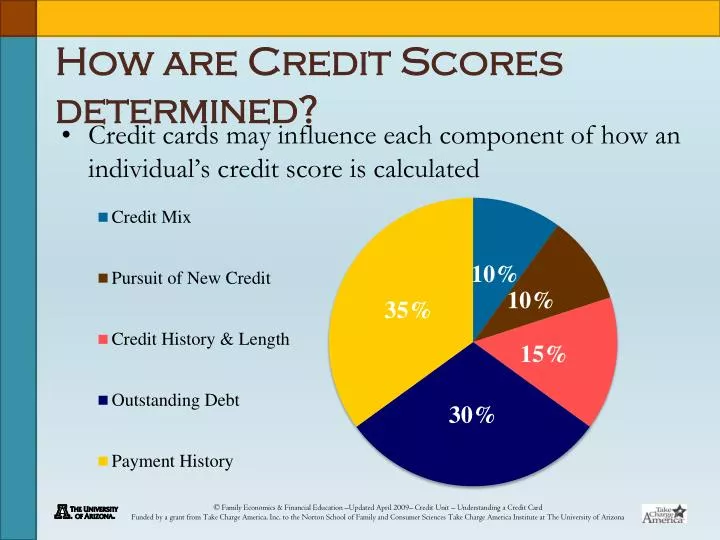

How are Credit Scores determined?. Credit cards may influence each component of how an individual’s credit score is calculated. What is a good FICO credit score?. FICO scores range from 300 – 850. The higher score is better. 750-850 (excellent) 660-749 (good) 620-659 (fair)

E N D

How are Credit Scores determined? • Credit cards may influence each component of how an individual’s credit score is calculated

What is a good FICO credit score? FICO scores range from 300 – 850. The higher score is better. 750-850 (excellent) 660-749 (good) 620-659 (fair) 350-619 (poor)

The higher your credit score, the lower your payments for a car Purchasing a $20,000 car with a 3 yr. loan: Cr. Score APR Mo. Paym. 720-850 6.790% $616 690-719 7.672% $624 660-689 9.171% $638 620-659 10.771% $653 590-619 14.120% $685 500-589 15.127% $695 www.myfico.com(if you have a low credit score, you probably cannot get a loan)

The higher your score, the less you pay on a home loan For example, on a $216,000 30-year, fixed-rate mortgage: credit score interest rate monthly payment 760 – 850 5.26% $1,194 700 – 759 5.48% $1,223 680 – 699 5.66% $1,248 660 – 679 5.87% $1,277 640 – 659 6.3% $1,337 620 – 639 6.85% $1,415 As you can see in this example, a person with a credit score of 760 or better will pay $221 less per month for a $216,000 30-year, fixed-rate mortgage than a person with a FICO® score of 620 – that’s a savings of $2,652 per year.

Example of how a credit score can move up and down: March 2009

Layaway Before the widespread use of credit cards, most stores had layaway plans. The store kept the merchandise until you paid it off. Some stores have started allowing layaway again, and it is becoming more popular.

New federal laws for students (2/10): Credit card companies cannot solicit on campus or near campus. Cannot offer students “tangible” items like t-shirts to apply for a card. You cannot have a credit card if you are under age 21 unless you can prove you have a steady income or you have a co-signer. Example: If you are 18 and in the Navy, you may be able to get a credit card after you get a paycheck for a year. Example of a co-signer: a parent signs the card application. If you do not pay, the parent is responsible.

The Cost of Using Credit $300 for an IPod/accessories And it will take 3 years and 8 months to pay off APR = 24% Minimum Payment of 4% or $12 Finance Charge $149.99 Your IPod REALLY cost $449.99 After you’ve made the last payment, will your iPod still be around??? 4-H 1

How Long Will It Take? You charge $3,000 for furniture. And it will take nearly 11 YEARS to pay off APR = 18% Minimum Payment of 4% or $120 Finance Charge $1,715.67 Total cost of original $3,000 loan = $4,715.67 After you’ve made the last payment, will you still be using that furniture in 11 years? 4-G 1

Prime Rate Credit card interest rates are based on the Prime Rate

What is a Prime Rate? The Prime Interest Rate is the interest rate charged by banks to their most creditworthy customers. The current Prime Rate is 3.25% Providers of consumer and commercial loan products often use the U.S. Prime Rate as their base lending rate, then add a margin (profit) based primarily on the amount of risk associated with a loan.

How is the prime rate calculated? The U.S. Prime Rate is determined by adding 3.00 percentage points to the “federal funds target rate.” For example, if the fed funds target rate is 0.25%, then the U.S. Prime Rate will be 3.25%.

What is the Fed Funds Target Rate? It is the interest rate banks charge each other for loans. The federal funds target rate is controlled by a group within the U.S. Federal Reserve system called the Federal Open Market Committee (FOMC). The FOMC holds a monetary policy meeting eight times every year to decide whether to raise, lower or make no changes to the fed funds target rate.

understanding the information on a credit card application • The Federal Truth in Lending Act of 1968 required card issuers to display the costs of a credit card in an easy to read format. (among other rules) • The Credit Cardholder’s Bill of Rights Act of 2008 refined this law even further by requiring the wording to be more understandable, the print large, and certain information must be in bold and/or larger font.

Information you need to know • Above is some of the types of information you need to know when applying for a credit card. These are explained further in the next slides.

Annual percentage rate • Annual percentage rate (APR) – Interest rate charged for amount borrowed in terms of per dollar per year. • All APR’s for credit cards are based on the Prime Rate. The credit card application will tell you how much is added to the prime rate. Your APR is based on your credit rating (score). • The lower the interest rate, the better

How to Avoid Paying Interest on Purchases • As long as you pay your entire balance by 5:00 on the day it is due, you will not pay interest on the balance. If the due date is a weekend or holiday, it is due at 5:00 on the next business day.

Minimum finance charge • If you don’t pay off the balance, you pay a finance charge, which is based on the APR and the balance you owe. • Minimum finance charge – Minimum amount charged for card use if you don’t pay the entire balance. • Card companies make you pay a finance charge even if you have a very low balance.

Balance calculation method • Balance calculation method for purchases- Method used to determine balance for finance charges. • You will learn how banks calculate Average Daily Balance when we start the assignments.

Annual fees • Annual fees- Yearly charge for credit card ownership • These used to be virtually unheard of, but with the law changes in 2010 many companies are starting to charge annual fees again.

Cash advances • What is a Cash Advance? • The APR for Cash Advances is higher than the card APR • Transaction fees for cash advances – If you choose to withdraw cash using your credit card, there are always extra fees. Typically 3-5% of how much you withdraw.

Late payment fees • Late payment fees – Penalty fee for payments not made by the due date (even one day late, or paid after 5:00 on the due date) • Usually based on your balance, but can be a flat fee. $39 is typical • Late payments can affect your credit score.

Penalty APR’s • Your APR can jump to a “penalty rate” if you: • Pay less than the minimum payments • Don’t pay the minimum by the due date • Make a payment that is returned (bounced check) • Penalty rates are typically 27% and up.

Credit limits • Every card has a credit limit, and it is based on your credit score. • For example, someone with very little credit history or a poor credit score may have a credit limit of $250-$500. • A person with a good credit score may have a limit of $10,000 or more.

Over the limit fees • The new credit card law requires the bank to decline your charge if your purchase will put you over your credit limit. • You can opt to change that if you choose, but if you go over the limit you pay a fee, usually of $39.

Balance Transfers • Moving the amount you owe on a credit card to a different credit card is called a balance transfer. • Companies will advertise a lower interest rate for balance transfers. • These are usually introductory rates and will only last for a short time. • Why do credit card companies try to tempt you to transfer balances?

Safety tips Sign card with a signature and “Please See ID” Do not leave cards lying around Close unused accounts in writing and by phone, then cut up the card Do not give out account numbers over the phone unless making purchases with a secure company. Keep a list of all cards, account numbers, and phone lists separate from cards (copy the f/b of cards) Report lost or stolen cards immediately.

Fair Credit Billing Act • Helps to protect consumers while using a credit card to make purchases • It allows the consumer to not pay for a product or service for which the consumer has a complaint • Billing disputes are covered within the Fair Credit Billing Act for credit cards • If products are not delivered or if it is not what they consumer requested, any amount of money that was credited to the card above the $50.00 fee that consumers are responsible for will be issued back • Debit cards do not have the same protection • Making credit cards a safer form of payment for online purchases

7.1 Account Statements Formula used to calculate the new balance on your credit card : New Balance = Previous Balance + Finance Charge + New Purchases – Payments – Credits Turn to p. 286, #1 for practice (answers next slide)

p. 286, #1 You owed $600 on your last bill (previous bal.) You did not pay it all, so you had a finance charge (interest) of $7.50 (+) You bought $90 at the store and used your card. (+) You sent $100 as a payment (-) Your new balance is $597.50 Try #2 on p. 286

p. 286, #2 • $270.78 Assignment: • pp. 286-287 (3, 5, 9-14) • #10, the $40 is not deducted yet

P. 286 3. $649 5. $337.65 $1,809.30 $299.97 $182.09

p. 286 $679.58 a. $109.90 b. $188.73 c. $369.04 $2494.20

Lesson 7.3—how the bank calculates finance charges on a credit card Average Daily Balance Method (New Purchases Included) Average Daily Balance—The average daily balance is the average of the account balance at the end of each day of the billing period. The company adds purchases and subtracts any payments or credits posted during that day from the beginning balance. The ending balances for every day are then totaled and divided by the number of days in the billing period to get the average daily balance. This number is used to calculate finance charges. Average Daily Balance = Sum of Daily Balances Number of Days in Billing Period

Number of Days in the Billing Period: how many days does the bank use to calculate your A.D.B.? Usually it is the total number of days in that month, but it can be days from a previous month also. Use a calendar if necessary. Post Date—shows dates when the bank recorded your purchases or payments. Anything that would make the balance change. **the post date will not always be the same date you bought the merchandise—there is usually a difference.

Transactions—either a payment or credit (returned something) that is deducted from the Balance or a purchase or fee that is added to the Balance. End of Day Balance— Previous Balance - Payments + Purchases Number of Days—the number of days that the balance remained the same. Sum of Daily Balances— Balance at End of Day x Number of Days

Look at the chart below to visualize how the Average Daily Balance is calculated. The billing period is the entire month of October.

*(does this equal the number of days in October?) _____________add add _______________

YOU HAVE ENOUGH INFORMATION TO FIND the Average Daily Balance: Sum of Daily Balances ÷ Number of Days in Billing Period = _____________________ Complete Practice Problem #1 in your notes.

Lesson 7.3, Part II: CALCULATING THE NEW BALANCE Use Practice Problem I (December) at the TOP of the previous page in your notes to find the new balance below. The APR is 24%. Finding the New Balance Step 1: Find the Average Daily Balance (already found in Practice Problem I--$119.31)

Lesson 7.3, Part II: CALCULATING THE NEW BALANCE Periodic Rate (if not given) = APR ÷ 12 (24% ÷ 12) = 2% Step 2: Find the Finance Charge: Average Daily Balance x Periodic Rate $119.31 x .02 = $2.39