Download

1 / 32

340 likes | 634 Views

DETERMINANTS OF INTEREST RATES. CHAPTER 2. Time Value of Money (TVM) and Interest Rates. The TVM concept assumes that interest earned over given period of time is immediatelly reinvested: Compounded Suppose you invest $ 1000 Simple interest: For 1 year at 12% interest rate;

E N D

DETERMINANTS OF INTEREST RATES CHAPTER 2

Time Value of Money (TVM) andInterest Rates • The TVM concept assumes that interest earned over given period of time is immediatelly reinvested: Compounded • Suppose you invest $ 1000 • Simple interest: • For 1 year at 12% interest rate; Value in 1 year: 1000+1000x(0.12)= $1120 • For 2 years at 12% int. Rate; Value in 2 years: 1000+1000x(0.12)+1000x(0.12)=$1240

Compound Interest. • Value in 1 year: 1000+1000x(0.12)= $1120 Value in 2 years: 1000+1000x(0.12)+1000x(0.12)+1000x(0.12)x(0.12)=$1254.4

Alternatively TVM can be used to convert the value of Future cash flow into their Present Values. • Payments: • Lump-sum payment • Annuity

For Lump-sum payments; • For Annuities

There is a negative relationship btw the interest rates and Present Value. • There is a positive relationship btw the interest rates and Future Value

Effective Annual Return • The annual interest rate used in the TVM equations are the simple (nominal or 12 month) interest rate. • However if the interest is paid and compounded more than once a year, the true annual rate will be the effective (equivalent) annual rate (EAR)

Example: What is the EAR on the 16% simple return compounded semiannully? • r =0.16/2=0.08 • EAR=(1+0.08)2 -1 = 0.01664 =16.64% • What if it is compounded quarterly? • r =0.16/4=0.04 • EAR=(1+0.04)4 -1 = 0.01698 =16.98%

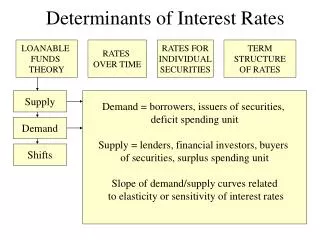

Loanable Funds Theory • It is the theory of interest rates determination that views equilibrium interest rates in financial markets as a result of supply and demand for loanable funds • The supply of loanable funds: Net supplier of funds (households) • The demand of loanable funds: Net demanders of funds (corporations and government)

Interest Rate Supply E Demand Q* Quantity of Loanable Funds Demand and Supply

Factors that cause the supply and demand curves for loanable funds shift

Determinants of Interest Rates for Individual Securities 1) Inflation rate: As actual or expected inflation rate increases, interest rate increases. 2) The real interest rates: It is the rate on a security if no inflation is expected over the holding period Fisher Effect; i = Expected (IP) + RIR

Example: One year T-bill rate in 2012 was 4.53% and inflation for the year was 2.80%. If investors expected the same inflation rate, the according to the Fisher effect the real interest rate for 2012; 4.53%-2.80% = 1.73% • If one-year T-bill rate was 1.89% while the inflation rate was 3.30%. The real rate; 1.89%-3.30% = -1.41 %

3) Default (Credit) Risk: It is the risk that a security issuer will default on making its promised interest and principal payments. As default risk increases, interest rate increases DRP (Default Risk Premiums) = ijt-iTt Bond rating Agencies

Example: 10-year Treasury interest rate was 4.70% Aaa rated corporate debt interest rate was 5.58% Baa rated corporate debt interest rate was 6.70% Average DRP: DRPAaa= 5.58%-4.70% = 0.88% DRPBaa=6.70%-4.70% = 2%

4) Liquidity Risk: If a security is illiquid, the investors add liquidity risk premium (LRP) to the interest rate on the security. 5) Special Provisions and Covenants: Such as taxability, convertability and collability affect the interest rates. As special provisions that provide benefits to the security holder increases, interest rate decreases.

6) Term to Maturity: Term structure of interest rates (yield curve) Maturuiy premium (MP) is the difference between the long and short-term securities of the same characteristics except maturity. • Yield curve: Relationship btw YTM and time to maturity.

Yields may rise with maturity (up-ward sloping yield curve: the most common yield curve) Yields may fall with maturity(Inverted or downward sloping yield curve) Flat yield curve: Yields are unaffected by the time to maturity İJ=f(IP,RIR,DRPJ, LRPJ, SCPJ, MPJ)

Term Structure of Interest Rates • Explanations for the shape of the yield curve fall into 3 theories • Unbiased Expectations Theory • Liquidity Preferences Theory • Market Segmentation Theory

1. Unbiased Expectations Theory • According to this theory, yield curve reflects the market’ s current expectations of future S-T rates. • Suppose an investor has a 4-year investment horizon • Buy a 4-year bond and earn current yield on this bond, 1R4 • Invest in 4 sucessive one-year bonds. You know the 1-year spot rate but form expectations on the future rates on 1-year bond for 3 years, 1R1, E(2r1), E(3r1), E(4r1)

Example: Suppose that the current 1-year rate (spot rate), 1R1=1.94%. • Expected one-year T-Bond rates over the following 3 years are; E(2r1)=3%, E(3r1)=3.74%, E(4r1)=4.10% • Using the unbiased exp. theory current rates for two, three and four year maturity T-Bonds should be;

1R2=[(1+0.0194)(1+0.03)]1/2-1=2.47% • 1R3=[(1+0.0194)(1+0.03)(1+0.0374)]1/3-1=2.89% • 1R4=[(1+0.0194)(1+0.03)(1+0.0374)(1+0.041]1/4-1=3.19%

2. Liquidity Premium Theory • It is based on the idea that investors will hold L-T maturities only if they are offered at a premium to compensate for future uncertainity with security’s value. • It states that L-T rates are equal to geometric average of current and expected S-T rates and liquidity risk premium.

Example: Suppose that the current 1-year rate (spot rate), 1R1=1.94%. Expected one-year T-Bond rates over the following 3 years are; E(2r1)=3%, E(3r1)=3.74%, E(4r1)=4.10% In addition, investors charge a liquidity premium such that; L2=0.10%, L3=0.20%, L4=0.30%,

Current rates for 1,2,3 and 4 year maturity Treasury securities; • 1R1=1.94% • 1R2=[(1+0.0194)(1+0.03+0.001)]1/2-1 = 2.52% • 1R3=[(1+0.0194)(1+0.03+0.001)(1+0.0374+0.002)]1/3-1=2.99% • 1R4=[(1+0.0194)(1+0.03+0.001)(1+0.0374+0.002)(1+0.041+0.003]1/4-1=3.34%

Market Segmentation Theory • Individual investors and FIs have spesific maturity preferences, and to get them to hold maturities other than their prefered requires a higher interest rate (maturity premium). • For exp banks might prefer to hold S-T T-Bonds because S-T nature of their deposits. Insurance companies might prefer to hold L-T T-Bonds because L-T nature of their liabilities (such as life insurance policies)

Forecasting Interest Rates • Upward sloping yield curve suggests that the market expects future S-T interest rate to increase. So that this theory can be used to forecast interest rates. • “Forward rate” is the expected or implied rate on a S-T security. The market’s expectations of forward rates can be derived directly from existing or actual rates on securities currently traded in the spot market.

1R2=[(1+ 1R1)(1+ 2f1)]1/2-1 • 2f1=[(1+ 1R2)2/(1+ 1R1)]-1

Example: The existing (current) one-year, two-year, three-year and four-year zero coupon Treasury security rates; • 1R1=4.32%, 1R2=4.31%, 1R3=4.29%, 1R4=4.34%

Using the unbiased exp. theory, forward rates on zero coupon T-Bonds for years 2, 3 and 4 are; • 2f1=[(1.0431)2/(1.0432)1]-1=4.30% • 3f1=[(1.0429)3/(1.0431)2]-1=4.25% • 4f1=[(1.0434)4/(1.0429)3]-1=4.49%