Download

1 / 69

690 likes | 796 Views

Fiscal Reporting and Performance Management – A Conceptual Framework. Japan IMF Sub Acc. Ian Ball Chairman, CIPFA International. Outline. Session objective Context Key changes The conceptual framework Implementation and marketing Current status. Session Objective.

E N D

Fiscal Reporting and Performance Management – A Conceptual Framework Japan IMF Sub Acc Ian Ball Chairman, CIPFA International

Outline • Session objective • Context • Key changes • The conceptual framework • Implementation and marketing • Current status

Session Objective • To present a conceptual framework that enables high quality fiscal and performance management

Countries with Sovereign Restructuring between 1990-2005 (Agreement Date) Source: Cruces J and Trebesch C, Sovereign Defaults: The Price of Haircuts (Preliminary Paper) December 2010

Context – 1980s New Zealand • Objective was better performance from all parts of the economy • Constitutional arrangements made for ease of action • No written constitution • No states • No Upper House of Parliament • “First past the post” electoral system

Context Financial management and reporting reform in the wider contexts of: • Microeconomic reform • Public sector management reform • State-Owned Enterprise Act 1986 • State Sector Act 1988 • Public Finance Act 1989 • Fiscal Responsibility Act 1994

Key Changes • Permanent tenure for departmental heads replaced with fixed term contracts • Chief executives with annual performance agreements • Use of performance agreements and performance related pay within departments

Key Changes • Very substantial decision-making authority granted to chief executives • Public Service Manual abolished, Treasury Instructions emasculated • No central services

Key Changes • Departments responsible for own accounting systems • Output focus reflected in performance and “purchase” agreements, budgets, appropriations, & reporting • Capital charge introduced

Key Changes • Accounting & appropriations moved to an accrual basis (1989 - 1991) • Financial statements & budgets progressively moved to an accrual basis (1989 - 1994)

Key Changes • Financial reporting in accordance with GAAP • GAAP determined by Accounting Standards Review Board • Audit required for financial and service delivery statements

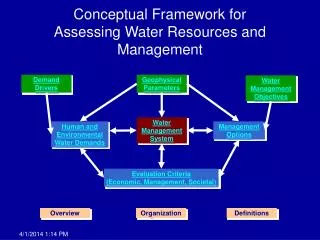

CONCEPTUAL FRAMEWORK Performance Accountability Integration

Performance Defined • “Owner” / “purchaser” distinction • Inputs / outputs / outcomes • “Crown” / department distinction

PERFORMANCE DECISION INCENTIVES PERFORMANCE SPECIFICATION AUTHORITY ON BEHAVIOR INFORMATION Accountability Framework MINISTER CHIEF EXECUTIVE

Budgeting Monitoring/ • Capital Reporting • Operating Operations / Budget Implementation Integrated Management Cycle Strategic Planning

“Purchase” Framework Input Output Outcome Social Benefit Revenue Cost

What Are Outcomes? • Outcomes – impacts on the community (e.g., level of crime, standard of living or health status of the population)

Outcomes Can be Measurable, Specifiable For example: • Quantity • Quality • Timeliness • Location • Population group (e.g. socio-economic status, children)

Outcomes - An Outcome Hierarchy Example: • Biodiversity • Preservation of endangered species • Preservation of endangered birds • Preservation of Yellow-breasted Bunting

What are Outputs? • Outputs – goods and services produced by an organization

Output Dimensions • Quality • Quantity • Timeframe • Location • Cost

OUTCOMES INTERVENTIONS Mix of actions to achieve desired outcomes Outputs Regulations Transfers Taxation Ownership

INPUTS OUTPUTS OUTCOMES Direct costs • Personnel • Travel • Stores Indirect costs • Overheads Reduction in road deaths Speed of transport Pollution Driver training Road traffic research Vehicle inspections

Transport Efficiency Travel Comfort Road Trauma Outcome1 2 3 Output1 2 3 Education Speed Enforcement Research

“Ownership” • Objectives and scope of business • Strategy – especially products/outputs • Financial performance • Capital maintenance • Risks

Financial performance indicators • Revenues • Surpluses/deficits • Cash flow performance • Debt level • Capital expenditure (new projects) • Cost of maintenance/replacement of assets

Non-Financial Performance • Productivity • Legal compliance • Overall service delivery performance

Capability - Financial Financial Capability: • Net worth • Asset and liability measures • Net debt • Contingent liabilities

Capability – Non-financial Non-financial Capability: • Human capital • Physical assets • IT • Intellectual property • Others?

Capability - Additional Dimensions • Reputation • Organisational culture • Staff morale • Political confidence • Ethics and integrity • Stakeholder relationship management • ‘Market’ (operating environment) expertise • Form of organisation / structure • Modes of production e.g. processes and systems, contracting out?

Managing Risk • Key personnel • Fire or natural disaster • Business/systems failure • Financial • Political • Policy • Legal/litigation • Others?

“Ownership” and “Purchase” • Measured quite differently • Financial statements key to ownership performance • Service performance statements for purchase performance • May be traded off against one another • Purchase performance normally has greater political significance

“Crown”/Department Distinction Managing items on behalf of the Crown • Assets (DOC) • Liabilities (DMO) • Revenue (IRD) • Expenses (DSW)

“Crown”/Department Distinction • Based on controllability • Reflected in output specifications • Reflected in balance sheet

PERFORMANCE DECISION INCENTIVES PERFORMANCE SPECIFICATION AUTHORITY ON BEHAVIOR INFORMATION Accountability Framework MINISTER CHIEF EXECUTIVE

Performance Specification Documents - Departments • Departmental Forecast Report • Corporate/Strategic Plan • CE Performance Agreement • Purchase Agreement

Performance Specification Documents - Government • Statement on Long-term Fiscal Position • Fiscal Strategy Report • Economic and Fiscal Update • Budget Policy Statement • Budget • Forecast Financial Statements • Estimates of Appropriation • Investment Statement

Decision-making Authority • Human resources • Purchasing • Capital expenditure • Accommodation • Financial management • systems • information

Incentives • Personal • term contracts • performance pay • Departmental • purchase agreement • budget and appropriations • capital charge

Reporting • Financial performance • Service performance

Departmental Reporting • Statement of Responsibility • Statement of Accounting Policy • Operating Statement • Statement of Financial Position • Statement of Cash Flows • Statement of Contingent Liabilities • Statement of ServicePerformance

Reporting by the Government • Financial statements • Annual • Monthly • Snapshot of the Financial Statements