Download

1 / 17

170 likes | 381 Views

Section 4C Savings Plans and Investments. Pages 246-268. Savings Plans and Investments. The Savings Plan Formula Planning Ahead with Savings Plans Total and Annual Returns Types of Investments Stocks Bonds Mutual Funds. Savings Plans.

E N D

Section 4CSavings Plans and Investments Pages 246-268

Savings Plans and Investments • The Savings Plan Formula • Planning Ahead with Savings Plans • Total and Annual Returns • Types of Investments • Stocks • Bonds • Mutual Funds

Savings Plans Deposit a lump sum of money and let it grow through the power of compounding (4B). Deposit smaller amounts [in an interest earning account] on a regular basis (4A) IRA’s, 401(k), Koegh, PensionSpecial Tax Treatment

ex/pg246 You deposit $100 into a savings plan at the end of each month. The plan has an APR of 12% and pays interest monthly.

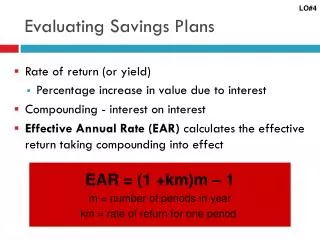

Is there a Savings Plan Formula? WOW !!! where A = accumulated savings plan balance PMT = regular payment amount APR = annual percentage rate (decimal) n = number of payment periods per year Y = number of years This formula assumes the same payment and compounding periods.

Where did this formula come from? Another way to figure accumulated value. After 6 months: End of month1 payment is now worth $100 x (1.01)5 End of month2 payment is now worth $100 x (1.01)4 End of month3 payment is now worth $100 x (1.01)3 End of month4 payment is now worth $100 x (1.01)2 End of month5 payment is now worth $100 x (1.01)1 End of month6 payment is now worth $100

After 6 months: 100x(1.01)5+100x(1.01)4+100x(1.01)3+100x(1.01)2+100x(1.01)1+100 = 100 x ((1.01)5 + (1.01)4 + (1.01)3 + (1.01)2 + (1.01) + 1) Do you see a pattern? After 10 months: A = 100 x ((1.01)9 + (1.01)8 + (1.01)7 + … + (1.01)2 + (1.01) + 1) After 55 months: A = 100 x ((1.01)54 + (1.01)53+ (1.01)52 + … + (1.01)2 + (1.01) + 1)

After N months: A = 100x [(1.01)N-1+(1.01)N-2+(1.01)N-3+ …+(1.01)2+(1.01)+1] BN-1 + BN-2 + BN-3 + … + B2 + B1 + 1 =

ex1/pg246-7 Use the savings plan formula to calculate the balance after 6 months for an APR of 12% and monthly payments of $100. Calculator:

ex2/pg248 At age 30, Michelle starts an IRA to save for retirement. She deposits $100 at the end of each month. If she can count on an APR of 8%, how much will she have when she retires 35 years later at age 65? Compare the IRA’s value to her total deposits over this time period. Calculator:

ex2/pg248 At age 30, Michelle starts an IRA to save for retirement. She deposits $100 at the end of each month. If she can count on an APR of 8%, how much will she have when she retires 35 years later at age 65? Compare the IRA’s value to her total deposits over this time period.

ex2/pg248 At age 30, Michelle starts an IRA to save for retirement. She deposits $100 at the end of each month. If she can count on an APR of 8%, how much will she have when she retires 35 years later at age 65? Compare the IRA’s value to her total deposits over this time period. The accumulated value of the IRA is $229,613 The value of the deposits is 35 x 12 x 100 = $42,000 [Compounding interest accounts for $229,613 - $42,000 = $187,613.] WOW! The Power of Compounding

ex3/pg250(Planning Ahead with Savings) You want to build a $100,000 college fund in 18 years by making regular, end of the month deposits. Assuming an APR of 7%, calculate how much you should deposit monthly. How much of the final value comes from actual deposits and how much from interest?

ex3/pg250(Planning Ahead with Savings) You want to build a $100,000 college fund in 18 years by making regular, end of the month deposits. Assuming an APR of 7%, calculate how much you should deposit monthly. How much of the final value comes from actual deposits and how much from interest?

ex3/pg250(Planning Ahead with Savings) You want to build a $100,000 college fund in 18 years by making regular, end of the month deposits. Assuming an APR of 7%, calculate how much you should deposit monthly. How much of the final value comes from actual deposits and how much from interest? The monthly payments are $232.18. The value of the deposits is 18 x 12 x 232.18 = $50,151 [The accumulated value of the fund is $100,000.] [Compounding interest accounts for $100000 - $50151 = $49849.] WOW! The Power of Compounding

More Practice 47/246 Find the savings plan balance after 18 months with an APR of 6% and monthly payments of $600 49/246 You set up an IRA with an APR of 5% at age 25. At the end of each month you deposit $75 in the account. How much will the IRA contain when you retire at age 65? Compare the amount to the total amount of deposits made over the time period. 53/246 You intend to create a college fund for your baby. If you can get an APR of 7.5% and want the fund to have a value of $75,000 after 18 years, how much should you deposit monthly?

Homework Pages 265-269 # 48, 50, 52, 54