Download

1 / 16

160 likes | 294 Views

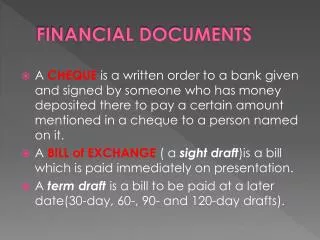

Investigating the flow of financial documents 2. The sequence of documents. Stage 2 – payment notification Seller makes out invoice listing goods, price, discounts and VAT Credit note is issued if any goods are returned

E N D

The sequence of documents Stage 2 – payment notification • Seller makes out invoice listing goods, price, discounts and VAT • Credit note is issued if any goods are returned • End of month – seller issues statement of account listing all transactions and balance owing. May include remittance adviceslip for buyer to return with payment

The invoice To: Jones and Kelly Riverside Walk HIGHTOWN HG2 8PP

The invoice – key points • Always on headed paper • Invoice shows VAT registration number • All items listed separately, then totalled • VAT added to sub-total to give total due • Terms = date when payment due • E & OE = errors and omissions excepted – gives firm right to amend errorslater.

VAT – key points • VAT = value added tax • Charged on most goods/services sold • Current rate = 17.5% – but Government can change rate • Businesses pay VAT to suppliers and collect VAT from customers. They pay the difference to HM Customs & Excise • Small scale businesses do not have to do this – but still have to pay VAT on purchases

Credit note To: Jones and Kelly Riverside Walk HIGHTOWN HG2 8PP

Credit note – key points Only issued when there is a problem and a refund is required, eg • Goods damaged • Incorrect goods delivered – and returned • Fewer goods delivered than charged on invoice • Overcharge on invoice

Statement of account To: Jones and Kelly Customer a/c no: 789 Riverside Walk Credit limit: £10,000 HIGHTOWN HG2 8PP Date: 30 June 2002

Statement of account – key points • Sent at end of month • Starts with any amount owing from previous month • All invoices add to amount owed • All credit notes and payments reduce amount owed • Final column shows balance after each transaction • Ends with current amount due • May include remittance advice for payment

Remittance advice From: Jones and Kelly Customer a/c no.: 789 Riverside Walk HIGHTOWN HG2 Statement date: 30/6/02 Amount enclosedCheque no. Your refDate of payment

Remittance advice – key points • Often tear-off form at end of statement • Customer includes form with payment • Supplier can immediately link payment to customer and statement.

The sequence of documents Stage 3 – making payment • Buyer checks invoice and statement • If correct, normally pays by cheque. Note: receipts may be issued by seller if cash payments are received for any reason

Cheques – key points • Cheques printed by banks • Business cheques include company name • May be completed by hand or printed by computer • Items completed are: date, payee, amount in words and figures • Cheques for large amounts signed by more than one person • Counterfoil states reason for payment

Cash sale receipt EASYPRINT MAIN STREET HIGHTOWN Name: John Smith Receipt no.: 123 Address: 2 Windy Road Date: 10 June 2002 Hightown 50 coloured photocopies £5.50 VAT @ 17.5% £0.96 Total paid £6.46 Received by:Paula King

Cash sales receipt – key points • Proves amount was paid • Should be kept safely in case goods faulty • Normally only issued for cash payments – not required for cheque payments

Computerised accounting packages Used by most businesses to: • Calculate and print invoices, credit notes and statements • Pay suppliers, including printing cheques • Keep records of all transactions including VAT • Produce reports, such as overdue payments • Monitor the bank balance