Download

1 / 4

40 likes | 55 Views

Though you will need the SSN for all the legal and government purposes, the Credit Privacy Number or CPN will help you keep your finances hidden and safe. At ShapeMyCredit, we can help you get the CPN for improving your credit past as well as protecting your SSN. Several people use the CPN to prevent identity theft. For more information, call (818) 299-1636.

E N D

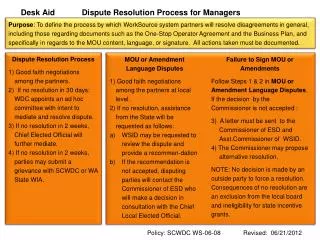

Fair Credit Reporting Act Facts The Fair Credit Reporting Act (FCRA) is the legislation that governs the credit bureaus. The FCRA also provides rules for information furnishers including creditors, collectors, and parties that post to public records. Implementation of FCRA policy is policed by the Federal Trade Commission (FTC). For credit repair purposes some of the most important provisions are included in section 611. Here is a Example: 611 (a) (1) (A) In general. Subject to subsection (f), if the completeness or accuracy of any item of information contained in a consumer’s file at a consumer reporting agency is disputed by the consumer and the consumer notifies the agency directly, or indirectly through a reseller, of such dispute, the agency shall, free of charge, conduct a reasonable reinvestigation to determine whether the disputed information is inaccurate and record the current status of the disputed information, or delete the item from the file in accordance with paragraph (5), before the end of the 30-day period beginning on the date on which the agency receives the notice of the dispute from the consumer or reseller. Beyond 611 The framework for the credit repair dispute process is included in FCRA Section 611. But beyond the legal guidelines provided by the FCRA are two factors just as important to any credit repair effort: common sense and experience.

Credit Repair Finesse Common sense and experience play a large role in the success of any credit repair program. Dealing effectively with the credit bureaus requires some finesse. It is important to have a genuine feeling, and even respect, for the operational process of the credit bureaus. Dispute letters should always conform to the capabilities of the departments that are processing your request. Smart and Simple Effective credit repair disputes must be prepared with clarity, simplicity, and a thorough understanding of legal leverage. Working Around the System Patience and perseverance are essential when dealing with the credit bureaus, as they often implement defensive practices to moderate their work flow. These defensive practices can include dismissive letters claiming “frivolous” disputes, and demands for additional identification, even when perfect identification was furnished. Another FCRA Tool Per the Fair Credit Reporting Act, if you dispute an item on your credit report and it is verified you may request a description of the procedure used to verify the item.

Good Information This is useful if you are not satisfied and would like to pursue the issue further as part of your credit repair program. If asked, the credit bureaus are required to provide the details of the dispute process including the name, address, and phone number of the party that verified the disputed account. They must provide the information within 15 days of receiving your request. Using the Rule Once you have the information in hand your credit repair effort can be efficiently routed to the right person at the creditor. Here’s the law: Section 611 (a) (6) (B) As part of, or in addition to, the notice under sub paragraph (A), a consumer reporting agency shall provide to a consumer in writing before the expiration of the 5-day period referred to in sub paragraph (A)… (iii) a notice that, if requested by the consumer, a description of the procedure used to determine the accuracy and completeness of the information shall be provided to the consumer by the agency, including the business name and address of any furnishes of information contacted in connection with such information and the telephone number of such furnishes, if reasonably available; (7) Description of reinvestigation procedure. A consumer reporting agency shall provide to a consumer a description referred to in paragraph (6) (B) (iii) by not later than 15 days after receiving a request from the consumer for that description.