Download

1 / 1

10 likes | 17 Views

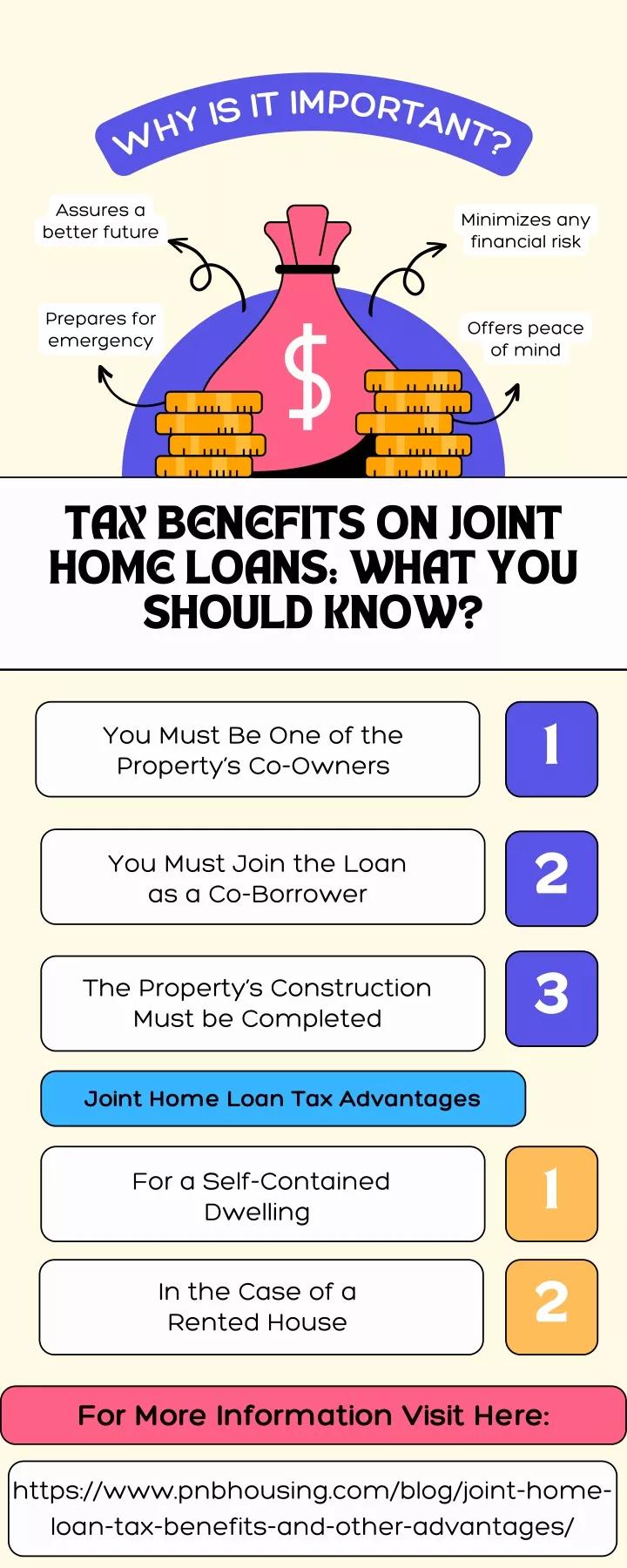

Joint home loans tax benefits offer several to co-borrowers, making them an attractive financing option for married couples, siblings, or friends looking to purchase a property together. The co-borrowers can claim deductions on both the principal and interest components of the loan, resulting in significant tax savings. However, it is essential to understand the eligibility criteria and the distribution of ownership before opting for a joint home loan. With proper planning, co-borrowers can maximize their tax benefits and reduce the burden of home loan repayment.<br>

E N D

WHYIS IT IMPORTANT? Assures a better future Minimizes any financial risk Prepares for emergency Offers peace of mind TAX BENEFITS ON JOINT HOME LOANS: WHAT YOU SHOULD KNOW? You Must Be One of the Property’s Co-Owners 1 You Must Join the Loan as a Co-Borrower 2 3 The Property’s Construction Must be Completed Joint Home Loan Tax Advantages For a Self-Contained Dwelling 1 In the Case of a Rented House 2 For More Information Visit Here: https://www.pnbhousing.com/blog/joint-home- loan-tax-benefits-and-other-advantages/