Download

1 / 24

240 likes | 407 Views

Molecular Diagnostics (AHIC, Watch Lists and Investor Scrutiny). Introductions and Welcome. Paul Henley VP Portfolio Management, Fifth Third CDC Yianni Vitellas VP – Portfolio / Risk Specialist Senior, Huntington CDC Mark Lenhardt Executive Director, Tax Oriented Investments, JPMorgan Chase.

E N D

Molecular Diagnostics(AHIC, Watch Lists and Investor Scrutiny)

Paul Henley VP Portfolio Management, Fifth Third CDC Yianni Vitellas VP – Portfolio / Risk Specialist Senior, Huntington CDC Mark Lenhardt Executive Director, Tax Oriented Investments, JPMorgan Chase Speakers

Investors are more focused on identifying risk by assessing the strength of projects within our portfolio, studying the capacity of our General Partners and evaluating the long-term sustainability of projects within our portfolio. Explore how AHIC standards and investors' needs are evolving.

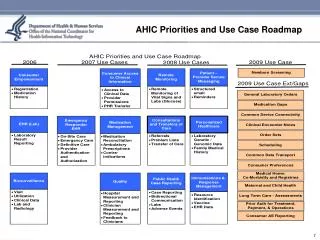

AHIC (Affordable Housing Investors Council) produces best practices for the housing credit field, guidelines that are widely adopted by its members and partners in the affordable housing industry. AHIC created the first reporting database in 1996, with the help of syndicators such as Michigan Capital Fund for Housing. 1996 also saw the adoption of underwriting standards, property inspection reports and exit strategies for all investors. AHIC Standards

AHIC continually updates their standards to keep abreast of the changing and challenging LIHTC world. • In 2004, the Underwriting Standards were updated, then again in 2010 and 2012. • In 2006, the Asset Management Committee of AHIC published new standards for grading projects, and rewrote the Risk Rating guidelines for projects. For the first time, projects are categorized as Development Stage or Operational Stage projects. AHIC Standards

In 2012, AHIC finalized and published its newest version of the Risk Rating Guidelines (hand-out available), Watch List Problem Categories and Asset Management Best Practices. AHIC will celebrate its 20th anniversary in 2015. It will continue to evolve its standards to help in strengthening the projects and long-term sustainability of projects within investors’ portfolios. Current topics of discussion include: i) the best way to balance the needs of urban and rural areas for allocation; ii) the optimal mix of incomes for affordable projects; and iii) what training the SHAs require for staff performing file reviews and physical inspections? AHIC Standards

There are five (5) Risk Ratings: • A – Excellent • B – Average • C – Weak • D – Moderate Risk • F – Significant Risk AHIC Standards

Risk Rating Guidelines • DCR (Debt Coverage Ratio) • Gross Operating Income minus Expenses and Replacement Reserves divided by Debt Service (Principal and Interest) • DCR is at or above 1.20x = “A” • DCR is between .5x and .85x OR significant cash deficits = “D” • Loan is in default on must pay debt = “F” AHIC Standards

Risk Rating Guidelines • Economic Occupancy • Net Rental Revenue divided by Gross Potential Rent • Economic occupancy is 95% or above = “A” • Economic occupancy is below 90% but greater than 80% = “C” • Economic occupancy is less than 80% = “D” AHIC Standards

Risk Rating Guidelines • GP / Sponsor / Property Management • GP / Sponsor is financially secure and able to meet all obligations = “A” • GP / Sponsor has modest financial capacity and liquidity has been identified as an issue / Weak Property Management = “C” • GP / Sponsor lacks ability or willingness to cover guarantee obligations / Management Company is ineffective and replacement is required = “D” AHIC Standards

Risk Rating Guidelines • Program Compliance • No material Compliance issues = “A” • Correctable Compliance issues with financial impact / Failing REAC or MOR score with no corrective plan / 8823s issued and not corrected within 90 days = “C” • Uncorrectable Compliance issues / 8823s issued and left uncorrected at year-end = “D” AHIC Standards

Identifying Risk(Assessing the Capacity of GP’sand Strength of Projects)

Importance of the expertise and capacity of the Developer / General Partner / Guarantor • Underwriting guidelines used in evaluating the Developer / General Partner / Guarantor • Financial capacity and ability to cover guarantee obligations • REO schedules • Contingent liability schedules • Liquidity and net worth requirements Identifying Risk

Syndicator Watch List Reports • Major Issues (the underlying cause(s) of the problem(s)) • Operating Deficit Guarantee (capacity of GP / Guarantor to perform on guarantee) • Funding of Deficits (how deficits are being funded) • Action Plan (what’s being done to fix the problem(s)) Identifying Risk

Periodic Investor Conference Calls • Investors “drill down” to further understand and identify risk Identifying Risk

Investors are increasingly focused on the long-term sustainability of properties • Investors analyze current cash flow / deficits • Investors prepare a projection of cash flow / deficits through the remainder of the compliance period • Investors assess the availability of cash and reserves • Investors assess GP operating deficit guarantee Long-Term Sustainability

Revenues • Issues adversely impacting revenues • Low Area Median Incomes (AMIs) • Occupancy • Property Management • Competition Long-Term Sustainability

Expenses • Issues adversely impacting expenses • Increasing beyond normal expectations • Utilities (Water and Sewer) • Property Taxes • Inefficient HVAC • Building is aging leading to maintenance costs increasing Long-Term Sustainability

Is current deficit considered short-term? Is current deficit reflective of ongoing factors? Is refinancing a possibility? Are reserves sufficient to fund long-term deficits? What is the GP’s capacity to perform on guarantee? Notwithstanding guarantee, what is GP’s willingness to stand behind the project? Long-Term Sustainability