Download

1 / 12

120 likes | 145 Views

Learn about different types of costs like explicit and implicit costs, labor concepts, opportunity costs, and more through key economic concepts. Explore how costs impact profit and decision-making in business.

E N D

COSTS MIKE BECK

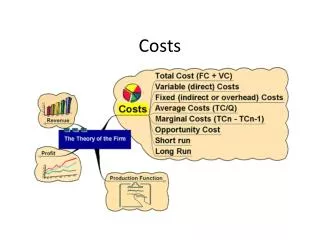

Key Concepts • Explicit- Inputs (Factors of Production) • 1. Land • 2. Labor • 3. Capital • Implicit- Opportunity costs • Entrepreneurial Ability • Total Revenue – (Explicit + Implicit Costs) = Economic Profit • The full opportunity cost of capital invested in a business is generally not included as a cost when accounting profits are calculated. • *Wages is the biggest cost for business • Labor

Concepts Continued • Sunk Cost- Cost you cant get back • Ex. Gym Club Membership • TC=Total Costs • TFC= Total Fixed Costs • Independent of production • TVC= Total Variable Costs • Based on rate of production • TC=TFC+TVC

Concepts (3) • AVC – Average Variable Cost • ATC- Average Total Cost • As marginal costs increase AVC and ATC increase • When Marginal Revenue = Marginal Cost this is the Optimum Level of Output • Opportunity Cost- The next best thing given off in a trade off.

Relation to Other Topics • Negative Externalities • Private Cost- cost to the business • Social Cost-includes negative externality • Long Run • All costs are variable

AP Free Response • http://apcentral.collegeboard.com/apc/public/repository/_ap06_frq_microeconom_51795.pdf • 2006 Exam Question 1

Multiple Choice • 1. When one decision is made, the next best alternative not selected is called • (a) economic resource. • (b) opportunity cost. • (c) scarcity. • (d) comparative disadvantage. • (e) production.

Multiple Choice • 2. What are variable costs? • Select the best answer • A. MC, ATC, AVC, AFC • B. fixed + variable • C. costs that vary with the Qproduced • D. long run ATC falls as Qoutput rises

Multiple Choice • 3. Which of the following is true of the concept of increasing opportunity cost? • (a) It is unimportant in command economies because of central planning. • (b) It suggests that the use of resources to produce a set of goods and services means that as • more of one is produced, some of the other must be sacrificed. • (c) It is irrelevant if the production possibilities curve is convex to the origin. • (d) It suggests that unlimited wants can be fulfilled. • (e) It means that resources are plentiful and opportunities to produce greater amounts of goods and • services are unlimited.

Answers • 1. B • The answer is opportunity cost because the definition of opportunity cost states that it is the next best thing given up. • 2. C • Variable costs are costs that correspond with the quantity that is produced, the more you produce the more costs. • 3. B • The more you produce of one thing, the more you are giving up of another, that is opportunity cost.

Real World • http://news.bbc.co.uk/2/hi/entertainment/7584902.stm • Opportunity Cost • One very recent example was the Titian paintings that were offered to the government for £100M, they were saying on the news how the government could either build a new children's hospital with that money or they could spend it to keep the Titians in the public. The OC of the new hospital is the Titian paintings; the OC of the Titian paintings is the new hospital. • http://www.brighthub.com/office/finance/articles/98561.aspx • Explicit Costs