Download

1 / 3

E N D

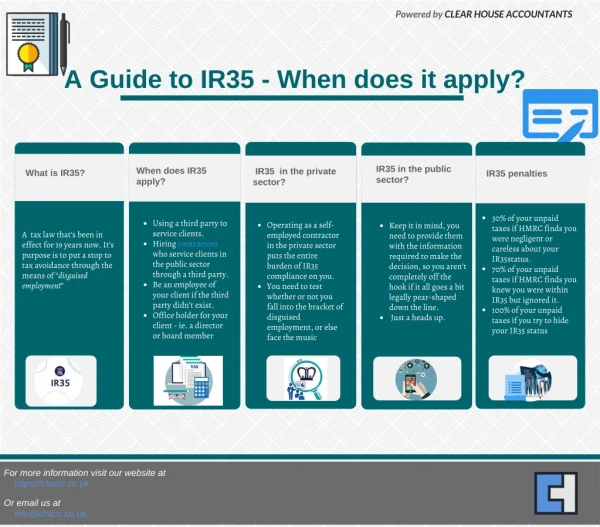

IR35: The beginner’s Guide to Understanding IR35 IR35 rules describes two sets of legislation set up by the UK Government to decide someone’s employment status to combat tax avoidance. To put it in simple words, IR35 is a method devised by Her Majesty’s Revenue and Customs (HMRC) to counter tax avoidance by people who disguise their employments. Before 2000, it was common for the people to switch their status from employee to contractor, hence avoiding the bulk of taxes they would be entitled to pay otherwise. People used to do so because the financial impact of IR35 is enormous and more evident as it can reduce a person’s net income by up to 25%.

HMRC was not very delighted to hear this, so IR35 rules were introduced in the UK to terminate UK residents’ methodology to employ people to avoid taxes. Principles of IR35 UK By the legislation, determining the IR35 status of the contractor or employee is the duty of the person employing them. They must make corroborate that the NIC and other taxes are paid timely to HMRC. On the contrary, in the private sector, this responsibility lies on the shoulder of the contractor himself. He is answerable for checking the IR35 status and checking that NIC and other mandatory taxes are not due to anyone. Fresh IR35 Rules HMRC has deployed the IR35 rule since 2000, but tax experts and business officials aren’t satisfied with the implementation. It is being called a poorly conceived law since then. However, the government has introduced new IR35 rules in the public sector, which will merge with the private sector by April 2020. Yet, these rules will be entirely implemented from 2021, but it includes: For the client: Whether the businesses are public or private sector, the IR35 rules will be managed by the contractors only. If the contractor’s company is inside the IR35 legislation, it will pay off its taxes to the third agency, who was to pay the contractor’s limited company. The third agency should submit the tax deducted from the employee’s wages or salaries to the HMRC. If the contract is non-compliant, then the client would pay the NIC to HMRC. For the contractor: If your client is a small company, then the intermediary, which is the limited company, will decide whether IR35 is applicable or not. The total employees hired by the contractor should be 50 or fewer. Implications of IR35 Legislation HMRC can determine the employment status of the client through the principle of the test of employment status. These may include three basic proposals; if the contractor has set up a contract with these three proposals, the chances of you falling outside the IR35 rules are of greater extent. However, if you are a genuine contractor, employee, freelancer, or interim, you don’t need to worry about anything. 1.Authority: This includes that the contractor and client are two separate entities. Once the work has been completed, the client can no more ask for the contractors’ favor. If the end

client controls you, you might want to amend some points of the contract because you are under serious risk of being caught inside IR35 UK. 2.Right of Substitution: This says that the contractor can bring another contractor or employee to complete the end client’s work. It can put IR35 rules on the contractor. 3.Financial Risk: The HMRC will want the contractor to be fully responsible for the financial reliability. Any error made during the contract would be the contractor’s responsibility. The IR35 is a complex system of legislation established by the UK, but if you become familiar with all the do’s and don’ts, it would help you stay on the law’s right side. If you still have any ambiguities, then talk to our experts at SK Accountants and Tax Consultants Ltd. to get expert advice and assistance in legal issues.