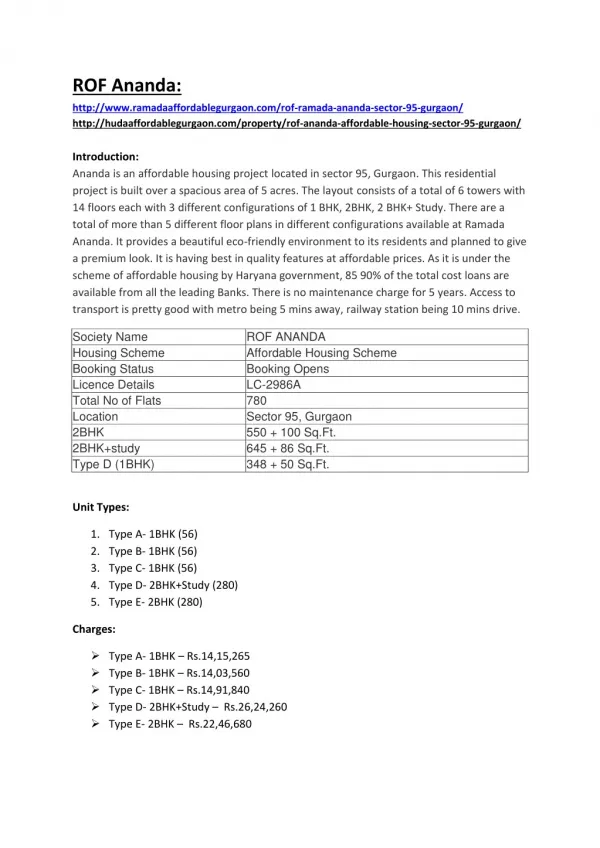

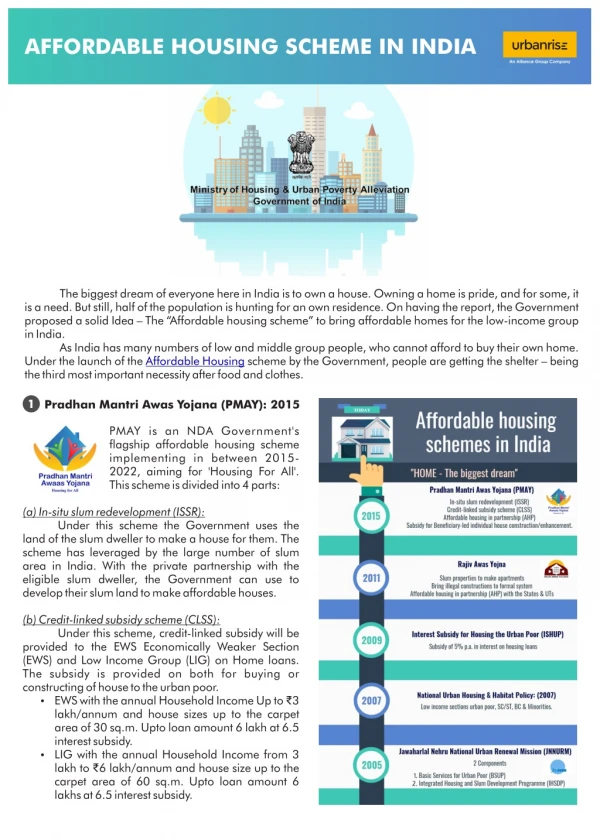

Download

1 / 19

300 likes | 783 Views

Meeting affordable housing demand in india. Venky Panchapagesan IIM, Bangalore. Increasing Demand for Urban Housing. Rapid urbanization fueled by growth opportunities and decline in the role of agriculture Urban housing needs come from: Needs of new and migrant population

E N D

Meeting affordable housing demand in india Venky Panchapagesan IIM, Bangalore

Increasing Demand for Urban Housing • Rapid urbanization fueled by growth opportunities and decline in the role of agriculture • Urban housing needs come from: • Needs of new and migrant population • Changing needs driven by social and economic improvement • Replacement demand due to wear and tear • Not a unique problem to India. • Countries face this issue acutely during their growth stage • Several models have been tried out globally • Need to innovate to take into account local conditions and setup • Need to tackle it NOW!

Urbanization and Economic Growth Source: World Bank

Urban Growth in India By 2050, 900M people will be added to our cities (FICCI, 2011) Source: KPMG, Census

Urban Housing Demand Source: MHUPA, 2011

Our Response So Far • Uncoordinated and too small to make an impact • Large and haphazard urban development • Inability to convert “informal settlements” to “formal settlements” in a meaningful scale • Poor enforcement of development codes • Large unmet customer demand especially for small and low-priced houses • Land price speculation, aided by corruption, making houses unaffordable for low and middle income earners • Financing limited to middle and high-end customers and risk sharing is limited. • Housing industry seems “under-developed and over-regulated” • Policies skewed towards “home ownership” as opposed to “seeking reasonable shelter” • Inadequate appreciation of housing investment as a catalyst for economic and social growth (Harris and Arku (2006))

House Affordability Source: www.numbeo.com, 2013

Why Can’t We Make Low Priced Houses in Large Scale? • Structural causes • Related to land market • Related to financing and risk sharing market • Governance-related causes • Outdated laws/policies • Policies with high negative externalities • Policies that fail to incentivize stakeholders • Procedures whose cost overweigh benefits/redundant procedures

Structural Causes • Poorly developed land market • Inelastic land supply • Large and inefficient distribution of government-owned land • Size diseconomies of privately owned land • Risks from uncertain legal title • Slow and time consuming legal process to resolve disputes • Opaque price discovery • Under-reporting to evade taxes and hide sources • Difficulty in getting secondary market price information

Structural Causes • Poor financing and risk sharing market • Title risk can be difficult to price • Limited market for distressed investments • Mortgage limited to regular income earners • Limited securitization and refinancing • No borrower default insurance • Default recovery process stacked against lenders

Governance-related Causes • Constraining laws • Outdated Rent Control Act • Urban Land Control and Regulation Act • Constraining policies • Issues with land use conversion policies • Issues with floor space creation policies • Constraining procedures • Poor coordination across multiple agencies • Procedures vary by jurisdiction • Redundant procedures

Maximum FSI in Different Cities Source: CPR, Bertaud (2010)

Recent Developments • Government-driven • New legislations (e.g., Land Acquisition Bill, RE Regulatory Bill) • Changes to policies (e.g., Direct and indirect changes to FSI) • More holistic urban development (e.g. JNNURM) • Market-driven • Market for FSI (e.g., Transfer of development rights) • New entrants in low priced developer segment • Improvements in construction technology • New sources of financing (e.g. FDI) • Still much needs to be done….

Focus Areas to Build Capacity • Increase land supply and curb speculation • Develop private enterprise to enhance efficiency • Bolster property rights and improve transparency

Increase Land Supply and Curb Speculation • Unlock government land without losing ownership • Develop rentals/leaseholds on government land (possibly for agencies’ extended stakeholders to start with) • Pilot projects in Tier 2 and Tier 3 cities to iron out model • Increase FSI for low price housing projects • Tax additional FSI development and use it to improve infrastructure • Incentivize FSI increases for rental development • Promote land readjustment schemes • Outsource infrastructure work to speed development • Incentivize development on collateral land left with banks by defaulting borrowers (under SARFAESI) • Taxes on vacant housing

Develop Private Enterprise • Allow private ecosystem to satisfy those who can afford • Streamline procedures to reduce delay (“single window clearance”, insurance scheme for delays) • Personal liability scheme for delays (“Sakala” guaranteed services program in Karnataka) • Provide financial and tax breaks for better technology • Breaks for Green and Sustainable housing development • Provide incentives to corporates to finance development of infrastructure as part of CSR • Incentives for undertaking certain functions • Underwrite risk in mortgages (for customers) and in bond issuances (for developers) through Risk Fund • Underwriting price risk • Certification of developers that can be used to claim subsidies

Delays in Approvals Source: KPMG, Corruption and Transparency in Realty – The Reality

Improve Property Rights and Transparency • Digitize land surveying and titling • Start with urban centres and move to rural areas later • Work with the legal system to quickly clear disputes • Digitize property transaction records • Link land ownership data with national IDs like Aadhaar, PAN card etc. • Make all this information available to public without cost and within reasonable time