Download

1 / 5

50 likes | 61 Views

Small businesses should implement consumer financing and BNPL services on their websites to boost sales and strengthen businesses.<br><br>Contact us<br>Charge After<br>Sales: 888.272.7228 <br>sales@chargeafter.com<br>https://chargeafter.com<br>Support: support@chargeafter.com<br><br><br>

E N D

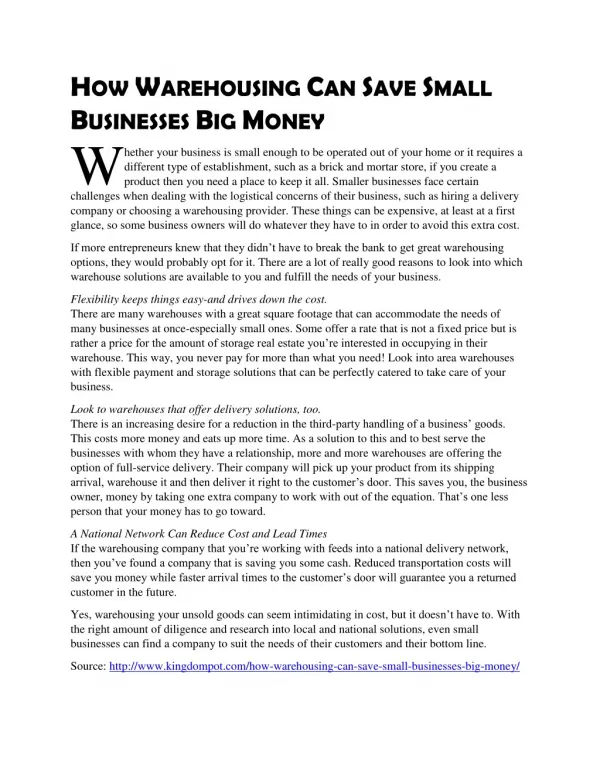

Small businesses how they can offer Small businesses how they can offer Customer Financing Customer Financing If you own a small business, the financial standing of your clients may eventually affect how successful your enterprise is. This is particularly valid if you provide more expensive goods or services. How then can you get customers to check out and finish a sale without having to lower your rates and damage your profit margin? Customer financing is one approach that might be used. The buy-now-pay-later strategy is used by customer finance, which is also known as consumer financing. You have the option of using a third-party financing business or offering financing internally. Customers have the product they desire, and you make sales on full-priced goods and services. This is a win scenario for both customers and business owners. What is Consumer Financing? Consumer financing is a service or program provided by a company to assist customers in making payments over time for goods, services, or products. Financing typically requires filling out an application and doing a credit check to determine the customer's overall credit risk. There are numerous consumer financing options accessible today. Most traditional financial institutions offered those goods, but Fintech businesses have emerged with the availability of POS financing and BNPL loan choices. So, if you own a small business, you have a wide range of funding options to select from.

As was already mentioned, there are several different kinds of financing techniques, but there are primarily two: 1.Primary Financing - refers to finance where a company serves as a lender and provides customers with its own lending program. Compared to third-party financing, primary financing is usually a more time-consuming process for the company. 2.Third-party financing - refers to a form of financing whereby proprietors of small businesses depend on a third-party lender to serve as a creditor at the point of sale. In the majority of these systems, the consumer establishes a payment schedule to pay for a product in full over time, frequently in monthly installments. Unlike other, stricter forms of financing, third-party lending institutions allow a wide variety of credit to be accepted. While some of these financing plans may not charge interest, others may do so at predetermined rates. Both approaches have advantages and disadvantages and can be advantageous for your business. Because of this, ChargeAfter's finance platform, one of the best in the business, enables both financing choices. You can either apply for primary financing, in which case you can use ChargeAfter's financing platform on your website and reap its advantages, or you can use a white-label BNPL solution and use the branded version of BNPL lending. Financing options for small businesses In-House Lending In-house finance might be a suitable option for your business if you sell more expensive items or services. Furniture, electronics, appliances, and home repairs are a few examples of goods and services clients can desire to finance. You will be responsible for covering the costs of credit checks and payment collection for in- house loans, which, as previously indicated, need both manpower and software. Additionally, you must select your conditions for accepting payment arrangements from clients and create a credit policy for your company. BNPL and POS Financing In recent years, businesses of all stripes, especially online retailers, have been more and more interested in third-party consumer finance. Several well-known online third-party lending companies are ChangeAfter, Affirm, AfterPay, and others. These third-party financiers often provide clients with interest-free payment options and permit customers to sign up partial payments against the cost of the things they have purchased. Frequently, biweekly or monthly payments are required for installment contracts. When using third-party consumer finance, you'll either pay a flat monthly fee or a cost for each transaction that is processed for financing. The advantage of working with a third-party

financing firm is that they handle a lot of the work on your behalf, relieving you of the burden of running credit checks or collecting payments. Layaway loans In a layaway payment arrangement, a company holds a product for a client until the customer makes full payment, usually in a series of instalments. In contrast to other forms of financing, a layaway arrangement prevents the consumer from taking possession of the item until the whole purchase price has been made. If the consumer does not finish paying for the item as specified in the layaway agreement, the item will be restored to stock. Depending on the conditions of the agreement, the customer's money may either be forfeited or reimbursed in full, less a fee. Some companies decide to charge a fee for keeping the product on hold while the consumer finishes making their payment. As credit cards became more widely used, layaway's appeal waned but it may still be a viable alternative for some companies and customers. In most cases, a layaway arrangement enables the consumer to avoid interest fees while keeping the item's price stable. Layaway options can be provided to clients with bad credit and lower seller risks. Benefits and Drawbacks of Vonsumer Financing Owners of small businesses should weigh the advantages and disadvantages of providing consumer credit. Below, we've listed some of the advantages and disadvantages. Advantages Advantages Increased AOV - When companies offer customer financing, order sizes rise 15% on average. Larger orders translate into higher sales, which improve your bottom line. Additionally, the buyer gets to get exactly what they want rather than settling for a choice that might not be what they need. Reduce burden - You didn't have to think about managing accounts or dealing with nonpayment problems if you choose to work with a third-party finance provider. Instead, you may concentrate on the expansion of your business and count on more reliable income flow. More Clients, More Sales - Whenever consumers are contemplating whether to make a purchase, the upfront cost and price shock can be a significant challenge. Customers may be able to afford these lower amounts if you can spread out the expense of a good or service over a number of months. The phrase "buy now, pay later" is an excellent strategy to increase sales of both pricey things and significant quantities of less expensive goods.

Disadvantages Interest and Fees - You may probably have to pay fees if you employ a third-party financier. Some companies charge a set monthly fee, while others take a portion of each transaction as their fee. It might be necessary to make manpower and software resource investments in order to offer in-house finance. Payments for Providers - Before you may give financing to clients during the checkouts with some suppliers, you may need to reach a minimum transaction amount. The cost of acquiring customers - Financing is a fantastic way to attract new clients, but the cost might not be justified. After a few months of employing client financing, you should evaluate the return on investment (ROI) to make sure it's the best course of action for your business. Even though these are regarded as drawbacks of consumer financing, if you choose the right provider, you can still avoid them or get better commission fees. The best options for your business to adopt ChargeAfter's platform are provided by their financing platform. The Cost of Financing Depending on the finance service you use, your company model's cost to include consumer financing will vary. You'll be responsible for covering the costs of conducting credit checks and obtaining customer payments for in-house financing. Additionally, processing and finishing those administrative chores would require labor, which will affect your expenditures. You must pay a fee to use third-party financing services. A set monthly fee or a percentage of each transaction's processing cost could be the fee. Conclussion The choice to provide your consumers with a financing program or a range of financing options ultimately rests with you. These financing options can result in increased sales, regardless of whether you use point-of-sale financing from businesses like ChargeAfter, Affirm or Klarna or offer financing internally. About ChargeAfter ChargeAfter is a leading multi-lender platform for Buy Now pay later (BNPL) Consumer Financing. It connects businesses with the most reliable lenders, enabling them to offer customers the greatest financing solutions. With the best system of Waterfall Financing, ChargeAfter guarantees BNPL lending to every shopper, by matching the most relevant lender to every client. Using the unique consumer financing technology, ChargeAfter provides all parties, merchants, lenders, and consumers, with the best shopping experience. Phoenix,

MUFG, VISA, Bradesco, BBVA, Synchrony, PICO Partners, CITI, Propel Venture Partners, Plug and Play, and other companies worldwide are among the investors of ChargeAfter. Contact us Charge After Sales: 888.272.7228 sales@chargeafter.com https://chargeafter.com Support: support@chargeafter.com