Download

1 / 12

120 likes | 292 Views

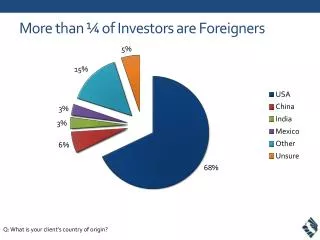

Why Foreign Investors are Smarter than Indian Investors?. Samir Arora Helios Capital Management. December 2010. What is your horizon?. Source: Bloomberg. 2. What is your horizon?. * from 01/01/1993. 3. Indian Investors: Where the H... are you?. * 1.9 billion in January 2008. 4.

E N D

Why Foreign Investors are Smarter than Indian Investors? Samir Arora Helios Capital Management December 2010

What is your horizon? Source: Bloomberg 2

What is your horizon? * from 01/01/1993 3

Indian Investors: Where the H... are you? * 1.9 billion in January 2008 4

Sectoral distribution of various EM countries India has a much more attractive universe 7

Market Cap Growth Decomposition As % of Market Implied Global cap Cap EPS Valuation FX new (20 years) CAGR (real) issuance Australia 2% 3.8% 2.1% 1.0% 0.0% 0.7% Brazil 3% 7.2% 4.5% 0.3% 1.0% 1.3% China 28% 11.5% 6.8% 0.0% 2.3% 2.0% France 3% 5.7% 2.2% 2.6% 0.0% 0.9% Germany 2% 4.1% 1.3% 2.5% 0.0% 0.3% Hong Kong 1% 5.0% 3.5% 0.7% 0.6% 0.1% India 5% 9.2% 6.4% -0.4% 1.9% 1.1% Italy 1% 6.0% 1.1% 4.4% 0.0% 0.4% Japan 3% 2.1% 0.5% 1.5% 0.0% 0.1% Korea 2% 5.5% 3.0% 1.3% 0.7% 0.5% Mexico 1% 7.3% 4.3% -0.1% 1.0% 2.0% Russia 4% 10.2% 3.6% 2.4% 1.6% 2.2% Singapore 1% 4.1% 3.0% 0.3% 0.3% 0.4% Spain 1% 3.2% 0.6% 2.3% 0.0% 0.3% Switzerland 1% 2.8% 1.8% 0.8% 0.0% 0.1% Taiwan 1% 5.0% 3.0% 0.5% 0.7% 0.7% United Kingdom 3% 3.7% 2.2% 1.3% 0.0% 0.2% USA 23% 4.6% 3.0% 1.3% 0.0% 0.2% India: 3rd biggest market in the world by 2030 India’s seductive growth prospects Source: Goldman Sachs Global ECS Report, Sep 2010 8

Indians are missing their own story Demographics: Powerful winds to take India higher • Demographics alone may contribute about 4% of annual GDP growth • India is likely to provide the largest increase to global labor force – estimated an additional 110 m by 2020 • Key trends driving the labor force are: urbanization, more women, large increase in the 30-49 age group. • Age structure is favorable to flows into equities and bonds, and less favorable to bank deposits • Spending on services such as healthcare and education may increase 5-fold • Manufacturing sector has the potential to create the necessary jobs due to various factors Source: Goldman Sachs , Global Economics Paper No: 201, July 2010 9

Indian Market: More up than down SENSEX RETURN (%) Positive Years: 21 (66%) Negative Years: 11 (34%) Percentage Total Return Range Note: Return is FY Ending. 10

“NON ZERO SUM” THEME 1: “NEW” For Private Sector / Compete With Government Of India • India has allowed privatization of sectors w/o privatizing its incumbent government owned companies • Allows private sector companies to win at the cost of government owned companies due to better manpower, product, customer experience, technology, etc • Major Sectors: Infrastructure, Financials (Banking, Insurance), Healthcare, Education “NON ZERO SUM” THEME 2: Factor Cost Advantage • Capitalize on India’s “Global competitiveness” • In these sectors, Indian companies do not yet compete with each other • Major sectors: IT, IT Services, Contract Research, Auto Ancillaries, Apparel Mfr. “NON ZERO SUM” THEME 3: Demographic / Lifestyle Changes • Invest in fast growth “New for India” secular themes • Major sectors: Air conditioning, Wealth Management and Financial Products (incl Stock Exchanges), Mortgage, Retail, Tourism, Cable/Satellite TV, Leisure, Vocational Education, Gaming, Liquor, Branded goods. Investment Strategy: Invest in “Non Zero Sum, under penetrated” themes 11

Mutual Fund Performance * Samir Arora was the Manager of the Fund from inception in March 1996 to July 2003 * Alliance Capital sold its Funds to Birla Sun Life Mutual Fund in 2005 12