Download

1 / 48

480 likes | 788 Views

13.1 Compound Interest. Simple interest – interest is paid only on the principal Compound interest – interest is paid on both principal and interest, compounded at regular intervals

E N D

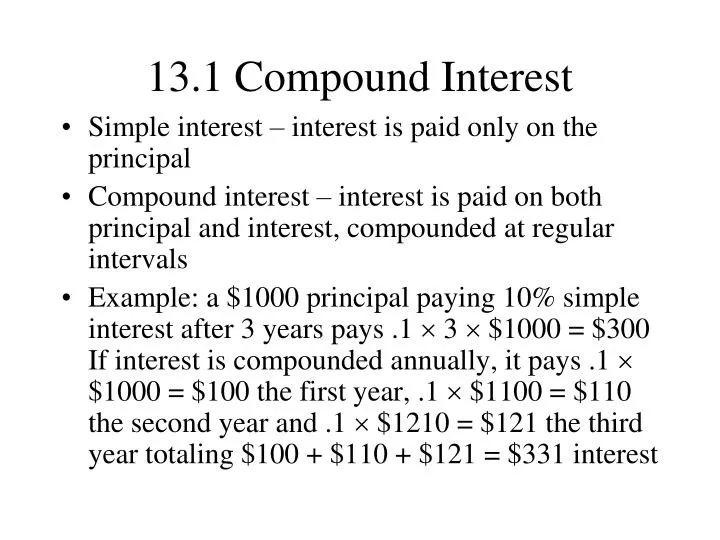

13.1 Compound Interest • Simple interest – interest is paid only on the principal • Compound interest – interest is paid on both principal and interest, compounded at regular intervals • Example: a $1000 principal paying 10% simple interest after 3 years pays .1 3 $1000 = $300If interest is compounded annually, it pays .1 $1000 = $100 the first year, .1 $1100 = $110 the second year and .1 $1210 = $121 the third year totaling $100 + $110 + $121 = $331 interest

13.1 Compound Interest • Compound interest formula:M = the compound amount or future valueP = principali = interest rate per period of compoundingn = number of periodsI = interest earned

13.1 Compound Interest • Time Value of Money – with interest of 5% compounded annually. 2000 2010 2020

13.1 Compound Interest • Example: $800 is invested at 7% for 6 years. Find the simple interest and the interest compounded annually Simple interest:Compound interest:

13.1 Compound Interest • Example: $32000 is invested at 10% for 2 years. Find the interest compounded yearly, semiannually, quarterly, and monthly yearly:semiannually:

13.1 Compound Interest • Example: (continued) quarterly:monthly:

13.2 Daily and Continuous Compounding • Daily compound interest formula: divide i by 365 and multiply n by 365 • Continuous compound interest formula:

13.2 Daily and Continuous Compounding • Time Value of Money – with 5% interest compounded continuously. 2000 2010 2020

13.2 Daily and Continuous Compounding • Example: Find the compound amount if $2900 is deposited at 5% interest for 10 years if interest is compounded daily.

13.2 Daily and Continuous Compounding • Example: Find the compound amount if $1200 is deposited at 8% interest for 11 years if interest is compounded continuously.

13.2 Daily and Continuous Compounding – Early Withdrawal • Early Withdrawal Penalty: • If money is withdrawn within 3 months of the deposit, no interest will be paid on the money. • If money is withdrawn after 3 months but before the end of the term, then 3 months is deducted from the time the account has been open and regular passbook interest is paid on the account.

13.2 Daily and Continuous Compounding – Early Withdrawal • Example: Bob Kashir deposited $6000 in a 4-year certificate of deposit paying 5% compounded daily. He withdrew the money 15 months later. The passbook rate at his bank is 3½ % compounded daily. Find his amount of interest.Bob receives 15-3 = 12 months of 3.5 % interest compounded daily

13.3 Finding Time and Rate • Given a principal of $12,000 with a compound amount of $17,631.94 and interest rate of 8% compounded annually, what is the time period in years?From Appendix D table pg 805( i = 8%) we find that n = 5 years

13.3 Finding Time and Rate • Example:Find the time to double your investment at 6%.If you try different values of n on your calculator, the value that comes closest to 2 is 12. Therefore the investment doubles in about 12 years.

13.3 Finding Time and Rate • Example:Given an investment of $13200, compound amount of $22680.06 invested for 8 years, what is the interest rate if interest is compounded annually?From Appendix D table pg 803( i = 7%) we find that for n=8, column A = 1.71818… so i = 7%.

13.4 Present Value at Compound Interest • Example:Given an amount needed (future value) of $3300 in 4 years at an interest rate of 11% compounded annually, find the present value and the amount of interest earned.

13.4 Present Value at Compound Interest • Example: Assume that money can be invested at 8% compounded quarterly. Which is larger, $2500 now or $3800 in 5 years?First find the present value of $3800, then compare present values:

14.1 Amount (Future Value) of an Annuity • Annuity – a sequence of equal payments • Payment period – time between payments • “Ordinary annuity” – payments at the end of the pay period • “Annuity due” - payments at the beginning of the pay period • “Simple annuity” – payment dates match the compounding period (all our annuities are simple)

14.1 Amount (Future Value) of an Annuity • Amount of an annuity - S (future value) of n payments of R dollars for n periods at a rate of i per period: • Use you calculator instead of using appendix D.

14.1 Amount (Future Value) of an Annuity • Example: Sharon Stone deposits $2000 at the end of each year in an account earning 10% compounded annually. Determine how much money she has after 25 years. How much interest did she earn?

14.1 Amount (Future Value) of an Annuity • Example: For S = $50,000, i = 7% compounded semi-annually with payments made at the end of each semi-annual period for 8 years, find the periodic payment (R)

14.1 Amount (Future Value) of an Annuity • Example: For S = $21,000, payments (R) of $1500 at the end of each 6-month period i = 10% compounded semi-annually. Find the minimum number of payments to accumulate 21,000.Trying different values for n, the expression goes over 14 when n = 11 (Exact value = 4.20678716(1500)=$21310.18)

14.1 Amount of an Annuity Due • An annuity due is paid at the beginning of each period instead of at the end. It is essentially the same as an ordinary annuity that starts a period early but without the last payment. • To solve such a problem: • Add 1 to the number of periods for the computation. • After calculating the value for S, subtract the last payment.

14.1 Amount of an Annuity Due • Example:Sharon Stone deposits $500 at the beginning of each 3 months in an account earning 10% compounded quarterly. Determine how much money she has after 25 years

14.2 Present Value of an Annuity • Present value of an annuity (A) made up of payments of R dollars for n periods at a rate of i per period:

14.2 Present Value of an Annuity • Example: What lump sum deposited today would allow payments of $2000/year for 7 years at 5% compounded annually?

14.2 Present Value of an Annuity • Example: Kashundra Jones plans to make a lump sum deposit so that she can withdraw $3,000 at the end of each quarter for 10 years. Find the lump sum if the money earns 10% per year compounded quarterly.

14.3 Sinking Funds • Sinking fund – a fund set up to receive periodic payments.The purpose of this fund is to raise an amount of money at a future time. • Bond – promise to pay an amount of money at a future time.(Sinking funds can be set up to cover the face value of bonds.)

14.3 Sinking Funds • Amount of a sinking fund payment: • Same formula as in section 14.1, except solved for the variable R.

14.3 Sinking Funds • Example: 15 semiannual payments are made into a sinking fund at 7% compounded semiannually so that $4850 will be present. Find the amount of each payment rounded to the nearest cent.

14.3 Sinking Funds • Example: A retirement benefit of $12,000 is to be paid every 6 months for 25 years at interest rate of 7% compounded semi-annually. Find (a) the present value to fund the end-of-period retirement benefit. ): (b) the end-of-period semi-annual payment needed to accumulate the value in part (a) assuming regular investments for 30 years in an account yielding 8% compounded semi-annually.

14.3 Sinking Funds • Example(part b) – amount to save every 6 months for 30 years for this annuity

15.1 Open-End Credit • Open-end credit – the customer keeps making payments until no outstanding balance is owed (e.g. charge cards such as MasterCard and Visa) • Revolving charge account – a minimum amount must be paid …account might never be paid off • Finance charges – charges beyond the cash price, also referred to as interest payment • Over-the-limit fee – charged if you exceed your credit limit

15.1 Open-End Credit • Example: Find the finance charge for an average daily balance of $8431.10 with monthly interest rate of 1.4%finance charge

15.1 Open-End Credit • Example: Find the interest for the following account with monthly interest rate of 1.5%

15.1 Open-End Credit • Example(continued) • Average balance = 10246.930 = $341.56 • Finance charge = .015 341.56 = $5.12 • Balance at end = 346.98 + 5.12 = $352.10

15.2 Installment Loans • A loan is “amortized” if both principal and interest are paid off by a sequence of periodic payments.For a house this is referred to as mortgage payments. • Lenders are required to report finance charge (interest) and their annual percentage rate (APR) • APR is the true effective annual interest rate for a loan

15.2 Installment Loans • In order to find the APR for a loan paid in installments, the total installment cost, finance charge, and the amount financed are needed • Total installment cost = Down payment + (amount of each payment number of payments) • Finance charge = total installment cost – cash price • Amount financed = cash price – down payment • Get: • Use table 15.2 to get the APR

15.2 Installment Loans • Example: Given the following data, find the finance charge and the total installment costTotal installment cost Finance charge

15.2 Installment Loans • Example: Given the following data, find the annual percentage rate using table 15.2from table 15.2 # payments = 12, APR is approximately 13%

15.3 Early Payoffs of Loans • United States rule for early payoff of loans: • Find the simple interest due from the date the loan was made until the date the partial payment is made. • Subtract this interest from the amount of the payment. • Any difference is used to reduce the principal • Treat additional partial payments the same way, finding interest on the unpaid balance

15.3 Early Payoffs of Loans • Example: Given the following note, find the balance due on maturity and the total interest paid on the note. • Find the simple interest for 60 days and subtract it from the payment. • Subtract it from the payment: • Reduce the principal by the amount from (2)

15.3 Early Payoffs of Loans • Example(continued)… Interest due at maturity:Balance due on maturity (add reduced principal to interest):Total interest paid on the note (add interest paid to interest due at maturity):

15.3 Early Payoffs of Loans • Rule of 78 (sum-of-the-balances method)Note (1+2+3+…+12) – sum of the month numbers adds up to 78 … used to derive the formula.U = unearned interest, F = finance charge, N = number of payments remaining, and P = total number of payments

15.4 Personal Property Loans • From section 14.2, the present value of an annuity (A) made up of payments of R dollars for n periods at a rate of i per period:

15.4 Personal Property Loans • A loan is made for $3500 with an interest rate of 9% and payments made annually for 4 years. What is the payment amount?

15.4 Personal Property Loans • A loan is made for $4800 with an APR of 12% and payments made monthly for 24 months. What is the payment amount? What is the finance charge?