Download

1 / 18

180 likes | 196 Views

This briefing note presents audit findings on the financial statements of the Department of Social Development, NDA, and SASSA in South Africa. It highlights qualification issues and unqualified opinions for different entities within the Social Security Cluster. The note also covers irregular expenditures and accounting policies.

E N D

Audit Outcomes 2009-10 Social Security Cluster 12 October 2010 Presented by: Musa Hlongwa and Abrie Adendorff AGSA team responsible for Social Development

Reputation promise/mission The Auditor-General has a constitutional mandate and, as the Supreme Audit Institution (SAI) of South Africa, it exists to strengthen our country’s democracy by enabling oversight, accountability and governance in the public sector through auditing, thereby building public confidence.

PART 1Introduction The purpose of the briefing note is to provide an insight by the Auditor-General South Africa into the issues resulting in the audit opinion on the financial statements of the Department of Social Development (DSD), National Development Agency (NDA) and the South African Social Security Agency (SASSA). The mission of the Department is to ensure the provision of comprehensive social protection services against vulnerability and poverty within the constitutional and legislative framework, and create an enabling environment for sustainable development. The Department further aims to deliver integrated, sustainable and quality services, in partnership with all those committed to building a caring society.

The activities of the Department The activities of the department are organised under the following five programmes:

The Social Development portfolio consist of the following entities: • Department of Social Development (DSD) – Vote No. 16 • South African Social Security Agency (SASSA) – Audit still in progress • National Development Agency (NDA) • Funds under the umbrella of DSD • Disaster Relief Fund • Social Relief Fund • Refugee Relief Fund • State President fund • High School Vorentoe Disaster Fund

Funding of the entities • Department of Social Development – Budgeted amount 09/10 – R86 508 187 000 (included in this amount is the amount for households – R79 259 748 000,programme 2 – Comprehensive social security, that is transferred to SASSA) • National Development Agency – R144 782 000 (transferred from DSD) • SASSA – R5 168 896 000 (transferred from DSD) • Funds – these funds are dormant and no funds are transferred to it

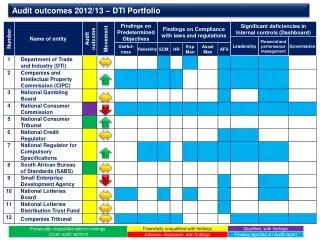

Audit Outcomes 2009-10 Summary of audit opinions(SASSA excluded for 2009/10) 3

2009-10 QUALIFICATION ISSUES • The Department of Social Development • The Department has been qualified on Transfers and Subsidies due to limitations placed on the audit by its agent, SASSA. • Transfer to Households: • 2160 Grant beneficiary files were selected for audit purposes. • 70 Files representing 3.24% of the sample were not presented for audit. • This extrapolated to the population based on grant type and province amounted to R 4,937,166,865.29 • Furthermore, of the 2090 files that were received, 191 files did not contain the documentation that is necessary for the beneficiary to receive the grant. This represents 8.8% of the sample and extrapolated to the population based on grant type and province amounted to R 5,659,286,161.10 • This resulted in a total scope limitation of R 10,596,453,026.39 • Management attests that the documentation is with SASSA however, it can neither be located nor retrieved due to their poor file management.

2009-10 QUALIFICATIONS The South African Social Security Agency SASSA has had an unqualified audit opinion for the prior 2 years and we are currently performing the audit for the 2009-10 financial year due to late submission of annual financial statements by SASSA. The National Development Agency The NDA has had an unqualified audit opinion for the prior 2 years and for the 2009-10 financial year. The 5 DSD Funds All the funds have had unqualified audit opinions for the prior 2 years and for the 2009-10 financial year.

Other Audit Report Matters Emphasis of Matter Basis of Accounting (DSD) • The department’s policy is to prepare financial statements on the modified cash basis of accounting determined by National Treasury as described in accounting policy note 1.1. Irregular expenditure (NDA) • As disclosed in note 31 to the financial statements, irregular expenditure to the amount of R881 819 was incurred, as proper procurement process had not been followed. Additional Matters Flow of funds (DSD) • As indicated in the report of the Accounting Officer, despite the social assistance grant expenditure being reported in the annual financial statements of the Department of Social Development, a dual accountability relationship exists between the Department and SASSA over the social assistance grants. The status of the current relationship therefore results in actions of SASSA having an impact on the audit report of the Department regarding matters concerning social assistance grant expenditure.

REPORT ON OTHER LEGAL AND REGULATORY REQUIRMENTS PREDETERMINED OBJECTIVES There were no findings on Audit of Predetermined Objectives for entities in the social services cluster. COMPLIANCE WITH LAWS AND REGULATIONS There were no significant non-compliance with laws and regulations for the entities in the social services cluster.

INTERNAL CONTROLS Leadership (DSD) • Due to the legislative reporting lines, the oversight responsibility fulfilled by the Department does not focus on the detail of the operational function performed by its agency, SASSA, which cascades down to the management of SASSA and its operational staff. • The accountability lines between the Department and SASSA are not clearly defined resulting in uncertain responsibility and accountability over the social assistance grant expenditure. • SASSA fulfilled its mandate of the distribution of social assistance grants in terms of its agent relationship on behalf of the Department. The social assistance grants distributed by SASSA are reported and disclosed within the financial statements of the Department and therefore the deficiencies identified at SASSA with regard to the social assistance grant expenditure are listed below: • Leadership • Quality is not understood by all to be a prerequisite and is not embedded in the entity’s values. • Performance is not measured. • The accounting authority does not exercise oversight responsibility over reporting and compliance with laws and regulations and internal control. • The commitment to quality is not communicated. • Control weaknesses are not analysed, and appropriate follow-up actions are not taken to address root causes.

INTERNAL CONTROLS (CONTINUED) • Financial and performance management • Requested information relating to the social assistance grant expenditure was not available and was not supplied without any significant delay. • General information technology controls relating to the SOCPEN system were not designed to maintain the integrity of the information systems and the security of the data. • Manual or automated controls relating to the social assistance grant expenditure were not designed to ensure that the transactions have occurred, are authorised, and are completely and accurately processed. • Governance • Internal controls were not selected and developed to prevent / detect and correct material misstatements in financial reporting and reporting on predetermined objectives.

OTHER REPORTS Investigations (DSD) • Investigations in progress included investigations undertaken by SASSA on the social assistance grant expenditure. As part of the effort made to clean up the social security database and reclaim amounts owing to the state, SASSA contracted the Special Investigations Unit (SIU) to manage, investigate and prosecute individuals identified in fraudulent activities within the social security system. • These investigations were still ongoing as at the date of this report. Performance audit (NDA) • A report to Parliament on a performance audit of projects that are funded by the National Development Agency was tabled in November 2009.