Download

1 / 44

440 likes | 634 Views

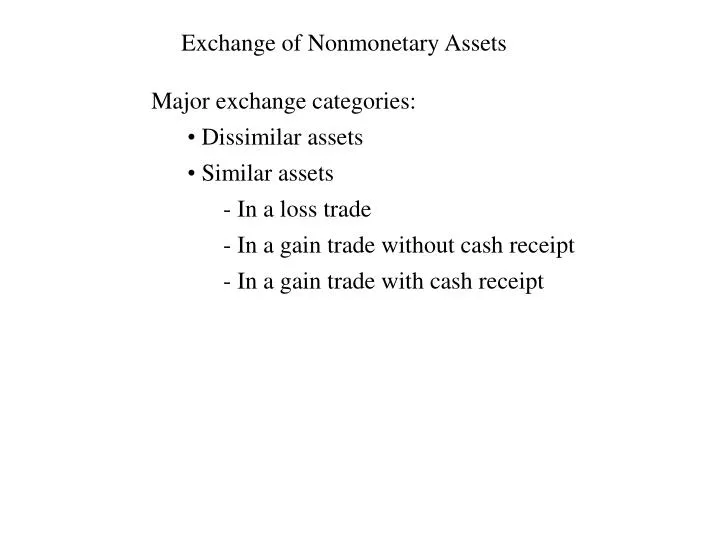

Exchange of Nonmonetary Assets. Major exchange categories: Dissimilar assets Similar assets In a loss trade In a gain trade without cash receipt In a gain trade with cash receipt. Exchange of Nonmonetary Assets. Major exchange categories: Dissimilar assets Similar assets

E N D

Exchange of Nonmonetary Assets • Major exchange categories: • Dissimilar assets • Similar assets • In a loss trade • In a gain trade without cash receipt • In a gain trade with cash receipt

Exchange of Nonmonetary Assets • Major exchange categories: • Dissimilar assets • Similar assets • In a loss trade • In a gain trade without cash receipt • In a gain trade with cash receipt Similarity refers to use or function within the line of business activity

Exchange of Nonmonetary Assets Case 1: Dissimilar Assets

Exchange of Nonmonetary Assets Case 1: Dissimilar Assets • Asset acquired recorded at FMV of asset given up • Gain or loss recorded at difference between • FMV of asset given up and BV of asset given up

Exchange of Nonmonetary Assets Case 1: Dissimilar Assets Example Crane given up: Original cost $50,000 Accum. Depr. $40,000 FMV $12,000 Truck received: FMV $13,200

Exchange of Nonmonetary Assets Case 1: Dissimilar Assets Example Crane given up: Original cost $50,000 Accum. Depr. $40,000 FMV $12,000 Truck received: FMV $13,200 Acquired truck valued at FMV of Crane given up: $12,000

Exchange of Nonmonetary Assets Case 1: Dissimilar Assets Example Crane given up: Original cost $50,000 Accum. Depr. $40,000 FMV $12,000 Truck received: FMV $13,200 Acquired truck valued at FMV of Crane given up: $12,000 Gain is recognized for difference between FMV of Crane and BV of Crane

Exchange of Nonmonetary Assets Case 1: Dissimilar Assets Example Crane given up: Original cost $50,000 Accum. Depr. $40,000 FMV $12,000 BV = $10,000 Truck received: FMV $13,200 Acquired truck valued at FMV of Crane given up: $12,000 Gain is recognized for difference between FMV of Crane and BV of Crane Gain = $12,000 – 10,000 = $2,000

Exchange of Nonmonetary Assets Case 1: Dissimilar Assets Example Journal entry: Accum. Depr., Crane 40,000 Crane 50,000 First, take the Crane off the books.

Exchange of Nonmonetary Assets Case 1: Dissimilar Assets Example Journal entry: Accum. Depr., Crane 40,000 Crane 50,000 Gain on Crane disposal 2,000 Then, record the gain on the transaction.

Exchange of Nonmonetary Assets Case 1: Dissimilar Assets Example Journal entry: Truck 12,000 Accum. Depr., Crane 40,000 Crane 50,000 Gain on Crane disposal 2,000 Finally, record the value of the new truck. Note that this is the FMV of the Crane given up (not FMV of the truck received).

Exchange of Nonmonetary Assets Case 2: Similar Assets in a Loss Trade

Exchange of Nonmonetary Assets Case 2: Similar Assets in a Loss Trade This will naturally occur when the fair market value of the asset given up is below its book value

Exchange of Nonmonetary Assets Case 2: Similar Assets in a Loss Trade • Asset acquired recorded at FMV of asset(s) given up • Loss recorded at difference between FMV of asset(s) • given up and BV of asset(s) given up

Exchange of Nonmonetary Assets Case 2: Similar Assets in a Loss Trade Example Car traded-in: Original cost $20,000 Accum. Depr. $10,000 FMV $9,000 Car received: FMV $13,000

Exchange of Nonmonetary Assets Case 2: Similar Assets in a Loss Trade Example Car traded-in: Original cost $20,000 Accum. Depr. $10,000 FMV $9,000 BV = $10,000 Car received: FMV $13,000 Note that we expect a loss of $1,000

Exchange of Nonmonetary Assets Case 2: Similar Assets in a Loss Trade Example Car traded-in: Original cost $20,000 Accum. Depr. $10,000 FMV $9,000 BV = $10,000 Car received: FMV $13,000 Note also that the dealer will expect us to pay $4,000 cash to make up for FMV shortfall. (He is only willing to give us FMV credit for our trade-in).

Exchange of Nonmonetary Assets Case 2: Similar Assets in a Loss Trade Example Journal entry: Accum. Depr., Old Car 10,000 Old Car 20,000 First, remove the old car from the books.

Exchange of Nonmonetary Assets Case 2: Similar Assets in a Loss Trade Example Journal entry: Loss on disposal, Old Car 1,000 Accum. Depr., Old Car 10,000 Old Car 20,000 Cash 4,000 Second, record the cash disbursement and the loss on disposal.

Exchange of Nonmonetary Assets Case 2: Similar Assets in a Loss Trade Example Journal entry: New Car 13,000 Loss on disposal, Old Car 1,000 Accum. Depr., Old Car 10,000 Old Car 20,000 Cash 4,000 Finally, record the new car. Notice that the value ends up being the equivalent to FMV of car given up ($9,000) + FMV of cash given up ($4,000).

Exchange of Nonmonetary Assets Case 3: Similar Assets in a Gain Trade without cash receipt

Exchange of Nonmonetary Assets Case 3: Similar Assets in a Gain Trade without cash receipt The gain is deferred until the new asset is sold.

Exchange of Nonmonetary Assets Case 3: Similar Assets in a Gain Trade without cash receipt The gain is deferred until the new asset is sold. New asset recorded at BV of asset(s) given up.

Exchange of Nonmonetary Assets Case 3: Similar Assets in a Gain Trade without cash receipt example

Exchange of Nonmonetary Assets Case 3: Similar Assets in a Gain Trade without cash receipt example House given up: Original cost $200,000 Accum. Depr. $30,000 FMV $250,000 BV = $170,000 • House received: • FMV $265,000 Note that we expect a gain of $80,000.

Exchange of Nonmonetary Assets Case 3: Similar Assets in a Gain Trade without cash receipt example House given up: Original cost $200,000 Accum. Depr. $30,000 FMV $250,000 BV = $170,000 • House received: • FMV $265,000 Note that we expect a gain of $80,000. But this gain will be deferred since this is an exchange of similar assets without cash receipt.

Exchange of Nonmonetary Assets Case 3: Similar Assets in a Gain Trade without cash receipt example House given up: Original cost $200,000 Accum. Depr. $30,000 FMV $250,000 BV = $170,000 • House received: • FMV $265,000 Note also that we will need to pay $15,000 cash to make up for FMV shortfall.

Exchange of Nonmonetary Assets Case 3: Similar Assets in a Gain Trade without cash receipt example Journal entry: Accum. Depr., Old House 30,000 Old House 200,000 First, remove the old house from the books.

Exchange of Nonmonetary Assets Case 3: Similar Assets in a Gain Trade without cash receipt example Journal entry: Accum. Depr., Old House 30,000 Old House 200,000 Cash 15,000 Next, record the cash disbursement.

Exchange of Nonmonetary Assets Case 3: Similar Assets in a Gain Trade without cash receipt example Journal entry: New House 185,000 Accum. Depr., Old House 30,000 Old House 200,000 Cash 15,000 Finally, record the value of the new house. Notice that this is equivalent to the book value of the old house ($170,000) + the book value of the cash given up ($15,000). Also notice that there is no gain recorded.

Exchange of Nonmonetary Assets Case 4: Similar Assets in a Gain Trade with cash receipt

Exchange of Nonmonetary Assets Case 4: Similar Assets in a Gain Trade with cash receipt Note that this is different than the prior case, when cash was given to make up for FMV shortfall.

Exchange of Nonmonetary Assets Case 4: Similar Assets in a Gain Trade with cash receipt When cash is received, the transaction is considered part sale and part exchange. So, a partial gain must be recognized.

Cash Received Recognized gain = x total gain FMV asset(s) received + Cash Received Exchange of Nonmonetary Assets Case 4: Similar Assets in a Gain Trade with cash receipt When cash is received, the transaction is considered part sale and part exchange. So, a partial gain must be recognized.

Exchange of Nonmonetary Assets Case 4: Similar Assets in a Gain Trade with cash receipt example House given up: Original cost $200,000 Accum. Depr. $30,000 FMV $250,000 BV = $170,000 • House received: • FMV $225,000 Note that we expect a gain of $80,000.

Exchange of Nonmonetary Assets Case 4: Similar Assets in a Gain Trade with cash receipt example House given up: Original cost $200,000 Accum. Depr. $30,000 FMV $250,000 BV = $170,000 • House received: • FMV $225,000 Note also that we will expect to receive $25,000 cash to make up for FMV shortfall.

Exchange of Nonmonetary Assets Case 4: Similar Assets in a Gain Trade with cash receipt example House given up: Original cost $200,000 Accum. Depr. $30,000 FMV $250,000 BV = $170,000 • House received: • FMV $225,000 Note also that we will expect to receive $25,000 cash to make up for FMV shortfall. Therefore, some portion of the $80,000 gain will be recognized. The remainder will be deferred.

Cash Received Recognized gain = x total gain FMV asset(s) received + Cash Received Exchange of Nonmonetary Assets Case 4: Similar Assets in a Gain Trade with cash receipt example First, compute recognized gain:

Cash Received Recognized gain = x total gain FMV asset(s) received + Cash Received Exchange of Nonmonetary Assets Case 4: Similar Assets in a Gain Trade with cash receipt example First, compute recognized gain: $25,000 x $80,000 = $225,000 + $25,000

Cash Received Recognized gain = x total gain FMV asset(s) received + Cash Received Exchange of Nonmonetary Assets Case 4: Similar Assets in a Gain Trade with cash receipt example First, compute recognized gain: $25,000 x $80,000 = $225,000 + $25,000 = $8,000

Exchange of Nonmonetary Assets Case 4: Similar Assets in a Gain Trade with cash receipt example Journal entry: Accum. Depr., Old House 30,000 Old House 200,000 First, remove the old house from the books.

Exchange of Nonmonetary Assets Case 4: Similar Assets in a Gain Trade with cash receipt example Journal entry: Cash 25,000 Accum. Depr., Old House 30,000 Old House 200,000 Gain on Exchange Transaction 8,000 Then, record the partial gain you just calculated for the transaction and the cash you received for the transaction.

Exchange of Nonmonetary Assets Case 4: Similar Assets in a Gain Trade with cash receipt example Journal entry: New House 153,000 Cash 25,000 Accum. Depr., Old House 30,000 Old House 200,000 Gain on Exchange Transaction 8,000 Finally, record the new house. Note that the new house is valued at the book value of the house given up ($170,000) minus the cash received ($25,000) plus the gain recognized ($8,000).

Exchange of Nonmonetary Assets Case 4: Similar Assets in a Gain Trade with cash receipt example Journal entry: New House 153,000 Cash 25,000 Accum. Depr., Old House 30,000 Old House 200,000 Gain on Exchange Transaction 8,000 Finally, record the new house. Note that the new house is valued at the book value of the house given up ($170,000) minus the cash received ($25,000) plus the gain recognized ($8,000). Another way to look at it: the new house is valued at its FMV ($225,000) minus the gain deferred on the transaction ($72,000).