Download

1 / 31

310 likes | 492 Views

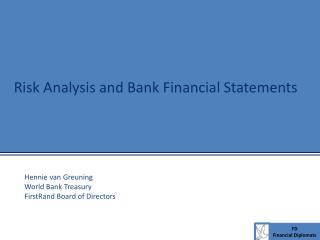

Unified Financial Analysis Risk & Finance Lab. Chapter 11: Risk Willi Brammertz / Ioannis Akkizidis. Risk. Risk intuitively explained. Rate. V A. Risk. V L. σ r. Time. t L. t A. Δ t. Δ t. σ r. The 2 main dimensions of interest rate risk are:. Interest rate gap. 4. 1. 5. 2.

E N D

Unified Financial Analysis Risk & Finance Lab Chapter 11: Risk Willi Brammertz / Ioannis Akkizidis

Risk intuitively explained Rate VA Risk VL σr Time tL tA Δ t • Δ t • σr The 2 main dimensions of interest rate risk are:

Interest rate gap 4 1 5 2 6 3 t0 Time Assets Liabilities Gap measures Δ T (Sensitivity gap)

Risk and sensitivity • General definition • Example: Interest rate risk Risk per unit of asset = Sensitivity * Risk factor volatility Δ NPV= NPV · Dur ·Δ r= $DUR ·Δ r σ NPV= NPV · Dur ·σr = $DUR ·σr

Is risk = VaR? • No, VaR is subset of risk measures • Alternative measures: e.g. • Expected shortfall • Regulatory measures • Alternative techniques: e.g. Stress scenarios

Critique on VaR • Losses beyond the confidence interval not taken into account • No sub-additivity • Focus on market value only • Sensitivity only linear approximation (parametric VaR)

Critical voices • Taleb: “… VAR is charlatanism, a dangerously misleading tool – like much of modern mathematised academic finance” • Turner report: “… misplaced reliance on sophisticated mathematics, which, once irrational exuberance disappeared, contributed to a collapse …” and “Mathematical sophistication ended up not containing risk, but providing false assurance that other prima facie indicators of increasing risk (e.g. rapid credit extension and balance sheet growth) could be safely ignored”

Critical voices • Keynes:“Too large a proportion of recent “mathematical” economics are mere concoctions, as imprecise as the initial assumptions they rest on, which allow the author to lose sight of the complexities and interdependencies of the real world in a maze of pretentious and unhelpful symbols” (General Theory, p.298)

CreditRisk+, assumptions • 1 year horizon • Net exposure per obligor (LGDi) • Expected long term default ~pi • Variance of default σi = pi *σ • States of sectors Sk • Risk allocation Θik

CreditRisk+, easy explanation • This is a Monte Carlo like explanation (However CreditRisk+ is analytic)

CreditRisk+, interpretation Risk-margin Risk-capital

CreditMetricsCorrelation • Helper variable Xi (for obligor i) • εk is ideally a sector index (market correlated) • Weights

Discounted recovery Discounted loss PD 1 PD 2 PD 3 Impairment II Exposure Maturity date Principal Interest Bucket 1 Bucket 2 Bucket 3 expected loss = discounted loss – discounted recovery Valuation under Default and for Derivatives Today Loss Valuation date

Liquidity and liquidity risk • Funding (structural, idiosyncratic) liquidity • Problem: Cash outflow > inflow • Risk incurred due to internal factors • Needs cash flow control (chapter 8) • Liquidity Gap analysis for basic analysis • Static analysis combined with behavioral stresses (ch 11.5) • Market liquidity: External factors affecting liquidity • Problem: Money stops flowing between actors • Risk incurred due to external factors • Related to credit risk • Dynamic analysis (chapter 14.4)

FSA Liquidity risk requirements Funding liquidity • Funding • Behaviour • Sales • Prepayments • Market liquidity • Spreads and Liquidity • Sales and Repos • Target variable: Survival period Market liquidity 22

Other risks • Earning at risk: • Focus on earning instead of value • Makes no sense in a static environment • Insurance risk: Static makes little sense (although some method proposed by Solvency II) • Operational risk: The other animal (Chapter 12)

Static stress testing • A stress test is a shift in one or more of the risk factors • Market stress • Credit stress • Liquidity stress Yield Time to Maturity AAA AA A ... 1M 10% 3M 10% 6M 15% 1Y 25% >1Y 40% A BBB BB ... 20% 40% 30% 10%

Rating and collateral • Credit ratings are often a combination of probability of default, collateral and recovery • Each of these categories has different „statistical qualtiy“ • Therefore they should not be confounded into a single measure • Rating should only reflect probability of default = uncollateralized rating

Spreads and collateral • Same problem applies to spreads • How much collateral is assumed? -> Not known • Better: Strict uncollateralized spreads