Download

1 / 19

190 likes | 297 Views

Is There a “Global Saving Glut”? And Is It the Cause of the US Current Account Deficit?. Menzie D.Chinn University of Wisconsin and NBER. Presentation at NABE Panel “International Capital Flows” ASSA, Chicago, January 6, 2007. Anticipating the Answers. Maybe (better investment drought)

E N D

Is There a “Global Saving Glut”?And Is It the Cause of the US Current Account Deficit? Menzie D.Chinn University of Wisconsin and NBER Presentation at NABE Panel “International Capital Flows” ASSA, Chicago, January 6, 2007

Anticipating the Answers • Maybe (better investment drought) • Maybe

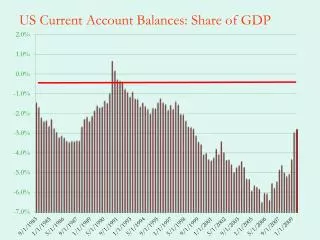

Too Obvious a Question? • Long term real rates are low • The U.S. CA deficit seems anomalously large • The East Asian surpluses appear anomalously large

Are Real Long Term Rates and the CA Moving Together? Note: 10 yr const. mat adjusted by Livingstone, Blue Chip, SPF 10 year expected infl.

US Long Term Real Rates Source: St. Louis Fed, Philadelphia Fed

World Real RatesInflation indexed Source: BIS, St. Louis Fed

Is the US Deficit Too Large? • Panel regression approach • 1971-2004, 21 industrial, 97 developing countries (WDI), in five year panels • Include time fixed effects • X are macro variables • Z are financial development, institutional variables (credit; law & order) Source: M.Chinn & H. Ito, “Assaying the World Saving Glut”,http://www.ssc.wisc.edu/~mchinn/CA_Chinn_Ito.pdf

Is the US Deficit Too Large? • Short answer: Barely, according to statistical level • Budget deficit is important

Reality Check Between 2000 and 2005, there was approximately a 4.3 percentage point swing in the US Federal budget balance, and a 2.2 percentage point swing in the U.S. current account balance. This outcome is consistent with a 0.5 coefficient.

NSUS’ REAsia NSEAsia RUS IUS IEAsia NSUS R0 R1 CA1EAsia > 0 CA1US < 0 How Can Low Rates and Imbalances Be Reconciled?

Ending Thoughts • Most of the debate has been cast in identities, or simple bivariate relationships • Chinn-Ito quantify the uncertainty surrounding the CA balance relationship • There is something to the saving glut story • But there is also a role for budget deficits • Financial development may or may not help reduce the saving glut