Download

1 / 9

90 likes | 225 Views

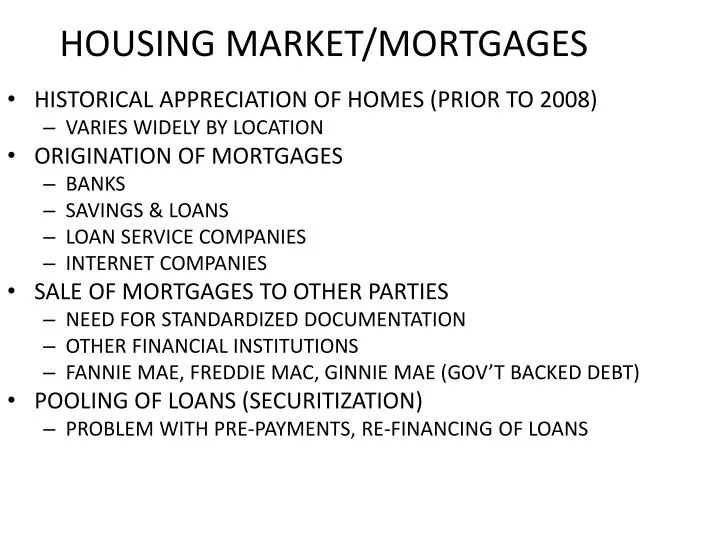

HOUSING MARKET/MORTGAGES. HISTORICAL APPRECIATION OF HOMES (PRIOR TO 2008) VARIES WIDELY BY LOCATION ORIGINATION OF MORTGAGES BANKS SAVINGS & LOANS LOAN SERVICE COMPANIES INTERNET COMPANIES SALE OF MORTGAGES TO OTHER PARTIES NEED FOR STANDARDIZED DOCUMENTATION

E N D

HOUSING MARKET/MORTGAGES • HISTORICAL APPRECIATION OF HOMES (PRIOR TO 2008) • VARIES WIDELY BY LOCATION • ORIGINATION OF MORTGAGES • BANKS • SAVINGS & LOANS • LOAN SERVICE COMPANIES • INTERNET COMPANIES • SALE OF MORTGAGES TO OTHER PARTIES • NEED FOR STANDARDIZED DOCUMENTATION • OTHER FINANCIAL INSTITUTIONS • FANNIE MAE, FREDDIE MAC, GINNIE MAE (GOV’T BACKED DEBT) • POOLING OF LOANS (SECURITIZATION) • PROBLEM WITH PRE-PAYMENTS, RE-FINANCING OF LOANS

CAUSE OF HOUSE INFLATION • SUPPLY/DEMAND • Job availability • Salaries • Interest rates • Credit terms • Material costs • Labor costs • Regulations • Commuting premium

TYPES OF MORTGAGES • Fixed – 15 year, 30 year • Adjustable – 3/30, 7/30 • Assumable • Non-Assumable • Government Backed (FHA, VA) • Conventional • Prime • Sub-Prime

HOME EQUITY LOANS • As home appreciates – get loan for other uses. • Reduces equity in home • Liens on property – 2nd, 3rd • Shorter term than mortgage • Line of credit • Less complicated than re-finance

CAUSES OF HOUSING CRISIS –2008 • LOOSE CREDIT REQUIREMENTS • INFLATED HOME PRICES (GROWTH OF EQUITY) • USE OF EQUITY LOAN FUNDS FOR NON-HOME RELATED EXPENDITURES • UNEMPLOYMENT • CREDIT DEFAULT SWAPS

HOUSING CRISIS EXAMPLE PURCHASE OF HOUSE – YEAR 1 Selling Price -- $150,000 Down Payment -- 5% Loan Amount -- $142,500 Loan Terms-- 6%, 30 year fixed P & I Payments -- $854 month Salary -- $50,000 year MORTGAGE PAYMENT -- $1,184 month Percent of Gross Pay -- 28% Percent of Take-Home Pay 34%

AFTER 2 YEARS Appraisal Price -- $200,000 Home Equity Balance -- $ 61,000 Home Equity Loan -- $ 25,000 Loan Terms -- 8%, 10 years fixed Loan Payment -- $303 month Salary -- $ 53,000 year TOTAL Monthly payments -- $1,184 + $303 =$1487 Percentage of Gross Pay 34% Percentage of Take-home pay 40%

AFTER 5 YEARS Appraisal Value -- $300,000 Home Equity Balance -- $146,000 Re-finance Loan -- $225,000 Cash Received -- $ 79,000 Loan Terms -- 5%, 30 years P & I Payments -- $ 1,208 Total Monthly Payment -- $ 1,600 Salary -- $ 60,000 year Percentage of Gross Pay 32% Percentage of Take-home 39%

AFTER CRASH (2 YEARS LATER) APPRAISAL VALUE $175,000 LOAN BALANCE $218,000 EQUITY <$ 43,000>