Download

1 / 28

280 likes | 406 Views

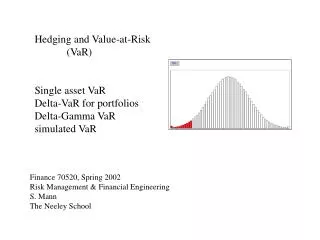

VaR Methods. IEF 217a: Lecture Section 6 Fall 2002 Jorion, Chapter 9 (skim). Value at Risk: Methods. Methods Historical Delta Normal Monte-carlo Bootstrap. Historical. Use past data to build histograms Method: Gather historical prices/returns

E N D

VaR Methods IEF 217a: Lecture Section 6 Fall 2002 Jorion, Chapter 9 (skim)

Value at Risk: Methods • Methods • Historical • Delta Normal • Monte-carlo • Bootstrap

Historical • Use past data to build histograms • Method: • Gather historical prices/returns • Use this data to predict possible moves in the portfolio over desired horizon of interest

Delta Normal • Estimate means and standard deviations • Use normal approximations • What if value is a function V(s)? • Need to estimate derivatives (see Jorion) • Computer handles this automatically in monte-carlo • Also, derivatives are all local approximations

Monte-Carlo VaR • Make assumptions about distributions • Simulate random variables • matlab: mcdow.m • Results similar to delta normal • Why bother with monte-carlo? • Nonnormal distributions • More complicated portfolios and risk measures • Confidence intervals: mcdow2.m

Value at Risk: Methods • Methods • Historical • Delta Normal • Monte-carlo • Bootstrapping

Bootstrapping • Historical/Monte-carlo hybrid • We’ve done this already • data = [5 3 -6 9 0 4 6 ]; • sample(data,n); • Example • bdow.m

Harder Example • Foreign currency forward contract • 91 day forward • 91 days in the future • Firm receives 10 million BP (British Pounds) • Delivers 15 million US $

Risk Factors • Exchange rate ($/BP) • r(BP): British interest rate • r($): US interest rate • Assume: • ($/BP) = 1.5355 • r(BP) = 6% per year • r($) = 5.5% per year • Effective interest rate = (days to maturity/360)r

Find the 5%, 1 Day VaR • Very easy solution • Assume the interest rates are constant • Analyze VaR from changes in the exchange rate price on the portfolio

Mark to Market Value(1 day future value) X = % daily change in exchange rate

X = ? • Historical • Delta Normal • Monte-carlo • Bootstrap

Historical • Data: bpday.dat • Columns • 1: Matlab date • 2: $/BP • 3: British interest rate (%/year) • 4: U.S. Interest rate (%/year)

BP Forward: Historical • Same as for Dow, but trickier valuation • Matlab: histbpvar1.m

BP Forward: Monte-Carlo • Matlab: mcbpvar1.m

BP Forward: Bootstrap • Matlab: bbpvar1.m

Harder Problem • 3 Risk factors • Exchange rate • British interest rate • U.S. interest rate

Daily VaR AssessmentHistorical • Historical VaR • Get percentage changes for • $/BP: x • r(BP): y • r($): z • Generate histograms • matlab: histbpvar2.m

Daily VaR AssessmentBootstrap • Historical VaR • Get percentage changes for • $/BP: x • r(BP): y • r($): z • Bootstrap from these • matlab: bbpvar2.m

Bootstrap Question: • Assume independence? • Bootstrap technique differs • matlab: bbpvar2.m

Risk Factors and Multivariate Problems • Value = f(x, y, z) • Assume random process for x, y, and z • Value(t+1) = f(x(t+1), y(t+1), z(t+1))

New Challenges • How do x, y, and z impact f()? • How do x, y, and z move together? • Covariance?

Delta Normal Issues • Life is more difficult for the pure table based delta normal method • It is now involves • Assume normal changes in x, y, z • Find linear approximations to f() • This involves partial derivatives which are often labeled with the Greek letter “delta” • This is where “delta normal” comes from • We will not cover this

Monte-carlo Method • Don’t need approximations for f() • Still need to know properties of x, y, z • Assume joint normal • Need covariance matrix • ie var(x), var(y), var(z) and • cov(x,y), cov(x,z), cov(y,z)

Value at Risk: Methods • Methods • Historical • Delta Normal • Monte-carlo • Bootstrap