Download

1 / 0

0 likes | 193 Views

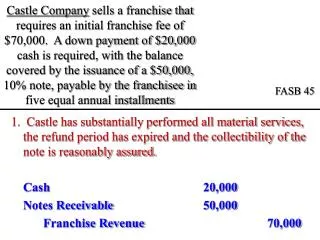

FASB Update. ACCOUNTING STANDARD UPDATES. ASUS ISSUED SINCE OCTOBER 2012. ASUS ISSUED SINCE OCTOBER 2012. ASUS ISSUED SINCE OCTOBER 2012. ASUS ISSUED SINCE OCTOBER 2012. ASUS ISSUED SINCE OCTOBER 2012. CLASSIFICATION OF SALES PROCEEDS OF DONATED FINANCIAL ASSETS (ASU 2012-05).

E N D