Download

1 / 12

120 likes | 213 Views

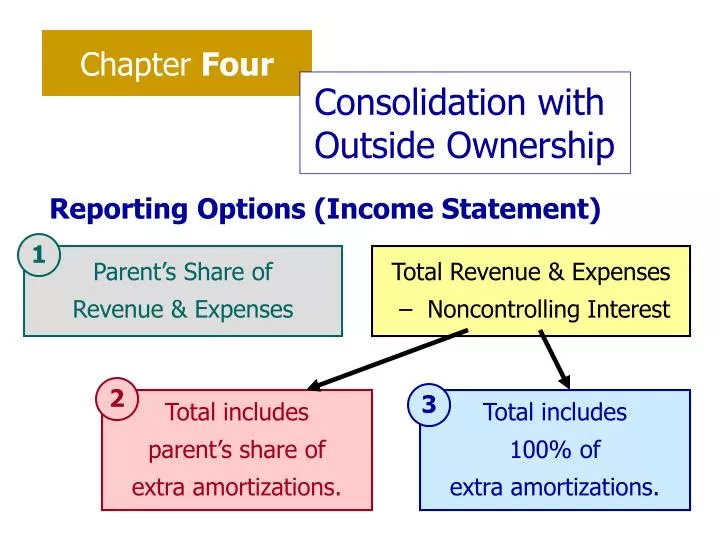

Chapter Four. Consolidation with Outside Ownership. Reporting Options (Income Statement). 1. Parent’s Share of Revenue & Expenses. Total Revenue & Expenses – Noncontrolling Interest. 2. 3. Total includes parent’s share of extra amortizations. Total includes 100% of

E N D

Chapter Four Consolidation with Outside Ownership Reporting Options (Income Statement) 1 Parent’s Share of Revenue & Expenses Total Revenue & Expenses – Noncontrolling Interest 2 3 Total includes parent’s share of extra amortizations. Total includes 100% of extra amortizations.

Reporting Options (Balance Sheet) 1 Parent’s Share of Assets & Liabilities Total Assets & Liab. – Noncontrolling Interest 2 3 Total includes parent’s share of extra assets. Total includes 100% of extra assets.

Noncnt intrst Parent claim Subsid assts $ 0 $ 96,000 $ 96,000 Current assts Current assts Current assts $ 96,000 $ 64,000 $160,000 $160,000 $ 64,000 $ 96,000 216,000 0 216,000 Bldg & equip Bldg & equip Bldg & equip 360,000 144,000 216,000 216,000 312,000 96,000 48,000 48,000 0 Goodwill Goodwill Goodwill 32,000 80,000 48,000 0 48,000 48,000 $360,000 $ 0 $360,000 Total Total Total $360,000 $600,000 $240,000 $360,000 $160,000 $520,000 Proportion. Parent Co. Econ Unit Example, p.159

Prob 4-39 Excess Annual Cost Amortization Equipment $(18,000) 10 yrs $(1,800) Buildings 93,000 15 yrs 6,200 Bonds Payable 12,000 10 yrs 1,200 Goodwill 31,000 - - Total $118,000 $5,600 Excess Annual Cost Amortization Equipment $(30,000) 10 yrs $(3,000) Buildings 155,000 15 yrs 10,333 Bonds Payable 20,000 10 yrs 2,000 Goodwill 51,667 - - Total $196,667 $9,333 60% Parent Co 100% Econ Unit ($400,000 0.60) - $470,000

Econ. Unit 380,000 250,000 378,000 252,000 Entry (S) Parent Co. R/E 380,000 Common Stock 250,000 Invst in Houston 378,000 NC int Hstn 1/1/05 252,000 Both methods treat book values of subsidiary the same.

Econ. Unit 124,000 14,000 51,667 21,000 101,200 67,467 Entry (A) Parent Co. Buildings 74,400 Bonds Payable 8,400 Goodwill 31,000 Equipment 12,600 Invst in Houston 101,200 NC int Hstn 1/1/05 Buildings 93,000 – 3 x 6,200 Bonds Payable 12,000 – 3 x 1,200 Goodwill 31,000 Equipment (18,000) – 3 x (1,800) 155,000 – 3 x 10,333 20,000 – 3 x 2,000 51,667 (30,000) – 3 x (3,000) 60% 100%

Econ. Unit 36,400 36,400 Entry (I) Parent Co. Equity in Hstn inc. 36,400 Invst in Houston 36,400 The parent’s share of subsidiary income is the same under both methods: 60%($70,000) - $5,600 = $36,400 Econ. Unit 24,000 24,000 Entry (D) Parent Co. Invst in Houston 24,000 Dividends Paid 24,000

Econ. Unit 7,333 2,000 3,000 10,333 2,000 Entry (E) Parent Co. Deprec Expense 4,400 Interest Expense 1,200 Equipment 1,800 Buildings 6,200 Bonds Payable 1,200 60% 100%

Econ. Unit 24,266 319,467 16,000 327,733 Noncontrolling Interest Entry Parent Co. NCint in Hstn inc. 28,000 NCint Hstn 1/1/05 252,000 Dividends Paid 16,000 NCint Hstn 12/31 264,000 40% ($70,000 - $9,333) $252,000 + $67,467

Excess Annual Cost Amortization Land $ 8,000 - Buildings 16,000 10 yrs $1,600 Goodwill 20,000 - - Total $44,000 $1,600 Prob 4-27 $156,000 – (80% x $140,000) = $44,000 Part (e) Purchase took place on July 1, 2004 Entry (S) R/E (1/1/04) 95,000 Preacq Income 4,000 Common Stock 40,000 Invst in Goldm 112,000 NC int Gldm 1/1/04 27,000

Palm Co. Storm Co. Totals Inc Stmnt Debits NC Int Revenues $ (300,000) $ (100,000) $ (400,000) Expenses 200,000 90,000 290,800 Preacq Inc 0 0 4,000 Ncint sub inc 0 0 2,000 Eqty in Sub (3,200) 0 0 Net Inc $ (103,200) $ (10,000) $ (103,200) Part (e) Purchase took place on July 1, 2004 (E) 800 (S) 4,000 (2,000) (I) 3,200 ½ year amortization 20% x $10,000