Download

1 / 10

110 likes | 280 Views

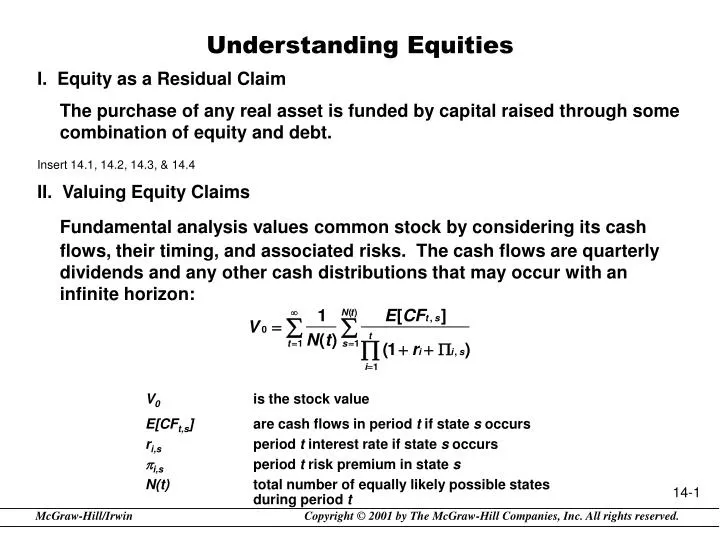

Understanding Equities I. Equity as a Residual Claim The purchase of any real asset is funded by capital raised through some combination of equity and debt. Insert 14.1, 14.2, 14.3, & 14.4 II. Valuing Equity Claims

E N D

Understanding Equities • I. Equity as a Residual Claim • The purchase of any real asset is funded by capital raised through some combination of equity and debt. • Insert 14.1, 14.2, 14.3, & 14.4 • II. Valuing Equity Claims • Fundamental analysis values common stock by considering its cash flows, their timing, and associated risks. The cash flows are quarterly dividends and any other cash distributions that may occur with an infinite horizon: V0 is the stock value E[CFt,s] are cash flows in period t if state s occurs ri,s period t interest rate if state s occurs pi,speriod t risk premium in state s N(t) total number of equally likely possible states during period t

Simplifying assumptions: 1. annual dividends 2. the periodic cash flows are averaged to a single number 3. dividends follow a simple growth pattern 4. one interest rate per period 5. sometimes a single interest rate is assumed for all time periods 6. there is a single risk premium across all states and periods • Insert 14.5 These yield: D0 current annual dividend gn period n dividend growth rate k annual discount rate

If growth is assumed to be constant beyond h years, the formula can be separated into finite and infinite parts: With a constant growth assumption, the formula simplifies to: • III. Riskiness of Equity Claims • There are numerous ways of assessing the riskiness of equity. With a single security, risk can be measured by the variability of cash flows. • The variance of an asset i is:

The covariance between two assets is: where r is return and t is time. • A scaling of the covariance to a range of -1 to 1 results in the correlation statistic: • A graphing of the variance and return of all possible combinations of two assets leads to a curved line which is called the efficient frontier. This line is efficient in the sense that for any given return, the minimum variance portfolio is on this line. • Insert 14.7 & 14.8

The variance of a portfolio of assets is the sum of the individual variances and covariances, each weighted by the quantity held. As the number of assets increases, the covariances stochastically dominate the variances. • When an investor possesses all assets (i.e. the market portfolio) and a riskless asset is available, the Capital Asset Pricing Model demonstrates that the relevant measure of risk is beta. Beta is merely the covariance between a single stock’s returns and that of the market portfolio; the only difference between beta and correlation is that the covariance is divided by the market portfolio’s variance:

Betas are calculated by regressing individual returns on market returns: ritreturn on asset i at time t rMarket Portfolio,ireturn on the market portfolio at time t etregression error term at time t • Another, less common measure of stock risk is stock duration. It measures the percentage change in value for a change in interest rates. • Duration is calculated by regressing the percentage change of stock prices over interest rate movements.

IV. Equity Market Efficiency • The efficiency of the equity market has been studied from many different perspectives. However, economists have focused on informational efficiency. Do prices rapidly change to reflect all available information? • Three types of efficiency: weak form efficiency, semi-strong form efficiency and strong form efficiency. • Research has produced the general conclusion that markets are efficient (especially informational). • V. Stock Ratings • Stock rating is a growing business. Rating firms take a rigorous approach in their assessments. • Standard & Poor’s assessment is based upon earnings per share (EPS) and dividends per share. Scores are then combined into a single categorical rating: A+ Excellent B+ Average A Good B Below Avg. A- Above Avg. B- Low C Lowest Value Line grades stocks by investment quality. Their analysis contains both subjective and objective elements. • Insert 14.10

VI. Types of Equity Ownership • A. Common Stock • Common stock represents a share in the ownership of the firm. It involves voting rights on major decisions. • Common stock owners are also entitled to dividends, if paid. • B. Preferred Stock • Holders of preferred stock receive dividends. The dividend is either a fixed rate or floating rate. • Cumulative provisions ensure that if dividends are suspended, shareholders will receive all back dividends prior to those awarded to common stock. • Most preferred stock carries a par value. This value is usually close to the initial amount received by the issuer. • Preferred stock often has a sinking fund provision. • Preferred stock has the characteristics of both common stock and bonds. • Insert 14.8 & 14.9

VII. Blurred Distinctions Between Debt and Equity There are close to one hundred other types of securities issued by corporations. Many of these were introduced within the last ten years and are difficult to classify as debt or equity. • A. A Financial Perspective A demonstration of how debt becomes more like equity and how new securities are hybrids of both. • Insert 14.10 & 14.11 • B. A Legal Perspective • The proliferation of new financial instruments has strained traditional legal analysis. • The duties of management to creditors are spelled out in the indenture agreement. It is extremely difficult and complex for management to exercise its fiduciary duties in a balanced way toward creditors and shareholders during a period of insolvency.

VIII. Summary • Equity is a claim on the corporate assets and their returns. • Valuation of equity is a diverse area but retains many of the characteristics of valuation that we have learned earlier. • The risk associated with both a single equity and a portfolio of equities was examined. • The issues surrounding the efficiency of equity market valuation was considered. • The distinction between common and preferred stock was illustrated. • Preferred stock as well as many of the new financial instruments retain characteristics of both debt and equity.