Download

1 / 22

220 likes | 403 Views

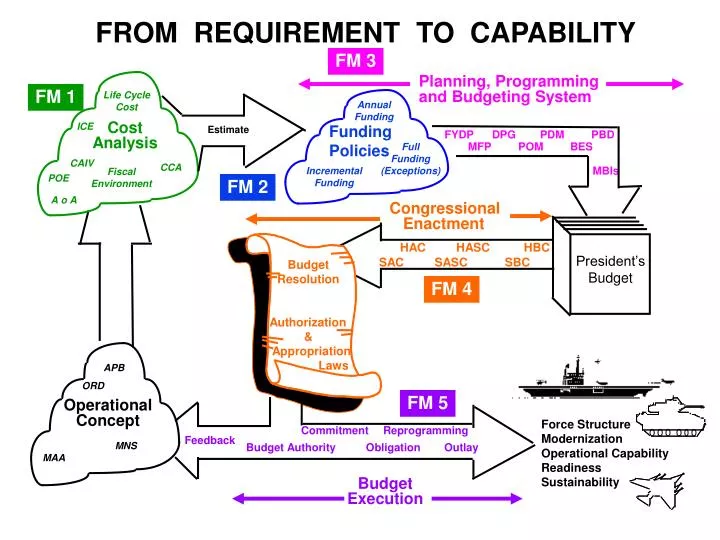

Planning, Programming and Budgeting System. Life Cycle Cost. Annual Funding. Funding Policies. Estimate. ICE. Cost Analysis. FYDP DPG PDM PBD. MFP POM BES. Full Funding (Exceptions). MBIs. CAIV. Incremental Funding. CCA. Fiscal

E N D

Planning, Programming and Budgeting System Life Cycle Cost Annual Funding Funding Policies Estimate ICE Cost Analysis FYDP DPG PDM PBD MFP POM BES Full Funding (Exceptions) MBIs CAIV Incremental Funding CCA Fiscal Environment POE A o A Congressional Enactment HAC HASC HBC President’s Budget SAC SASC SBC Budget Resolution Authorization & Appropriation Laws APB ORD Operational Concept Force Structure Modernization Operational Capability Readiness Sustainability Commitment Reprogramming Feedback Budget Authority Obligation Outlay MNS MAA Budget Execution FROM REQUIREMENT TO CAPABILITY FM 3 FM 1 FM 2 FM 4 FM 5

FM1 Lesson Overview • Fiscal Environment • Life Cycle Cost Concepts • Analysis of Alternatives • Cost Estimating Requirements • Cost Estimating Methodologies • Learning Curve • Affordability • Cost as an Independent Variable

Federal Government Spending1950-2000 All Other Net Interest Other Grants Payments to Individuals National Defense

Budget Authority Credit Card Spending Limit Commitment Verifies Available Credit Obligation Purchase Item with Credit Card Expenditure Write Check for Credit Card Bill Outlay Check clears your account Monetary Concepts

Life Cycle Cost • Life Cycle Cost is the ________________ to the Government for a system over its ________________. • Three ways to look at Life Cycle Cost: • ______________________________ • ______________________________ • ______________________________ • __________________________ • __________________________ • __________________________ • __________________________ total cost entire life Appropriations Work Breakdown Structure Cost Categories (DoD 5000.4-M) Research & Development Investment Operation & Support Disposal

Life Cycle Cost Categories Notional % of LCC ~16% Space system ~53 - 54% Surface vehicle ~66 - 68% Ship ~66% ~0% ~37% ~18% ~0 - 1% ~31% Operating & Support Cost Program Cost % ~9% ~0 - 2% Disposal Cost ~1% R&D Cost Investment Cost Production & Deployment C&TD SD&D Support

Life Cycle Cost Composition } Life Cycle Cost RDT & E Prime Equipment & Support Items MILCONFacilities O & M, MILPERS (also RDT&E, Procurement, MILCON) • Operations & Support • Disposal PROCUREMENT Support Items PROCUREMENT Prime Equipment PROCUREMENT Initial Spares Program Acquisition Cost Weapon System Cost Procurement Cost Flyaway Cost Development Cost

Cost Terms WBS Elements Prime Mission Equipment - Hardware & Software - Test & Evaluation - Systems Engineering - Program Management - Nonrecurring “Startup” - Allowance for Changes Support Items - Tech Data - Publications - Contractor Services - Support Equipment - Training Equipment - Factory Training O & S Elements - Petroleum, Oil, Fuel Lubricants - Training - Personnel - Supplies & Spares - Maintenance • Development = Research and Development of Prime Mission Equipment and Support Items • Flyaway = Procurement of Prime Mission Equipment • Weapon System = Procurement of Prime Mission Equipment and Support Items (or Procurement - Initial Spares) • Procurement = Procurement of Prime Mission Equipment, Support Items and Initial Spares • Program Acquisition = Development + Procurement + Facilities • Life Cycle = Program Acquisition + O&S + Disposal

Cost Estimating - Players & Products • Program Office • Program Office Estimate (POE) • Cost Analysis Requirements Description (CARD) • User • Analysis of Alternatives (AoA) • Component • Component Cost Analysis (CCA) • OSD Cost Analysis Improvement Group (CAIG) • Independent Cost Estimate (ICE) • Contractors

Analysis of Alternatives (AoA) DoD 5000.2-R Part 2.4 • Quantitative discussion of • reasonable materiel alternatives • Purposes: • Aid & document decision-making • Foster joint ownership, enhance understanding of future decisions • ACAT I • Required at Program Initiation • Prepared by User (not PMO) designated by Component head • ACAT IA • Required at Program Initiation • Prepared by the OSD Principal Staff Assistant (PSA) • Optional for other ACATs (MDA discretion)

Cost Estimating Requirements ACAT IC & IDACAT IA POE Program Initiation & Program Initiation & all subsequent milestones all subsequent milestones Includes cost-benefit analysis CARD Same as ICE or CCA Same as CCA CCA - ACAT IC: All milestones All milestones starting with after Milestone A (Milestone 0) Milestone B (Milestone I) (unless OSD CAIG does ICE) - Prepared at MDA discretion for programs with OSD CAIG ICE ICE ACAT ID - All milestones after Milestone A (Milestone 0) Note: Italics denote applicable milestones for programs grandfathered under 1996 version of DoD 5000.2-R Source: Interim DoD 5000.2-R, Sep 2000

Defense Acquisition Board Assistant Secretary (FM) Reconciliation (if necessary) Program Office MDAP Cost Review Process OSD CAIG ICE OIPT + Svc Cost Position Svc Cost Position (ACAT ID) Service Acquisition Decision Panel POE + CCA (ACAT IC) POE CCA Service Cost Agency

Assistant Secretary (FM) Review Program Office MAIS Cost Review Process IT OIPT POE + CCA (ACAT IAM) PA&E Analysts Service Acquisition Decision Panel POE + CCA (ACAT IAM) POE + CCA (ACAT IAC) POE CCA Service Cost Agency

Cost Estimating Methods ANALOGY PARAMETRIC ENGINEERING ACTUAL COSTS 1 to 1 comparison of like system Statistical analysis of like systems “Bottoms-up” estimate Extrapolation from actuals of same system Actual contract of same system +/- changes CAIG really likes it !! Cost data exists Prototype / Production differences Take current system +/- changes Fast Inexpensive Easy to change Subjective Risky Cost Estimating Relationships Easy to do “what-If” drills Constrained by data GIGO WBS by component Accurate Piece by piece WBS Slow Labor Intensive Expensive WHAT HOW WHEN ADV DISADV MS C, LRIP When drawings, specs available Rate Prod Review, Subsequent Prod Contracts Early MS B & later

GROSS ESTIMATES DETAILED ESTIMATES Concept & Technology Development System Development & Demonstration Production & Deployment Cost Estimating MethodsAppropriate to Acquisition Phases Actuals Parametric Analogy Engineering CE PDRR EMD Production / O&S

Learning Curve Theory As the quantity produced of a product doubles, the per unit production hours expended in producing the product will decrease at a fixed rate or constant percentage.

Learning Curves • Apply to production labor • A “90% learning curve” means that the labor hours to produce the fourth unit are only 90% of those required to produce the second unit (10% decrease). • Reasons that improvement occurs • Worker experience • Uninterrupted production • Consistent design • Tooling improvements • Emphasis on productivity

Learning Curve - Computing UNITDIRECT LABOR HOURS 1...........................................… 200 2...........................................… ____ 3 169 4...........................................… ____ 5 157 6 152 7 149 8...........................................… ____ 9 143 10 141 180 (.9 x 200) 162 (.9 x 180) 90 % LEARNING CURVE 146 (.9 x 162)

Affordability • Programs must be consistent with overall DoD planning and funding priorities • To foster greater program stability: • Assess program affordability at each milestone and decision review • Programs must be fully funded in the FYDP • CAIG (ICE) and CPIPT reviews (CAIV) shall provide sufficiently accurate cost and/or benefit data to allow reasonable affordability assessments

Cost As An Independent Variable (CAIV)BASIC CONCEPT • Essential to balance three significant parameters or variables in acquisition programs: • Performance satisfying operational requirements • Affordable Life-Cycle Cost • User Acceptable Schedule • Two of those variables are dependent on the third. • Under CAIV philosophy, performance and schedule are dependent on cost

CAIV Concept of Implementation • PM establishes cost objectives for each life-cycle cost category at Program Initiation • PM reassesses cost objectives and progress toward achievement at subsequent milestones & decision reviews • Cost/Performance IPT considers reducing life cycle costs by trading (i.e., reducing) specific performance parameters (but not required capabilities) • PM approves trade-offs within ORD/APB performance thresholds • Performance breaches require ORD/APB validation authority approval