Download

1 / 65

650 likes | 794 Views

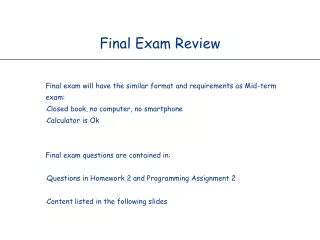

REVIEW FINAL EXAM. 45 40 35 30 25 20 15. 30 25 20 15 10. Sugar (tons). Sugar (tons). 5 10 15 20 25 30. 5 10 15 20. Wheat (tons). Wheat (tons). Wheat. Sugar. USA. 30. 30. (1W costs 1S). (1S costs 1W). Brazil. 10. (1W costs 2S). 20.

E N D

45 40 35 30 25 20 15 30 25 20 15 10 Sugar (tons) Sugar (tons) 5 10 15 20 25 30 5 10 15 20 Wheat (tons) Wheat (tons) Wheat Sugar USA 30 30 (1W costs 1S) (1S costs 1W) Brazil 10 (1W costs 2S) 20 (1S costs 1/2W) Which country has a comparative advantage in wheat? • Which country should EXPORT Sugar? • Which country should EXPORT Wheat? • Which country should IMPORT Wheat?

Output Questions: OOO= Output: Other goes Over

Input Questions: IOU= Input: Other goes Under

Q % d % P PRICE ELASTICITY OF DEMAND Commonly Expressed as… The percentage change in quantity P The percentage change in price P2 P1 Elasticity is .5 D Q Q2 Q1

Pineapples Radios Kenya 30 10 (1R costs 3 P) (1P costs 1/3R) India 40 (1P costs 1R) 40 (1R costs 1P) Kenya wants Radios If the terms of trade for 1 radio is greater than 3 pineapples then Kenya is worse off and should make radios on their own. India wants Pineapples If the terms of trade for 1 radio is less than 1 pineapple then India is worse off and should make pineapples on their own. What terms of trade benefit both countries?

Pineapples Radios Kenya 30 10 (1R costs 3 P) (1P costs 1/3R) India 40 (1P costs 1R) 40 (1R costs 1P) Trading 1 radio for 2 pineapples will benefit both If Kenya produces radios by themselves, they give up 3 Pineapples for each radio. If they can trade 2 pineapples for each radio they are better off. If India produces pineapples by themselves, they give up 1 pineapple for one radio. If they can get 2 pineapples for one radio they are better off. The countries trade at a lower opportunity cost than if they made the products themselves!

Use the midpoint formula again. • Elasticity = • % change in Q = • % change in Q = • For the quantities of 10 and 7, the % change in Q is approx. 35.3 percent. (3/8.5 times 100) Elasticity

Using the Midpoint Formula Elasticity = % change in p = times 100. % change in p = For the prices $2 and $2.50, the % change in p is approx. 22.22 percent. Elasticity

PRICE ELASTICITY OF DEMAND Extreme Cases Perfectly Inelastic Demand D1 P Ed = 0 0 Q Perfectly Elastic Demand P D2 Ed = Q 0

PRICE ELASTICITY & TOTAL REVENUE So is total revenue When prices are low, P TR D Q Quantity Demanded

PRICE ELASTICITY & TOTAL REVENUE Total revenue rises with price to a point... P TR D Q Quantity Demanded

PRICE ELASTICITY & TOTAL REVENUE Total revenue rises with price to a point... then declines P TR D Q Quantity Demanded

PRICE ELASTICITY & TOTAL REVENUE Total revenue rises with price to a point... then declines P TR D Q Quantity Demanded

PRICE ELASTICITY & TOTAL REVENUE Total Revenue Test Total revenue rises with price to a point... then declines P TR D Q Quantity Demanded

PRICE ELASTICITY & TOTAL REVENUE Total revenue rises with price to a point... then declines P TR Inelastic Demand D Inelastic Demand Q Quantity Demanded

PRICE ELASTICITY & TOTAL REVENUE Total revenue rises with price to a point... then declines P TR Elastic Demand Inelastic Demand D Elastic Demand Inelastic Demand Q Quantity Demanded

PRICE ELASTICITY & TOTAL REVENUE Total revenue rises with price to a point... then declines P TR Unit Elastic Elastic Demand Inelastic Demand D Elastic Demand Inelastic Demand Q Quantity Demanded

ECONOMIC COSTS Economic Profit Accounting Profit Implicit costs (including a normal profit) Accounting costs (explicit costs only) Explicit Costs Profits to an Economist Profits to an Accountant T O T A L R E V E N U E Economic (opportunity) Costs

SHORT-RUN PRODUCTION RELATIONSHIPS Law of Diminishing Returns Total Product Total Product, TP Increasing Marginal Returns Quantity of Labor Average Product, AP, and Marginal Product, MP Average Product Marginal Product Quantity of Labor

SHORT-RUN PRODUCTION RELATIONSHIPS Law of Diminishing Returns Total Product Total Product, TP Diminishing Marginal Returns Quantity of Labor Average Product, AP, and Marginal Product, MP Average Product Marginal Product Quantity of Labor

SHORT-RUN PRODUCTION RELATIONSHIPS Law of Diminishing Returns Total Product Total Product, TP Negative Marginal Returns Quantity of Labor Average Product, AP, and Marginal Product, MP Average Product Marginal Product Quantity of Labor

UTILITY MAXIMIZING COMBINATION MU of product B MU of product A Price of A Price of B 16 Utils 8 Utils = $1 $2 Algebraic Restatement of the Utility Maximization Rule =

PRODUCTIVITY AND COST CURVES Average product and marginal product Quantity of labor Costs (dollars) Quantity of output AP MP MC AVC

LONG-RUN PRODUCTION COSTS Unit Costs Output

LONG-RUN PRODUCTION COSTS Unit Costs Output

LONG-RUN PRODUCTION COSTS The long-run ATC just “envelopes” all of the short-run ATC curves. Unit Costs Output

LONG-RUN PRODUCTION COSTS Unit Costs long-run ATC Output

ECONOMIES AND DISECONOMIES OF SCALE • Labor Specialization • Managerial Specialization • Efficient Capital • Other Factors Diseconomies of Scale Constant Returns to Scale graphically presented...

ECONOMIES AND DISECONOMIES OF SCALE Economies of scale Unit Costs long-run ATC Output

ATC decreases as Output increases ATC is constant as Output increases Constant returns to scale Economies of scale Unit Costs long-run ATC Output

ATC decreases as Output increases ATC is constant as Output increases ATC increases as Output increases Constant returns to scale Diseconomies of scale Economies of scale Unit Costs long-run ATC Output

MARGINAL REVENUE-MARGINAL COST APPROACH Profit Maximization Position $200 150 100 50 0 Economic Profit MC MR $131.00 ATC Cost and Revenue AVC $97.78 1 2 3 4 5 6 7 8 9 10

MR = MC Optimum Solution MARGINAL REVENUE-MARGINAL COST APPROACH Profit Maximization Position $200 150 100 50 0 Economic Profit MC MR $131.00 ATC Cost and Revenue AVC $97.78 1 2 3 4 5 6 7 8 9 10

MARGINAL REVENUE-MARGINAL COST APPROACH Short-Run Shut Down Point $200 150 100 50 0 MC ATC Cost and Revenue AVC MR $71.00 Minimum AVC is the Shut-Down Point 1 2 3 4 5 6 7 8 9 10

SHORT-RUN COMPETITIVE EQUILIBRIUM The Competitive Firm “Takes” its Price from the Industry Equilibrium S= MCs P P Economic Profit ATC S=MC D $111 $111 AVC D Q Q 8 8000 Firm (price taker) Industry

SHORT-RUN COMPETITIVE EQUILIBRIUM How about the long-run? The Competitive Firm “Takes” its Price from the Industry Equilibrium S= MCs P P Economic Profit ATC S=MC D $111 $111 AVC D Q Q 8 8000 Firm (price taker) Industry

PROFIT MAXIMIZATION IN THE LONG RUN P P $60 50 40 $60 50 40 Q Q 100 100,000 Firm (price taker) Industry Temporary profits and the reestablishment of long-run equilibrium S1 MC ATC MR D1

P P $60 50 40 $60 50 40 Q Q 100 100,000 Firm (price taker) Industry PROFIT MAXIMIZATION IN THE LONG RUN An increase in demand increases profits… Economic Profits S1 MC ATC MR D2 D1

PROFIT MAXIMIZATION IN THE LONG RUN P P $60 50 40 $60 50 40 Q Q 100 100,000 Firm (price taker) Industry New competitors increase supply, and lower prices decrease economic profits. Zero Economic Profits S1 S2 MC ATC MR D2 D1

PROFIT MAXIMIZATION IN THE LONG RUN P P $60 50 40 $60 50 40 Q Q 100 100,000 Firm (price taker) Industry Decreases in demand, losses, and the reestablishment of long-run equilibrium S1 MC ATC MR D1

P P $60 50 40 $60 50 40 Q Q 100 100,000 Firm (price taker) Industry PROFIT MAXIMIZATION IN THE LONG RUN A decrease in demand creates losses… Economic Losses S1 MC ATC MR D1 D2

P P $60 50 40 $60 50 40 Q Q 100 100,000 Firm (price taker) Industry PROFIT MAXIMIZATION IN THE LONG RUN Competitors with losses decrease supply, and prices return to zero economic profits. S3 Return to Zero Economic Profits S1 MC ATC MR D1 D2

MARGINAL REVENUE-MARGINAL COST APPROACH Loss Position $200 150 100 50 0 Economic Loss MC ATC Cost and Revenue AVC $91.67 MR $81.00 1 2 3 4 5 6 7 8 9 10

MONOPOLY REVENUES & COSTS Elastic T $200 150 200 50 Dollars MR D Q 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 $750 500 250 Dollars TR Q 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

MONOPOLY REVENUES & COSTS Elastic Inelastic $200 150 200 50 Inelastic Portion MR is Negative Dollars A Monopolist will always operate on the Elastic Portion of the Demand Curve MR D Q 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 $750 500 250 Dollars TR Q 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

OUTPUT AND PRICE DETERMINATION 200 175 150 125 100 75 50 25 Price, costs, and revenue Q 0 1 2 3 4 5 6 7 8 9 10 Profit Maximization Under Monopoly Remember the MR=MC Rule? Profit Per Unit MC $122 Profit ATC $94 D MR = MC MR

OUTPUT AND PRICE DETERMINATION 200 175 150 125 100 75 50 25 What About Loss Minimization? Price, costs, and revenue Q 0 1 2 3 4 5 6 7 8 9 10 Profit Maximization Under Monopoly Profit Per Unit MC $122 Profit ATC $94 D MR = MC MR

OUTPUT AND PRICE DETERMINATION Since Pm exceeds AVC, the firm will produce 200 175 150 125 100 75 50 25 Price, costs, and revenue Q 0 1 2 3 4 5 6 7 8 9 10 Loss Minimization Under Monopoly Loss Per Unit MC ATC A Loss AVC Pm V D MR = MC MR Qm