Download

1 / 39

390 likes | 585 Views

The review of Georgian Customs environment. 10 th DWVG Economic Forum 14 December, 2010 David Koghuashvili, Of-Counsel Mgaloblishvili Kipiani Dzidziguri (MKD). The review of Georgian Customs environment. Content. Introduction Golden List (authorized economic operator)

E N D

The review of Georgian Customs environment 10thDWVG Economic Forum 14 December, 2010 David Koghuashvili, Of-Counsel Mgaloblishvili Kipiani Dzidziguri (MKD)

The review of Georgian Customs environment Content • Introduction • Golden List (authorized economic operator) • Registration of Goods and the State Control • The sequences of procedure for the commodity registration at the EZR during import 2

The review of Georgian Customs environment As of January 1st 2011 the new tax and customs laws, which are incorporated now into one single code, will be enforced.And many of provisions form the named changes have already been reflected in presently active revenue legislation from the August 1st 2010.All these changes were developed following a fundamental review of tax and customs policies to introduce a more liberal regime. As a result out of 21 taxes under the former tax code, only six exist today and will remain as it is thereafter. Introduction In September 2010 the Parliament of Georgia adopted a new tax code (the “Tax Code”) which will take effect from January 1, 2011. The Tax Code introduces a several new initiatives and predominantly aims at improvement of the tax environment, attraction of investments through offering the efficient tax administration and better protection of the taxpayers’ rights. At the same time, one of the major novelties of the Tax Code is that it incorporates both tax and the customs legislation into a single legal act, which could be named as Georgian Revenue Code. 3

The review of Georgian Customs environment As of January 1st 2011 the new tax and customs laws, which are incorporated now into one single code, will be enforced.And many of provisions form the named changes have already been reflected in presently active revenue legislation from the August 1st 2010.All these changes were developed following a fundamental review of tax and customs policies to introduce a more liberal regime. As a result out of 21 taxes under the former tax code, only six exist today and will remain as it is thereafter. • More is coming ahead in terms of secondary legislation, normative act, bylaws which will provide with more clarity to certain provisions from tax code. • This time the presentation offers the main trends under the Revenue code dealing with the most recent implications on customs regulations. Namely what are those novelties providing with simplicity to the customs clearance process: • To start with, let me admit that under new Revenue code the customs procedures, likewise in taxation case, are also regulated by sub-legislative acts of the Ministry of Finance and the revenue Service. These acts were still at the level of elaboration in the course of preparation of this brochure. Therefore, we will have to refer to the draft version of normative acts and other official materials when presenting these novelties in front of you today. Introduction 4

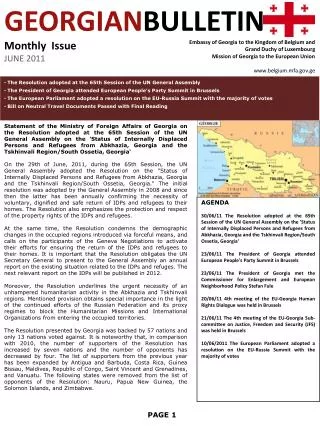

The review of Georgian Customs environment As of January 1st 2011 the new tax and customs laws, which are incorporated now into one single code, will be enforced.And many of provisions form the named changes have already been reflected in presently active revenue legislation from the August 1st 2010.All these changes were developed following a fundamental review of tax and customs policies to introduce a more liberal regime. As a result out of 21 taxes under the former tax code, only six exist today and will remain as it is thereafter. • In this regards customs system is one of the most important components of the reforms accomplished by the GOG. • As a result of this reform the customs procedures became upgraded and simplified and modern management technologies have been introduced. • At present the Customs executes a risk management profile system that is based on an automated processing of filed customs returns/declarations – ASYCUDA (Automated System of Customs Data). • This clearance system anticipates the four channel release of goods at customs. • Physical examinations of goods, that take place only in the red channel; • Only documentary checking goes on in the yellow channel. • When releasing the goods through the green and the blue channels no examination of goods is performed (in case of the blue channel only audit can be expected after certain period of time). Introduction 5

The review of Georgian Customs environment As of January 1st 2011 the new tax and customs laws, which are incorporated now into one single code, will be enforced.And many of provisions form the named changes have already been reflected in presently active revenue legislation from the August 1st 2010.All these changes were developed following a fundamental review of tax and customs policies to introduce a more liberal regime. As a result out of 21 taxes under the former tax code, only six exist today and will remain as it is thereafter. • After launching this system 85% of goods undergo customs registration without a physical examination by means of a camera control only. • The process of customs registration itself is carried out inside the territory of Georgia in specially arranged customs offices (Tbilisi, Telavi, Akhaltsikhe, Gori, Kutaisi, Batumi and Poti regional centers). In line with this simplification three special zones have been in introduced for customs processing– so called Economic Zone of Registration (hereinafter – EZR), through out Georgia, namely: • Economic Zone of Registration TBILISI • Economic Zone of Registration BATUMI • Economic Zone of Registration POTI. • Among these zones the Economic Zone of Registration TBILISI had already been launched at the end of November, last month 2010 and the other two zones will begin to function in the 1st quarter of 2011. Introduction 6

The review of Georgian Customs environment 6

The review of Georgian Customs environment As of January 1st 2011 the new tax and customs laws, which are incorporated now into one single code, will be enforced.And many of provisions form the named changes have already been reflected in presently active revenue legislation from the August 1st 2010.All these changes were developed following a fundamental review of tax and customs policies to introduce a more liberal regime. As a result out of 21 taxes under the former tax code, only six exist today and will remain as it is thereafter. Golden List (authorized economic operator) Importer/Exporter Golden List (authorized economic operator) is another innovation of the Customs system of Georgia. Persons included in this list have the right to enjoy even more simplified customs procedures and pay import duties under concessional deadlines. Otherwise the customs price in general relies on methods based on‘’General Agreement in Tariffs and Trade’’ standards (GATT) In the end, as a result of the reforms the duration of undertaking customs procedures counts only 2 hours at present (versus the period of three day practiced earlier) 7

The review of Georgian Customs environment Registration of Goods and the State Control The most widespread customs regimes include import, export, temporary import of goods, transit and re-export. At the moment of registration of goods the owner of the commodity fills in a customs (commodity) declaration and pays customs taxes and duties. Size of taxes and duties depends on the type of a customs regime (commodity operation) and the commodity, as well as the quantity of the good. In case of an import the owner of the goods completes a certificate of origin of the goods as well. 8

The review of Georgian Customs environment Registration of Goods and the State Control Customs duties consist of the import fee, VAT, excise duty and customs fees. In case of import of certain type of goods the importer is also required to get a relevant license/permit and pay a license/permit fee. Tariff of the import fee is fixed and it can be 0%, 5% or 12%. The tariff depends on the type of commodity. 9

The review of Georgian Customs environment Registration of Goods and the State Control 12% tariff rate basically applies to beef, mutton or chicken and meat products, particular types of dairy products, mineral water, fruit, specific building material etc. (The detailed list is available in the first part of Article 197 of the Tax Code of Georgia). 5% tariff rate applies to pork, means of hygienic care and cosmetic items, clothes, plastic produce etc. 10

The review of Georgian Customs environment Registration of Goods and the State Control Special tariff is anticipated for import of strong beverages. Import fee for 100 liters of strong beverage consists of the tariff rate (0.2 to 3 EURO) multiplied by the percentage data of alcohol in the beverage. (For example, in case of Whisky importers if the volume of alcohol is 40%, the import fee on 100 liters will be 1.5 EURO x 40 or 60 EURO) For specific type of beverages the tariff rate is defined directly thus is fixed (for example, Sparkling Wine – 1.5 EURO per one litter) 11

The review of Georgian Customs environment Registration of Goods and the State Control 0% rate is anticipated for baby food and diabetic products, special machinery, transportation and equipment related to the oil and gas industry. A zero rate is foreseen for one time import of particular type of goods if the import is not related to an economic activity 12

The review of Georgian Customs environment Registration of Goods and the State Control • Apart from the commodity spelled out above, the following import is also taxed at a zero rate: • Import of commodity produced in a free industrial zone; • Import of commodity foreseen in a grant agreement; • Import of goods for diplomatic purposes; • Import of fuel, lubricant and other materials for international • flights and shipment; • Import of four liters of strong beverages and 200 cigarettes; • Import of goods in a parcel by a legal person provided that • the value of the goods does not exceed GEL 300 and total • weight of them is not more than 30kg. 13

The review of Georgian Customs environment Registration of Goods and the State Control Concessional regimes of taxation may be introduced in the process of trade with individual countries through international trade agreements or the Generalized systems of Preferences – GSP. Import of goods in Georgia is taxed with the Value Added tax. VAT rate is 18% and it is calculated from the price of import. The import price is the sum of the price of imported goods, the payable taxes in the process of import (except VAT) and the service cost that is considered to be a subsequent service of the imported goods. 14

The review of Georgian Customs environment Registration of Goods and the State Control Tax Code foresees a special regime of VAT taxation of import for those persons who made more than 200,000 GEL VAT payment for 12 (consecutive) months. In this case the import of goods is not looked upon as the object of taxation for the person. At that, it is deemed as if person received a credit on taxable import of particular goods within the reporting period. 15

The review of Georgian Customs environment Registration of Goods and the State Control Import of excise goods is taxed with excise tax too. Tax rate in this case is differentiated and depends on the type of excise goods. (For example, excise tariff for beer is 0.4 GEL per 1 liter, but for whisky it is 3 GEL per 1 liter). In case of import of certain goods ((scrap metal for instance) the price of import is calculated according to weight. In case of import of a light automobile the price of import is defined according to the age of the car and the volume of its engine. 16

The review of Georgian Customs environment Registration of Goods and the State Control • When moving the goods across the economic territory of Georgia (import, export, transit, etc.) the applicable liabilities are identified according to the integrated tariff of Georgia. • The integrated tariff is approved by the Government of Georgia. This is a unity of data consisting of: • National Product mix of foreign economic activity (hereinafter – NAFE); • Import duty rates or/and concessions applicable to the goods included in NAFE; • Concessions (preferences) established by the effective international agreements ratified by the Georgian Parliament; • Prohibitions and restrictions identified by the Georgian legislation and applicable to the goods included in NAFE 17

The review of Georgian Customs environment Registration of Goods and the State Control Identification and classification of goods are carried out on basis of NAFE codes. The commodity code is specified by the declarant; declarant self identifies then a tariff value and applies into a declaration. When defining the value, the special rules in compliance with the WTO regulations are used. The proposed tariff value is verified (controlled) by the Revenue Service who has the right to disagree with the given value. In this case the Revenue Service identifies the value on its own. 18

The review of Georgian Customs environment Registration of Goods and the State Control The reform of the customs system anticipates one more innovation – the owner of the goods obtains the right for correcting the already completed declaration at his/her own decision and no sanctions (penalty) are applied in such case. This is a case when taxpayer declares incorrect value of the goods, when in reality it is higher than the one indicated in the declaration. The declarant/taxpayer is entitled to make amendments to the declaration at his own initiative, and if it does so, no penalties will be applied. 19

The review of Georgian Customs environment Registration of Goods and the State Control 6 different methods for the value definition are employed in the event of import. In particularity, the value can be defined: a) According to the price of a transaction (the first method); b) According to the price of a transaction on identical commodity (the second method); c) According to the price of a transaction on alike commodity (the third method); d) According to the unit price of the goods (the fort method); e) According to the compound value (the fifth method); f) According to the reservation method (the sixth method). 20

The review of Georgian Customs environment Registration of Goods and the State Control These methods are applied only successively. It means that the second method shall be employed only then when it is not possible to identify the value by use of the first method and so on. The State control is accomplished for the purpose of double checking of accuracy of the data given in a declaration. The control is carried out in a respective zone on the territory of Georgia. The control also includes the phytosanitary border and quarantine, veterinary border and quarantine and sanitary-quarantine examination 21

The review of Georgian Customs environment The sequences of procedure for the commodity registration at the EZR during import 22

The review of Georgian Customs environment Step by step procedure of commodity registration at the EZR in the course of import The driver Upon arrival at the EZRhands a registration certificate over to an administrative officer sitting in a cabin without getting out of the truck. The officer provides the driver with: A parking card and the permit to enter the EZR. The truck gets moved to the parking place. 23

The review of Georgian Customs environment Step by step procedure of commodity registration at the EZR in the course of import • The administrative officer confirms arrival of the vehicle/transportation in ASUCUDA database and puts the following information in the internal database: • Plate number of the vehicle; • The number of a registration certificate, the number and name of declarants (if any). The administrative officer reconciles the certificate data with the numbers of the truck and the seal and verifies the wholeness of the seal. • In case of breakage/inconsistence of wholeness of the seal an delinquency act shall be compiled. 24

The review of Georgian Customs environment Transfer of documents to the importer by the driver and informing the importer The driver leaves the parking place, holding the permit pass through the exit at the side of the cabin; The driver passes the document on to the importer in the waiting hall or on the territory adjacent to the central entrance; In case of absence of the information on arrival of the vehicle at the EZR or failure to contact with a driver on the territory of the EZR, the importer approaches the information service desk. 25

The review of Georgian Customs environment Transfer of documents to the importer by the driver and informing the importer • The information service: • Finds out whether the vehicle/transport is on the territory of the EZR according to the plate number of the truck and the name of the importer; • contacts with the administrative officer on duty in order to find the driver; the officer on duty passes the information to the driver (when the driver is around thtransportation mean), in other case he applies a sticker tothe transportaition mean, conveying the request for the driver to show up to the information service desk. 26

The review of Georgian Customs environment Request of the importer to visually examine or/and physically inspect the commodity by the help of experts prior to submission of a declaration of the goods Prior to submission of a declaration, the importer is entitled to request a visual examination and/or physical inspection of the goods through the subsequent experts. For this purpose the importer approaches an operator of the information service. 27

The review of Georgian Customs environment Request of the importer to visually examine or/and physically inspect the commodity by the help of experts prior to submission of a declaration of the goods • The operator: • Informs the importer on the service fees for visual examination, loading/unloading or/and physical inspection of the goods by the help of experts; • Instructs the importer to fill in an application for requesting a visual examination or/and physical inspection of the goods by the help of experts; • Have the officer on duty to determine the time, when a visual examination or/and physical inspection of the goods by the help of experts can be carried out and passes the information to the importer. 28

The review of Georgian Customs environment Assigning a queue number • The operator: • An operator from the information service asks the declarant to produce the number of a registration certificate or the plate number of transportation mean/vehicle or the name of an importer; • After finding the number in the internal database, the operator passes a queue number to the declarant for obtaining a service; • According to the queue number on the electric table the importer goes to fill in a declaration. 29

The review of Georgian Customs environment Filling in a declaration • The process of declaring goods implies binding the presented documents, checking boxes relevant to the list of items and marking with a sticker; • Upon completion of the declaration, thefilling of declaration form is being processed; • Prior to filling in a declaration it is determined whether an importer has any tax arrears left. • In case of arrears presence customs clearance shall be completed, but the goods, in agreement with the corresponding regional center of taxpayer’s registration, shall be moved to another place and the right on lien (will be arrested) will be applied. 30

The review of Georgian Customs environment Filling in a declaration • The terms for submission of declaration or/and arrival of goods or/and transportation means are verified. In case the terms are infringed, an administrative prosecution is instigated. • failure toidentify the documents required for declaration or a commodity code or/and the customs value or/and the weight of the goods or/and the terms of shipment or/and the supplier or/and the country of origin on basis of the submitted documents, the declarant has the right to: • to apply for identification of the goods; • Or request a visual examination or a physical inspection of the goods. • The declaration is assigned with a number and the corridor is to cross by is identified, accordingly. 31

The review of Georgian Customs environment The green or the blue corridors • The declaration is assigned with the A number; • In case of penalties and sanctions the declarant pays • corresponding amount to the bank; • The declaration gets the stamp “Release Permitted” and the • registration/clearance certificate (TIR Carnet)shall be taken of control; • A copy of the declaration and a copy of clearance • certificate and a notification on service fee and customs • duties are passed on to the declarant who is entitled to pay dues out within 5 calendar days. 32

The review of Georgian Customs environment The red corridor • The declaration and the supporting documents are transferred • to the red group whish sends a notification to the declarant on • the time and the place of examination of the truck; • The goods get examined and the examination report is compiled • (if commodity is homogeneous, the examination is undertaken • by means of a scanner. In other cases a physical inspection of • goods is carried out); • If the data given in the declaration correspond those stipulated • in the supporting documents, the declaration is assigned with the • “A” number; • The declaration shall get the stamp “Release Permitted” and the • clearance certificate (TIR Carnet) shall be taken of the control; • A copy of the declaration and a copy of the registration certificate and a notification on the service fee and customs duties shell be passed on to the declarant; 33

The review of Georgian Customs environment The red corridor • If examination discloses non-declared goods of different brand name together with the declared goods or if the commodity does not reconcile with the declared items: • A commodity inspection shall be undertaken by the experts; • Only undeclared goods (the goods of different brand name) • shall be inspected to determine the • customs value and the commodity code; • A case of infringement of customs legislation shall be filed. 34

Elements of Risk Management System Random selection Module Risk criteria Risk criteria Red channel (Physical inspection) Yellow channel (Documentary check) Green Channel (No prerelease check) BlueChannel (post clearance audit) ’’ASYCUDA” Automated System of Customs Data

The review of Georgian Customs environment Departure of a truck from the EZR • At the exit of the EZR an administrative officer takes the seal off • truck and then verifies in the database the release of the clearance certificate (TIR Carnet) off control and the presence of stamped ticket, ‘’Release Permitted’’, on the declaration. • After accomplishment or verification of the aforementioned • procedures the truck is allowed to leave the territory of the EZR. • These procedures and services are located in one place so that the owner of the good do not have to visit several places to submit different documents and make a payment of service fees. 35

The review of Georgian Customs environment Advantages Of EZR • At the EZR the owner of the good is able to: • Promptly fill in and finalize a customs declaration without the need to hire a declarant or a broker; • Examine, load/unload the goods without additional expenses; • Have the goods examined by the experts and the documents translated (if needed) in no time; • Pay duties at place (if he desires so); • Transferthe registered/cleared goods to the importer’s warehouse by transportation means of the terminal. • Have the term of payment of customs duties and the service fees deterred for 5 calendar days from the moment of assigning the number to the declaration when filling in a declaration in the terminal while carrying out the import of goods. 36

The Advantages for starting Business in Georgia under new tax code 37