Download

1 / 5

0 likes | 9 Views

Discover easy ways to calculate your mortgage payments with our top tools and expert tips. Get accurate estimates and make informed decisionsu2014start today!

E N D

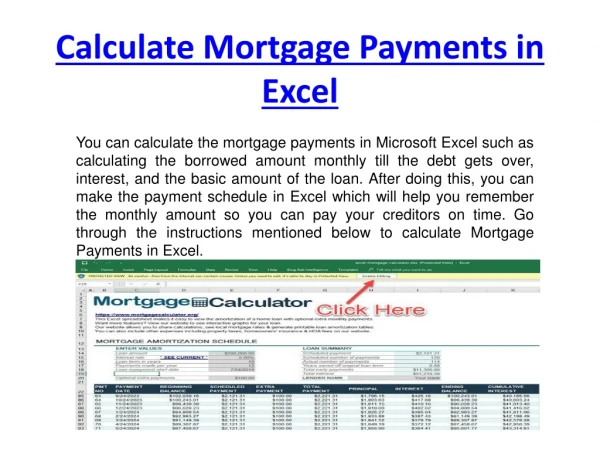

How to Calculate Your Monthly Mortgage Payments: Tools and Tips When you're gearing up to buy a home, one of the biggest questions on your mind is probably, "What will my mortgage payments look like?" It’s a fair question and one that deserves a clear and straightforward answer. After all, knowing what you'll be paying each month is key to planning your finances and ensuring your dream home doesn’t turn into a financial nightmare. So, What Exactly Is a Mortgage? At its core, a mortgage is a substantial loan, usually provided by a bank or a similar financial institution, to help you buy a property—be it a house, a condo, or even a piece of land where you’ll build your future home. But here’s the thing: your property isn’t just yours until you’ve paid off the mortgage. It acts as a security for the loan, which means that if you hit hard times and can’t keep up with your payments, the lender has the right to sell the property to recoup the debt. It’s a sobering thought, but one that underscores the importance of budgeting wisely. Typically, you repay the borrowed amount—plus interest—over a set period. This could be as long as 40 years, depending on your age and what your finances can comfortably handle. It’s a long-term commitment, but one that leads to the pride of homeownership. If you have any questions or concerns about mortgage loans, don't hesitate to reach out. At Think Homewise, we’re here to help you navigate the process and get your online mortgage approval quickly and easily.

Understanding Mortgage Repayments Your mortgage repayment is the monthly amount you pay back to the lender. It’s not just the principal amount (the money you borrowed) but also includes any interest charges. When you sign up for your mortgage, you and the lender will agree on how much you’ll pay each month and when those payments are due. Think of it as a steady march toward full ownership of your home. Each payment brings you closer to the day when the house is entirely yours, free and clear of any debt. Key Factors in Calculating Your Mortgage Payment When planning for a mortgage, understanding the basics of your monthly payment is essential. Let's break down the key components you need to know: 1. PITI: The Four Pillars of Your Mortgage Payment Principal: The amount you borrow to buy your home. Each payment reduces this amount, helping you build equity. Interest: The cost of borrowing is determined by your interest rate. This significantly impacts your overall payment. Taxes: Property taxes vary by location and are based on your home's assessed value. Insurance: Homeowner's insurance protects against potential damage or loss, adding security to your investment. 2. The Role of Your Down Payment Your down payment directly affects your mortgage. A larger down payment means borrowing less, leading to lower monthly payments and less interest paid over time. Down payments typically range from 5% to 20% of the home's price. 3. Understanding PMI If your down payment is less than 20%, you may need to pay Private Mortgage Insurance (PMI). This protects the lender if you default on the loan and is added to your monthly payment. Once you reach 20% equity, PMI can be removed, lowering your costs. How Mortgage Interest Rates Impact You Here’s where it gets interesting. When you borrow money to buy a home, the lender doesn’t just hand over the cash for free. They charge you interest on the loan, which is a percentage of the amount you’ve borrowed. This interest is what makes your monthly mortgage payments higher than just the principal amount. And here’s something to keep an eye on: if your mortgage interest rate changes—something that can happen with variable-rate mortgages—your monthly payments will change too. It’s

always a good idea to use a mortgage calculator to see how these fluctuations might affect your finances, so there are no surprises down the line. In the end, understanding your mortgage payments is all about being informed and prepared. Whether you’re calculating potential payments or learning how interest rates work, having this knowledge helps you make better decisions on your path to homeownership. And remember, while the numbers are important, it’s your dream home that makes it all worthwhile. How can you easily compute your mortgage payments? When it comes to figuring out your mortgage payments, using a regular calculator can be tricky and time-consuming. The formula is complex, and getting it right isn’t always easy. That’s where a mortgage payment calculator comes in handy. With a mortgage calculator, you can quickly and accurately calculate your payments without the hassle of manual calculations. It simplifies the process by taking the guesswork out of the equation, allowing you to focus on planning your finances. There are various types of mortgage calculators available, each designed for different needs. Whether you’re calculating your monthly payments, understanding the impact of extra payments, or comparing different loan options, it’s essential to choose the right tool for the job. This way, you’ll get the most accurate results and make informed decisions about your mortgage. At Think Homewise, we offer a range of tools to help you manage your mortgage with ease. 1) Mortgage Payment Calculator lets you estimate your monthly payments. 2)Closing Cost Calculatorhelps you understand the expenses involved in finalising your purchase. 3) Affordability Calculator provides insights into what you can comfortably afford. For more information and to access these tools, click here. How a Mortgage Calculator Can Guide Your Home Buying Decisions Imagine you’re sitting down with a calculator that’s designed to take the guesswork out of your mortgage payments. This tool takes into account your loan amount, the interest rate you’ve secured, and even the deposit you’ve managed to save up. With these inputs, it gives you a ballpark figure of what your monthly repayments might look like. Now, while this calculator is handy, remember it’s more of a guide than a gospel truth. It’s there to give you an idea, but the actual numbers might differ once all the fine print is settled.

A mortgage affordability calculator is a powerful tool that can simplify the homebuying process by answering crucial questions and helping you make informed decisions. Here’s how it can assist you: Choosing the Right Loan Term: The calculator can show you the impact of choosing a shorter loan term, which comes with higher monthly payments but less interest, versus a longer term with lower payments but more interest overall. Finding the Best Loan Option: By inputting your financial details, the calculator can help identify which loan products you might qualify for, giving you a clear view of your options. Assessing Affordability: It helps you determine how much house you can afford based on your income, credit score, and existing debt, ensuring you don’t overextend yourself. Deciding on a Down Payment: The calculator can guide you on how much to put down, balancing the upfront cost with the potential to lower your monthly payments and possibly avoid mortgage insurance. Renting vs. Buying: When weighing the cost of renting against buying, the calculator helps compare monthly payments and other costs, assisting you in making the best financial decision. Using a mortgage calculator gives you a clearer picture of your financial capabilities and helps you confidently navigate the homebuying process. With the concept of mortgage loans now clear, is there anything else you should consider? Yes, there are additional considerations for your mortgage to keep in mind. When planning your mortgage, it's important to keep a couple of extra factors in mind: 1. Setup Fees: Many mortgages come with arrangement fees and other upfront costs. You can either pay these fees right away or add them to your mortgage balance. If you roll the fees into your mortgage, make sure to factor them into your overall calculations. 2. Fixed vs. Variable Rates: If you choose a fixed-rate mortgage, your payments will stay the same each month for the term you've locked in, usually two to five years. On the other hand, with a variable or tracker mortgage, your payments can change based on fluctuations in the Bank. While it’s difficult to predict future rate changes, it’s essential to consider how potential increases could impact your finances if you opt for a variable rate. Keeping these factors in mind helps ensure you’re fully prepared for the financial responsibilities of your mortgage. Conclusion As you navigate the journey of buying or refinancing your home, understanding the essentials of your mortgage payment is key to making informed decisions. From grasping the impact of PITI to evaluating the benefits of a larger down payment and considering the implications of PMI, every detail plays a crucial role in shaping your financial future.

By leveraging tools like mortgage calculators and staying mindful of additional costs such as setup fees and interest rate fluctuations, you position yourself for success. Remember, a well- informed homeowner is a confident homeowner. So, take control of your mortgage knowledge today and unlock the door to your dream home with clarity and confidence. If you have any questions about mortgage payments or loans, reach out to Think Homewise today, the top mortgage brokers in Ontario. Our team of experts is here to provide you with the guidance you need to make informed decisions and find the best solution for your needs.