Download

1 / 4

0 likes | 13 Views

Wondering if you can switch lenders after mortgage pre-approval? Discover the steps and benefits of changing mortgage lenders for a better deal in our guide!<br>

E N D

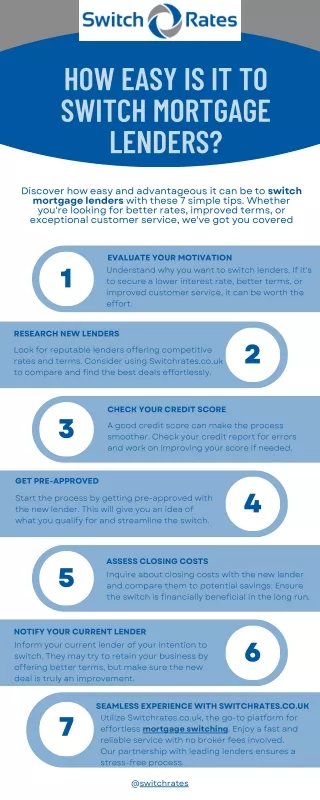

Is It Possible to Change Mortgage Lenders After Pre- Approval? Getting pre-approved for a mortgage is like getting a golden ticket in the home-buying process—it shows sellers you're serious and ready to buy. But what if you find a better deal with another lender after you've been pre-approved? Can you switch lenders without causing problems? Think Homewise understands that the journey to homeownership is filled with decisions and opportunities. In this guide, we’ll explore the ins and outs of switching mortgage lenders post-pre-approval and how online mortgage approval in Canada can give you the flexibility you need. Stay tuned to find out how you can make the best choice for your future home. Can You Switch Lenders? Absolutely, you can switch mortgage lenders after getting pre-approved—but it’s not without its nuances. Think of it as hitting the reset button on your mortgage application with a new lender. This means you’ll need to provide fresh documentation, such as proof of income, bank statements, and credit reports, for the new lender to assess your financial situation.

Switching mortgage lenders at renewal is quite common, but getting the timing right is key. If you’re in the midst of buying a home, you’ll need to ensure this switch happens smoothly within the agreed timeframe, especially if you have a purchase agreement or closing date already set. It’s also important to be aware of how switching lenders might impact your credit score. Each mortgage application involves a hard inquiry on your credit report, which can slightly lower your score. Fortunately, credit bureaus generally treat multiple inquiries within a short period as one when calculating your score, typically within a 14-45 day window, depending on the scoring model. Before making the switch, carefully compare the terms from your current lender and the new one. Consider factors like interest rates, loan terms, and closing costs. Finding a better rate or more favorable terms can make the effort worthwhile, potentially saving your money in the long run. What to Keep in Mind Before switching lenders, here are some additional tips to consider: Shop Around for the Best Deal:Explore multiple lenders to compare their offers. Don’t just focus on interest rates; also consider overall loan costs and terms. Understand the Costs Involved: Be prepared for potential additional costs, including appraisal fees and closing costs. Compare these costs across lenders to find the most cost-effective option. Familiarize Yourself with the Process: Understand the steps involved in switching lenders to avoid any surprises and ensure a smooth transition. Consider Timing: Make sure the switch aligns with your home-buying schedule to avoid potential delays. If you’re feeling confused or need expert advice, don’t hesitate to speak with the advisers at Think Homewise. They can provide guidance to help you make the best decision for your mortgage needs. How to Switch Mortgage Lenders After Being Pre-Approved Switching mortgage lenders after getting pre-approved is a manageable process, but it requires careful planning. Here’s a step-by-step guide to help you make a smooth transition:

Assess Your Current Mortgage Offer: Start by examining your existing pre-approval offer. Consider the interest rate, loan terms, closing costs, and any associated fees. Determine if switching lenders could provide you with better terms or savings. Research and Compare Lenders: Look into different lenders and their mortgage products. Seek out those with competitive interest rates, favorable loan terms, and strong customer service. Compare their rates, fees, and overall reputation to find the best fit for your needs. Apply for a New Pre-Approval: Once you’ve selected a new lender, initiate the pre-approval process with them. Submit all required documentation, such as proof of income, bank statements, and credit reports. The new lender will review your financial details and issue a new pre-approval letter if you qualify. Arrange for a New Appraisal: The new lender will need an updated appraisal to verify the value of the property you’re purchasing. Schedule and pay for this appraisal, ensuring the appraiser has access to the property for their evaluation. Review Closing Costs: Be aware that switching lenders might incur additional closing costs, including appraisal fees, title insurance, and loan origination fees. Compare these costs with your new lender’s offer to make sure they fit within your budget. Notify Your Current Lender: Inform your current lender of your decision to switch. Follow their procedures for transitioning, and ensure they provide any necessary documentation, like the appraisal report, to your new lender. Finalize Your New Mortgage: Once everything is in order and you’re satisfied with the new lender’s terms, move forward to finalize your mortgage. Work closely with your new lender to complete the paperwork and meet any remaining conditions. Close on Your Home: Set up a closing date with your new lender and the involved parties, such as the title company or attorney. Attend the closing meeting to sign the final documents and transfer the funds. With this step completed, you’ll have successfully switched lenders and secured your mortgage. By following these steps, you can ensure a smooth transition to a new lender and benefit from improved mortgage terms.

Pros and Cons of Switching Lenders Switching mortgage lenders can offer several benefits, but it also comes with potential drawbacks. On the positive side, you might secure a lower interest rate, which can lead to significant savings over the life of your mortgage. Additionally, a new lender might provide more favorable terms for a shorter loan duration if you aim to pay off your mortgage sooner. You could also gain access to different mortgage options that better align with your financial goals, such as a fixed- rate loan instead of an adjustable-rate mortgage. However, there are also some cons to consider. One major drawback is the cost of a new appraisal, which can add to your expenses. Switching lenders may involve extra closing costs, including fees for loan origination and title insurance. The process itself can be time- consuming and complex, requiring new documentation and coordination with multiple parties. Weighing these pros and cons carefully will help you decide if switching lenders is the right move for you. Conclusion Switching mortgage lenders after pre-approval is certainly possible, and it can be beneficial if you find a better deal. However, it’s important to weigh the pros and cons and consider factors such as timing and costs. If you’re contemplating making a switch, consider reaching out to a knowledgeable mortgage advisor like Think Homewise for personalized guidance. For those looking to explore their options, Think Homewise offers expert advice and support. Whether you're interested in online mortgage approvalor seeking mortgage pre-approval in Canada, their team is ready to assist you. Contact 1(866) 846-9473 to discuss your mortgage needs and find the best solution for you.