Download

1 / 7

70 likes | 262 Views

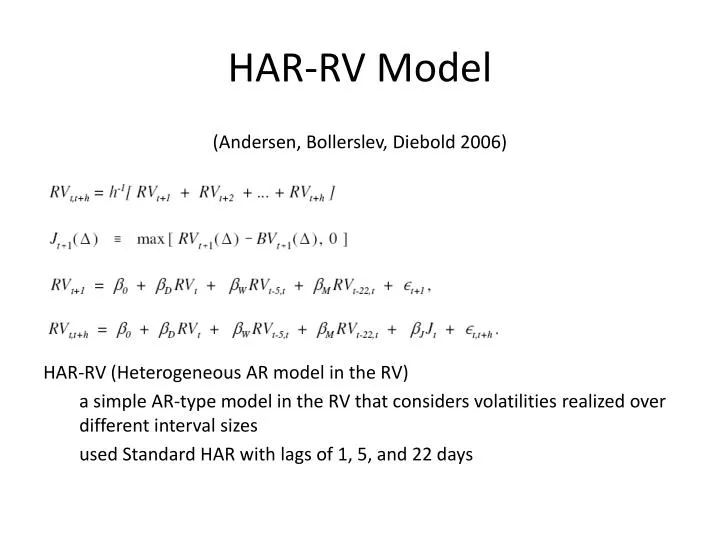

HAR-RV Model. (Andersen, Bollerslev , Diebold 2006) HAR-RV (Heterogeneous AR model in the RV) a simple AR-type model in the RV that considers volatilities realized over different interval sizes used Standard HAR with lags of 1, 5, and 22 days. Stocks Used. 13 stocks:

E N D

HAR-RV Model (Andersen, Bollerslev, Diebold 2006) HAR-RV (Heterogeneous AR model in the RV) a simple AR-type model in the RV that considers volatilities realized over different interval sizes used Standard HAR with lags of 1, 5, and 22 days

Stocks Used • 13 stocks: • AEP, BHI, BRKH, ETR, GOOG, GS, HNZ, KFT, MA, MET, NYX, PM

AIC • Akaike Information Criteria • Measure of the relative goodness of fit • Estimates relative support for a model • SBIC • Schwartz/Bayesian Information Criteria • Measures efficiency of parameterized model in terms of predicting data • Similar to the AIC

VCV • Non-heteroskedasticity robust covariance matrix • VCCV Robust • Heteroskedasticity-robust covariance matrix