Download

1 / 12

120 likes | 258 Views

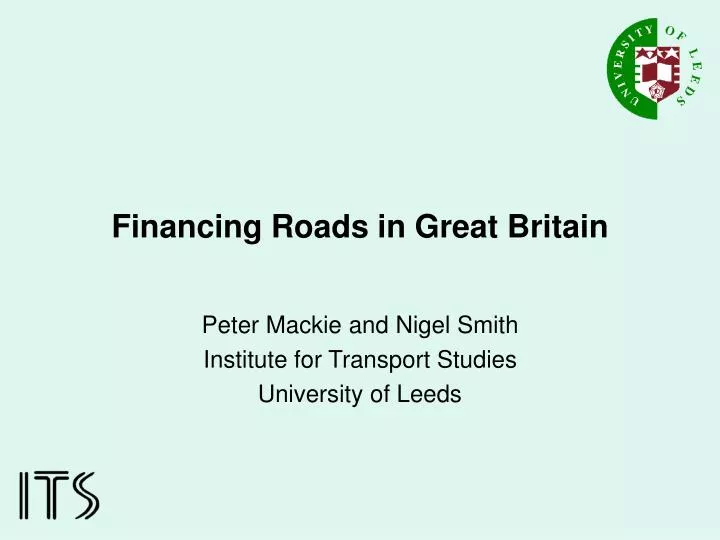

Financing Roads in Great Britain. Peter Mackie and Nigel Smith Institute for Transport Studies University of Leeds. Before 1990. A strong public sector procurement tradition that is to say, public procurement from private construction firms using competitive tendering

E N D

Financing Roads in Great Britain Peter Mackie and Nigel Smith Institute for Transport Studies University of Leeds

Before 1990 • A strong public sector procurement tradition that is to say, public procurement from private construction firms using competitive tendering • Very little tolling of roads therefore few opportunities for privately owned toll-financed schemes • A strict Treasury attitude to private finance (the Ryrie rules): • No additionality. Private finance for sector investment should replace public finance not be additional to it • Risk transfer. Private finance is acceptable provided that genuine risk transfer to the private sector takes place

Exceptions (1) – tolled estuary crossings • Severn and Dartford Crossings running out of capacity; new bridges required • Private concession awarded to take over existing facility and provide a new crossing for the franchise period • Reversion of assets to the Government at the end of the period • Regulated tolls • Some risk transfer, but flexible franchise period implies risk sharing

Exceptions (2) – local development schemes • Private sector financial contributions to public sector schemes • Used where land development requires improved main road or junction connections • Difficulties where multi-developer sites exist – law on planning gain not satisfactory

Private Finance Initiative for Roads (1992) • Economic recession, serious squeeze on public investment. From 1993/4 to 1998/9 • Motorway and trunk road expenditure fell 33% • Local road expenditure fell 50% real • Much interest in private finance. Government relaxed the ‘no additionality’ rule • Private finance acceptable provided • Genuine risk transfer to private sector • Private sector cheaper than via public sector • The PUBLIC SECTOR COMPARATOR

Design, Build, Finance and Operate • Competitive bidding for lowest shadow toll per unit of traffic • Why might going private be cheaper? If the procurement structure achieves efficient risk transfer • Design risk – innovation • Construction risk – claims culture • Operating risk – whole life costing • In general, more effective scrutiny by all parties • But inappropriate risk transfer leads to higher cost – planning risk, ? Traffic risk • Efficiency gains need to more than offset differential cost of capital

The DBFO first generation payment mechanism • Bidders specified ‘bands’ of traffic that would attract different payment amounts. The top band generated no additional return for the concessionaire, so that the procuring agency’s financial exposure was capped • Traffic was divided into vehicles below 5.2 metres in length and above 5.2 metres in length, as a proxy for light and heavy axles to reflect differential maintenance costs • The service availability component was designed to incentivise contractors to complete construction works on time or early • Scheme performance reflected lane-rental charges and highway safety considerations Under this scheme, construction risk, operating risk and a significant proportion of traffic risk was passed to the concessionaire.

Illustration of traffic related shadow toll payment mechanism Annual traffic payment (£ millions) Band 2 6p Band 3 3p Band 4 0p Band 1 9p Maximum payment 9.0 8.1 Central forecast of payment 7.4 6.3 Low forecast of payment 5.3 0 58 70 88 100 130 146 Vehicle kilometres (millions)

National Audit Office and Parliament Reviews (1998) • Capital intensive projects had lower cost via DBFO than conventional procurement. But major maintenance/reconstruction no cheaper and sometimes more expensive • Results sensitive to choice of discount rate for public sector comparator • Need to stimulate the market and to permit technical variations • Need for reliable accurate traffic measurement, and audit of complex financial calculations • Procurement process costly and time consuming. Significantly higher transaction costs than conventional procurement

Private Finance versus Public Sector Comparator for eight tranche one schemes

Since 2000 • Private finance for roads out of favour, tranche 3 of DBFO programme cancelled • DBFO really converts an upfront capital outlay into a mortgage over the life of the asset. Significant % of DfT budget required to pay the mortgages on existing schemes • Reduction in public sector discount rate from 6 to 3.5 per cent makes it very difficult to beat the public sector comparator

The Future • Renewed interest in privately owned and procured toll expressways - M6 Toll around Birmingham now open; Government consulting on extension to Manchester (c.100 kms) • DBFO is currently dead, but lessons • There is a market in innovatory construction • There is a market advantage in private sector control of construction projects • There is an advantage in internalising the whole life costing culture • There is a good case for a design, build, indemnify and transfer form of turnkey contract – private construction management without private finance