Download

1 / 26

260 likes | 271 Views

Explore the world of surety bonds and fidelity coverages that are often required in various industries. Learn about the parties involved in a surety bond contract and the different types of bonds available.

E N D

Surety Bonds and Fidelity Coverages Not Insurance May be sold by insurance companies

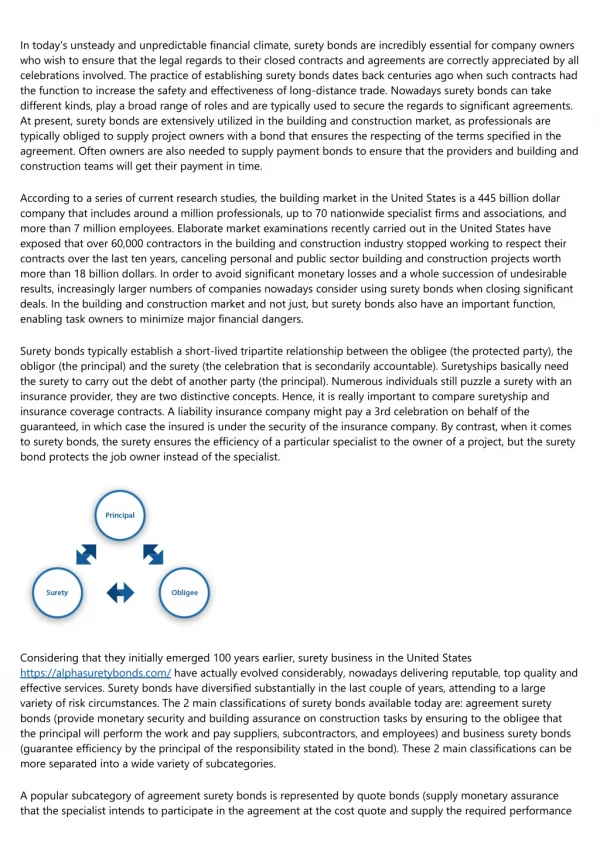

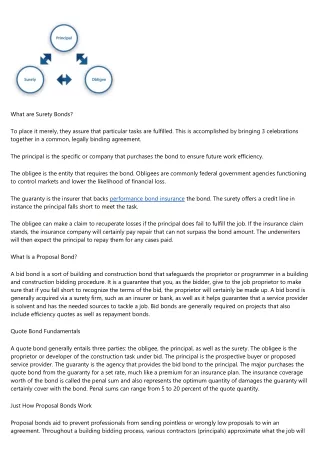

Suretyship 3 Parties to the Surety Bond Contract Surety (a.k.a Guarantor): guarantees to pay oblige if principal defaults Obligee: part to whom the principle owes the obligation PRINCIPAL (a.k.a): agrees to fulfill an obligation Vince promises to do something for Andy, and Tyler vouches for Vince. They sign an agreement promising Andy that, if Vince doesn’t fulfill his promise, Tyler will step in and take care of Vince’s obligations. This is an example of a suretyship.

Suretyship The principal (obligor) is the party that first agrees to fulfill an obligation, and is the one who purchases the bond. The obligee is the party that wants a guarantee that the principal will perform as promised, and is the recipient of the contractual obligation. The surety, or guarantor, is the party (often an insurance or bonding company) that guarantees to the obligee that the principal will fulfill its contractual obligations. If the principal fails to perform, the surety will pay the bond amount to the obligeeand then go after the principal to recover their losses. Vince promises to do something for Andy, and Tyler vouches for Vince. They sign an agreement promising Andy that, if Vince doesn’t fulfill his promise, Tyler will step in and take care of Vince’s obligations.

Suretyship Surety (3rd party – contractor purchases bond from surety): guarantees to pay oblige if principal defaults Obligee (OWNER of apartment complex): part to whom the principle owes the obligation PRINCIPAL (CONTRACTOR): agrees to fulfill an obligation Contractor needs to be bonded in order to get a job building a row of condos. Surety bonds are also commonly required for public adjusters, and some states even require them for independent adjusters. In most states, a public adjuster must be bonded for at least $50,000. If he fails to perform as promised, his surety steps in to fulfill his financial obligation.

Indemnitor • 4th party to a surety bond who agrees to reimburse the surety for losses sustained if the principal defaults

Terms Related to Surety Bonds • Penal Sum • The penal sum is the specified maximum amount the surety will have to pay in the event that the principal defaults. • Collateral • Collateral is cash or valuable property put into a reserve controlled by the surety. The surety holds the cash or property until the principal completes its obligation, at which point the surety returns the collateral to the principal. If the principal does not complete the obligation as promised, the surety has the right to keep the collateral.

Terms Related to Surety Bonds • Joint Control, • the surety establishes dual control over the contractual duty of the principal in order to ensure the work is completed as promised and all disbursements are proper and relevant. • For example, a contractor agrees to build a sidewalk in front of a school. In a Joint Control arrangement, the surety will come in and co-manage the job with the contractor to make sure it gets done correctly, on time, and within budget

Contract Bonds • Bid Bonds: Bid bonds state that the principal is capable of taking on and implementing the project if they are selected during the bidding process. Bid bonds are often required when applying for a contract, and the principal will usually be required to provide a performance or payment bond (or both) if they get the contract. • Performance Bonds: Performance bonds guarantee the completion of a contract. • Payment Bonds: Payment bonds guarantee payment for all labor and materials on a contract. • Subdivision Bonds: Subdivision bonds guarantee that a contractor will meet all the requirements for sidewalks, streets, sewer, and other public works in the completion of a contract. Maintenance Bonds: Maintenance bonds guarantee that the principal will correct any defective workmanship once a project has been finished. • Completion Bonds: Completion bonds guarantee that funds that are loaned for the completion of a project will be

Judicial Bonds • Fiduciary Bond: Guarantees work of someone appointed to take financial responsibility for other • Court (a.k.a Litigation) Bond: Often required of litigants in civil suits to protect opposing parties • Bail Bonds: Court bond that guarantees appearance of a defendant in court • Replevin • https://www.youtube.com/watch?v=mxPOSrRe3Ws (first 60 secs)

Other Bonds • Public official bonds - protect the public from a public official’s lack of performance. The obligee is the state and the principal is the public official. These can be individual or blanket bonds. • Customs bond may be required from individuals or companies that import or export products from other countries. This bond guarantees that the importer or exporter will pay all the necessary customs taxes, fees, and financial responsibilities associated with moving products over international borders. • Financial Guarantee bonds are non-cancellable indemnity bonds, backed by an insurance company, which guarantee that someone who owes money will pay the money back (with the required interest) according to the underlying contractual agreement or promissory note. Debt issuers use financial guarantee bonds as a way of attracting investors.

Other Bonds • Self-insurance workers’ compensation bonds are designed to pay for losses if the self-insured employer cannot meet its obligations. In most states, a company that wants to self-insure its workers’ compensation risk must post one of these bonds. This assures the state that the company will have the necessary resources to pay any workers’ compensation claims that come up • Faithful Performance of Duty bonds pay for losses incurred by an organization or a member of the public because an employee failed to perform his duty. Essentially, this bond covers losses caused by the employee’s dishonesty, negligence, misconduct, bad faith, or malfeasance.

Fidelity Bonds • Fidelity bonds serve a distinctly different purpose than surety bonds. Unlike a surety bond, which guarantees that the principal WILL do something, a fidelity bond guarantees that the principal will NOT do something. • Fidelity bonds are written on a form called the “Employee Theft and Forgery Policy” and they work very much like commercial crime insurance policies. • The obligee is the employer, who pays for the bond, often without the employee even knowing about it. • The surety for this type of bond is the insurer, which promises to pay the obligee • If the principal (that is, the employee) commits certain acts.

Fidelity Bonds • The employer can also choose whether the bond apply on a “loss-sustained” or a “discovery” basis. • A “loss sustained” form is triggered if the actual loss occurs during the policy period, while a “discovery” form is triggered if the employer makes a claim during the policy period, no matter when the loss occurred. • Larceny • Theft • Embezzlement • Forgery • Misappropriation • Wrongful abstraction • Willful misapplication

Fidelity Bonds Policy Period & Limits • The declarations page of a fidelity bond may set a specific policy period, usually from 12:01 a.m. on a specified date to 12:01 a.m. on the same day of the following year, or until cancelled. • The policy uses limits of liability, just like other types of insurance. LIMITS • These dollar amounts can be set as single loss or aggregate limits, and they are part of the insuring agreement. A “single loss” limit includes all losses caused by the same person or employee or resulting from a common series of acts. • An “aggregate limit” is the total dollar amount the insurer has agreed to provide for all losses discovered during the policy period.

Scheduled Fidelity Bonds • Applicable to only select employees or positions • Employees can be bonded for different amounts • Limit of liability is per name/position scheduled • Premiums based on amount of coverage, number of individuals scheduled and their coverage amounts, business activities of the insured and deductible amounts • Typically used in businesses where employees have greater responsibilities or handle large sums of money

Blanket Fidelity Bonds • Cover ALL Employees of the named insured unless specifically excluded • New employees are automatically covered • All employees are bonded for same aggregate amount • Limit applies per occurrence • Premium based on amount of coverage requested, total number of all employees insured’s business activites, and amount of deductible • Common uses for blanket bonds include businesses with large number of employees and organizations with voluntary or honorary positions.

Employee Retirement Income Security Act • Employee Retirement Income Security Act (ERISA) regulates most types of employee benefit and pension plans. ERISA requires that every fiduciary of an employee benefit plan and every person who handles funds or other property of those plans must be bonded. These bonding requirements help protect employee benefit plans from risk of loss due to fraud or dishonesty on the part of people who handle the plan funds.

Standard Form No. 14 for Brokers/Dealers Eligibility • Stockbrokers of securities listed on stock exchanges • Stock exchanges • Securities investors • Investment bankers and trusts • Mutual funds • Commodity brokers • Stockbrokers operating on a partnership basis

Standard Form No. 15 for Finance Companies Eligibility • small loan companies, • mortgage bankers, • title insurance companies principally engaged in mortgage business, • holding companies who manage stocks and securities for others, • real estate investment trusts, and • finance companies that primarily finance paper for and through dealers and those licensed under the Small Business Administration Act.

Standard Form No. 23 for Credit Union Blanket Bond • Standard Form No. 23 - Credit Union Blanket Bond - Written for credit unions, mutual benefit associations and remedial loan associations in Connecticut provided they do not grant or extend accident, health, death, or burial benefits to their members. This is also written for National Credit Union Share Insurance Fund.

Standard Form No. 24 for financial institution • used by national and state commercial banks and trust companies, American agencies for foreign banks, title insurance companies that accept deposits or act as trust companies, Federal Reserve banks, and federal home loan banks. • The Standard Form 24 is also available by rider for savings banks, and savings and loan associations.

Standard Form No. 25 - Insurance Companies Blanket Bond • The Standard Form 25 is a blanket bond used by all kinds of insurance companies, including life insurance, title insurance, self-insurance, and risk retention groups. It contains the following insuring agreements: Fidelity coverage is for losses caused directly by the fraudulent or dishonest acts of employees who are either acting alone or in collusion with others. • On Premises coverage protects against losses due to burglary, robbery, unexplainable disappearance, damage, destruction, theft, or larceny by someone on the premises. • In Transit coverage includes loss of property caused by robbery, larceny, theft, misplacement, disappearance, damage, or destruction while the property is in transit, whether in the care of a messenger or in the custody of a transportation company. • Forgery or Alteration coverage includes losses directly resulting from the forgery or alteration of any instrument specified in the insuring agreement. And finally, Securities coverage protects against losses caused when the insured deals in specified securities that have been forged, altered, lost, or stolen.

Standard Form No. 28 - Insurance Companies Blanket Bond • Excess Bank Employee Dishonesty bond. It is used with any of several other financial Institution bonds to provide excess employee fidelity coverage.

Public Employee Dishonesty Coverage • Coverage Form O is also known as Public Employee Dishonesty Coverage. It is insurance for government entities that covers loss caused by employee dishonesty. • The limit in the Coverage Form O is applied on a per occurrence basis. A similar form, Coverage Form P, applies the limit on a per employee basis.

Review of Fidelity Bonds • Standard Form 24 – Commercial banks, trust companies, Federal Reserve Banks, saving and loan associations • Standard Form 14 – stockbrokers, stock exchanges, investment bankers • Standard Form 15 – Finance companies • Standard Form 23 – Credit unions • Standard Form 25 – insurance companies • Stand from 28 0 excess employee fidelity coverage