Download

1 / 23

230 likes | 244 Views

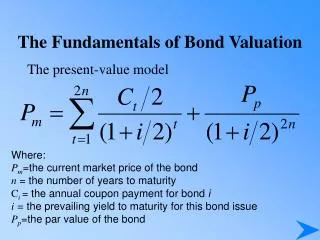

Join our conference to prepare for the bond market, covering economic indicators, rate forecasts, and various types of municipal bonds. Learn about the current historic interest rates and where they might be headed, based on expert opinions. Gain insights into Unlimited Tax General Obligation Bonds, Limited Tax General Obligation Bonds, Revenue Bonds, and more. Discover important IRS rules and bond rating grades that impact interest costs. Understand the key factors for bond ratings and financial management policies. Explore examples of ratings and essential points for a rating presentation. Finally, delve into taxing options, public vs. private bond sales, and unique characteristics of different communities.

E N D

WCMA Summer Conference Preparing For The Bond Market August 18, 2016 8:45 AM Jim Nelson Bond Underwriter, Senior Vice President Phone: (206) 389-4062 Email: jnelson@dadco.com Columbia Center, 701 Fifth Ave., Suite 4050 Seattle, WA 98104 Website: www.davidsoncompanies.com/ficm

Overview • Surprisingly, interest rates are near a historic low • Voters have been more supportive of tax measures • More WA municipal bonds are being rated • Due diligence and continuing disclosure requirements • Planning ahead can help to achieve a lower interest cost

2 Economic Indicators

3 Economic Indicators

4 Home Prices in Central Puget Sound

Where are Rates Headed? According to the GO BankingRates, July 18, 2016 article, “2016-2017 Interest Rate Forecast: How to Get the Best Interest Rates”: The Wall Street Journal reported in July 2016 that Daniel Tarullo, a Fed governor, said that before raising interest rates, the Fed should wait until there’s more evidence that the inflation rate is closer to the Fed’s 2 percent target, and that inflation would remain near that level. During the Fed’s mid-June 2016 meeting, the board of governors indicated that before raising interest rates, they need more economic data in order to show that the economy is growing, said Tarullo. Confirming Tarullo’s prediction is Jack McIntyre, a chartered financial analyst, senior research analyst and portfolio manager for the global fixed-income fund at Brandywine Global Investment Management. McIntyre predicts that the Fed will not raise interest rates during the rest of 2016. Given the over $8 trillion of sovereign bonds with negative yields, Treasury bonds will continue to be attractive to investors, McIntyre said.

Types of Bonds • UNLIMITED TAX GENERAL OBLIGATION BOND(Voted) – • A bond that is secured by the full faith, credit and taxing power of a • municipality. Secured by a pledge of the special excess levy for the life • of the bond. • LIMITED TAX GENERAL OBLIGATION BOND (Non-voted) – • A type of municipal bond that is guaranteed by the municipality’s pledge to use all legal resources, including the levying of property taxes up to a set statutory limit. If a municipality exhausts the property tax resources for bond repayment within that limit, other revenue sources must be used for bond repayment. • REVENUE BOND – • Revenue bonds are payable from specific sources of revenue (typically water and sewer system revenues). • LOCAL IMPROVEMENT DISTRICT (LID) BOND – • A bond payable from special assessments levied on the benefited properties within a local improvement district. The special benefit for the properties is an increase in property value. The amount of the assessment on the property owner must be less than the estimated increase in property value from the LID improvements.

Some IRS Rules To Remember • IRS Spend Down Requirements • Spend 85% of bond proceeds within 36 months of the Delivery Date. • Bank-Qualified Status • There may be an interest cost savings if a municipality issues $10,000,000 or less in the calendar year. • Reimbursement Resolution • If the City is considering the use of cash for capital improvements, you may want to consider a Reimbursement Resolution.

Bond Rating Grades • A rating grade helps to achieve a lower interest cost. • Investors view the rating grade as an indication of risk. • A higher rating grade results in lower interest rates.

Debt Factors Economy The Rating Management Factors Key Factors For the Rating Bond raters consider the local economy, finances and other factors. Financial Performance

Financial Management Policy A Financial Management Policy is a set of financial policies to achieve financial integrity, assist the elected officials and staff in financial management, and provides continuity over time as elected officials and staff members change. • Cash/Reserve Fund goals • Communication • Use of Debt • Budgeting and Forecasting • Periodic Review of Plans and Policies

Examples of Limited Tax General Obligation Ratings Notes: Stanwood’s Revenue Bonds are rated AA-. Moody’s puts more weight on economic factors. They also assign one grade lower with a Limited Tax General Obligation Bond. S&P puts more weight on the financial factors. They do not distinguish between Unlimited Tax and Limited Tax Bonds.

Key Points for a Rating Presentation • Summary of Strengths • Description of the Bonds • City Management • Financial History • Revenue Sources • Description of local and regional Economy • Policies • Unique Characteristics of your community

Examples of Taxing Options Levy Lid Lift EMS Levy Excess Levy Voted Bond Sales Tax Increase Utility Tax Increase New taxing jurisdiction

Public Bond Sale vs Private Placement • Public Bond Sale • Typically a lower borrowing cost (depending on term & amount) • Involves preparing the Official Statement and a Rating Presentation • Involves more work by City staff • Typical time frame is 8 to 12 weeks • Private Placement • The financing costs are lower. • Typically a higher borrowing cost (depending on term & amount). • Does not require preparing the Official Statement and Rating Presentation. • Involves less work by City staff • Typical time frame is 6 weeks

Continuing Disclosure • Must have a Continuing Disclosure Undertaking (“CDU”) • with a Bond sale. • SEC Rule 15c2-12 regulates bond underwriters and the municipalities. • CDU is the responsibility of the municipality. (We are happy to assist you!) • Upload information on the Electronic Municipal Market Access (known as “EMMA”) information system by September 30th each year. • Typical information required for a Limited Tax General Obligation Bond: • annual financial statement • assessed value • regular property tax collections • regular property tax levy rate • outstanding general obligation debt • Upload Audit Report within 10 business days of publish date. • Disclose credit related events within 10 business days of occurrence.

Steps to Ensure Future Compliance • Establish policies and procedures. • Assign the responsibility to 2 people. • Set up calendar reminders. • Review the EMMA website. See the following helpful links: • http://www.msrb.org/educationcenter/issuers/disclosing.aspx • http://www.msrb.org/msrb1/training-tutorials.aspx • http://www.msrb.org/msrb1/emma/pdfs/EMMACDManual.pdf

Key Points To Plan Ahead Have you updated your Financial Management Policy? Do you need to adopt a Reimbursement Resolution? Consider market timing and bundling multiple purposes into one financing. THANK YOU!

Public Finance Services • Debt Structuring and Analysis • Disclosure and Continuing Disclosure • Financial Advisory • Direct Placement to Banks • Rating Agency Analysis and Presentations • Ongoing Service after the Bond sale: • Assist with communications between the municipality and rating agency • Assist with Continuing Disclosure and Material Event Notices • Fixed and Variable Debt • Taxable and Tax-exempt • Refunding Bonds • Revenue Bonds • Planning for LID and ULID Projects • Non-voted Bonds • Voted Bonds and Tax Levy Impact • Planning for a Voted Bond and the voter education process

Davidson’s Public Finance Team Mark Froio (Senior Vice President) – Full time bond underwriter, located in Seattle. Extensive market knowledge and experience to achieve lower interest rates. (Mark has 30 years of experience.) Maura Lentini (Vice President) – Former Moody’s rating analyst, assists with rating agency presentations. (Maura has 16 years of experience.) Crystal Vogl (Vice President) – Disclosure Expert preparing Official Statements and assisting with Continuing Disclosure requirements and deadlines. (Crystal has 16 years of experience.) Suzanne Eide (Vice President) – Bond Structuring/Quantitative Expert for voted bonds, non-voted bonds, revenue bonds, LID bonds and refunding bonds. (Suzanne has 15 years of experience.)

Neither this material nor any of its contents may be disclosed, sold, or redistributed, electronically or otherwise, without prior written consent of Davidson Companies. The information presented herein is based on public information we believe to be reliable, prevailing market conditions, as well as our views at this point in time. We make no representation or warranty with respect to the accuracy or completeness of this material. Past performance is not necessarily indicative of future results. Davidson Companies does not assume any liability for any loss which may result from the reliance by any person upon such material. We make no representations regarding the legal, tax, regulatory, or accounting implications of entering into a Transaction. Required Disclosure Pursuant to MSRB Rule G-23: An underwriter’s primary role will be to purchase as principal, or arrange for the placement of the securities in a commercial arm’s length transaction with the issuer, and may have financial and other interests that differ from those of the issuer. In its capacity as underwriter and not as financial advisor, an underwriter may provide incidental financial advisory services at the issuer’s request, including advice regarding the structure, timing, terms and other similar matters concerning the issuance. However, an underwriter does not assume any financial advisory or fiduciary responsibilities with respect to the issuer.