Download

1 / 27

270 likes | 367 Views

The MARKETING RESEARCH AND INTELLIGENCE ASSOCIATION Ottawa Chapter would like to acknowledge the support of the following organizations. Without their kind support we could not continue to offer quality programs such as ……. 2005 Canadian Technologically Advanced Family Survey.

E N D

The MARKETING RESEARCH AND INTELLIGENCE ASSOCIATION Ottawa Chapter would like to acknowledge the support of the following organizations. Without their kind support we could not continue to offer quality programs such as ……

2005 Canadian Technologically Advanced Family Survey October 27, 2005

Table of Contents • About the 2005 Canadian Technologically Advanced Family Survey • Overview • Telephony • Internet • Home Networking • Wireless • Conclusions and Recommendations

About the 2005 Canadian Technologically Advanced Family Survey Background • Yankee Group has conducted the Canadian Technologically Advanced Family (CTAF) Survey since 1999. It captures information about consumer adoption of and potential interest in communications products and services. • Using a proprietary index, we segment Canadian households into the following categories: Technologically Advanced Families (TAFs), Early Mass, Late Mass and Laggards. By doing this we can identify households across the adoption spectrum, ranging from early-adopting TAFs to late-adopting Laggards. • More specifically, the survey measures: • Penetration of and consumer demand for communications, computing and entertainment products • Consumers’ interest in new products, technologies, services, packages and providers • Consumers’ perceptions of service providers and willingness to switch

About the 2005 Canadian Technologically Advanced Family Survey (continued) Methodology • We collected data using a survey that was mailed to randomly selected Canadian households in May and June 2005. • The survey consisted of 34 pages and covered entertainment (cable/satellite), telephony products and services, wireless products and services, home computing, online/internet, home networking, single service provider (bundling), and information on consumer attitudes, lifestyle and background. • We collected 1,103 surveys.

Table of Contents • About the 2005 Canadian Technologically Advanced Family Survey • Overview • Telephony • Internet • Telephony • Bundles • Television • Wireless • Conclusions and Recommendations

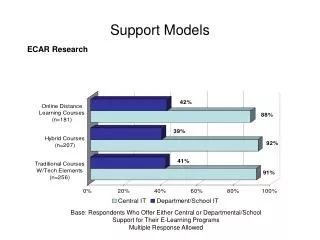

Consumer Profile Avg. Cdn. Households TAFs Early Mass Late Mass Lag Mean Household Income $66,169 $80,899 $70,899 $63,799 $44,749 Households with Children 40% 62% 52% 34% 12% Home-Based Business1 12% 23% 15% 9% 7% 8% VoIP Awareness 28% 54% 36% 22% High-Speed Data2 77% 95% 84% 70% 32% Services Home Networking 20% 65% 34% 3% 0% Digital Cable3 28% 50% 37% 21% 11% HDTV4 9% 22% 10% 4% 0% 81% 81% 37% PCs 100% 94% Devices MP3 Player 66% 40% 0% 25% 12% Total Monthly Communications and Entertainment Spending2 $209.07 $247.25 $214.41 $194.55 $181.67 Spending Market Segmentation Is Becoming Increasingly Important to Drive New Product and Technology Growth 1 Anyone in household 2 Of those with internet access 3 Of those with cable or satellite 4 Those with HDTV-compatible sets Source: Yankee Group 2005 Canadian Technologically Advanced Family Survey

Table of Contents • About the 2005 Canadian Technologically Advanced Family Survey • Overview • Telephony • Home Networking • Telephony • Bundles • Television • Wireless • Conclusions and Recommendations

Local Telephony Enjoys Relatively High Levels of Satisfaction with Providers The same can’t be said about all other services, especially in less technologically advanced households. How satisfied are you with your service provider? Somewhat Satisfied/Very Satisfied Source: Yankee Group 2005 Canadian Technologically Advanced Family Survey

In 2005, Fewer Canadian Households Cited the Phone Company as Their First Choice for a Bundled Services Provider Which company would be your first choice to provide bundled services? Note: In 2003, satellite and cable companies were combined into a single category. Source: Yankee Group 2005 Canadian Technologically Advanced Family Survey

Cablecos Are Less Attractive as Local Telephony Service Providers Applying the same discounts for local telephony services, cablecos would generally attract less interest than another phone company if customers look to switch. How likely would you be to switch local providers? Source: Yankee Group 2005 Canadian Technologically Advanced Family Survey

Although VoIP Awareness Remains Low, Key Target Segments Show Significantly Higher Awareness Have you ever heard of voice over Internet Protocol (VoIP) telephone service? Cable and telephone companies launched service in 2005 without reference to VoIP technology. All providers may be able to win market share by touting technology features to savvy customers in the high-awareness categories above. Source: Yankee Group 2005 Canadian Technologically Advanced Family Survey

Although Consumer Confusion and Mixed Perceptions of VoIP Continue, the Low-Priced Service Message Is Clearest What is your opinion on how VoIP telephone service compares to regular phone service? • Consumers easily identify the trade-off represented by the niche and alternative providers: low cost comes with an apparent sacrifice in quality. • A relatively low number have no opinion of the quality of the various elements—roughly 12% overall. Source: Yankee Group 2005 Canadian Technologically Advanced Family Survey

The Triple Play Is the Best Defense Against Churn to Cable Companies How likely are you to switch voice service to your cable company if the price were the same or 10% to 15% less? • Customers who currently combine phone service with two of internet, wireless or television from a single provider are significantly less likely to consider churning to a cable TV provider for telephone service (“phone” = LD and local). • Sample sizes are small, but a triple play of phone, wireless and internet appears to provide the best protection against churn. Source: Yankee Group 2005 Canadian Technologically Advanced Family Survey

Table of Contents • About the 2005 Canadian Technologically Advanced Family Survey • Overview • Telephony • Internet • Telephony • Bundles • Television • Wireless • Conclusions and Recommendations

Photo Sharing, Blogging and Voice Calls See Big Usage Gains in 2005; Only Dating Declines Which of the following have you used the internet for in the past month? Base: Online households Source: Yankee Group 2005 Canadian Technologically Advanced Family Survey

Table of Contents • About the 2005 Canadian Technologically Advanced Family Survey • Overview • Telephony • Internet • Home networking • Bundles • Television • Wireless • Conclusions and Recommendations

Home Networking Took a Big Leap from 2004 to 2005 A strong majority of TAF households are wired, with a significant number connected wirelessly. Almost all networked homes use a broadband pipe for internet access. • Percent of total online households with home networks: • 25% in 2005 • 16% in 2004 95% of TAFs, 94% of Early Mass households and 91% of Late Mass households have high-speed networks. Note: Of households with internet access Source: Yankee Group 2005 Canadian Technologically Advanced Family Survey

Shared Internet and Printer Access Are Clearly the Main Drivers for Home Networking What were your top reasons for buying a home network? Applications such as entertainment and gaming appear as secondary and tertiary considerations for the mass market. Note: Among users with a home network Source: Yankee Group 2005 Canadian Technologically Advanced Family Survey

Table of Contents • About the 2005 Canadian Technologically Advanced Family Survey • Overview • Internet • Home Networking • Telephony • Bundles • Television • Wireless • Conclusions and Recommendations

TAFs Are Likely to Port Their Wireless Numbers, While Non-TAFs Are Not Would you be more likely to switch wireless providers if you could keep the same wireless number? Source: Yankee Group 2005 Canadian Technologically Advanced Family Survey

Consumers Are Generally Happy with Their Mobile Services Few respondents rated their provider as underperforming across a range of metrics. Source: Yankee Group 2005 Canadian Technologically Advanced Family Survey

Table of Contents • About the 2005 Canadian Technologically Advanced Family Survey • Overview • Internet • Home Networking • Telephony • Bundles • Television • Wireless • Conclusions and Recommendations

Conclusions and Recommendations • Consumer adoption of network-reliant, PC-independent devices such as game consoles, cameras and music players continues to rise, fueling demand for high-speed access and home networks. • Voice over IP is gaining awareness both in its own right and as a technology-neutral phone company alternative. It will drive further network dependence. • Even as Canadians indicate price sensitivity, an appetite for network-reliant communications and entertainment creates loyalty to single providers. Simple, reliable offerings resonate strongly as sophistication in technology adoption increases. However, as technology savvy rises, consumers seem more willing to consider a switch to another service provider based on price. The advantage of premises presence must be bolstered with bundle offers to defend against churn. • Wireless and television constitute the biggest spending within the communications bundle. New technologies such as ITV that enhance the TV experience will drive loyalty to the service providers at premium prices—with the hope of creating technology advantages with a greater likelihood of sticking than current platform offerings.

Conclusions and Recommendations (continued) • Consumers seem generally pleased with the level of service they are receiving from their providers. Pricing offers will be well received but will not be the primary driver to incumbent churn. Instead, growth opportunities are linked to content, technology and applications, especially in the area of entertainment content. For example, interactive, user-centric web applications saw big gains in 2005 that create opportunities for third-party content producers and the service providers that integrate them. • The current marketplace will see a natural evolution in the next several years as 2- and 3-year contracts expire to an environment of technological and pricing parity. In the next decade, market share will move toward duopoly as non-event-related churn affects both cablecos and telephone providers in the natural course of business. • Our survey data indicates an environment in which a significant change in quality of service (as Rogers experienced during the migration from @Home in 2001 and Bell Mobility experienced with billing very recently), high-bar-setting new applications and technologies, or very aggressive pricing will be the key determinant in whether the cablecos or telcos win or lose the battle for market share.

Jeff Leiper Director jleiper@yankeegroup.com Carrie MacGillivray Analyst cmacgillivray@yankeegroup.com www.yankeegroup.com 2005 Canadian Technologically Advanced Family Survey Canadian Market Strategies