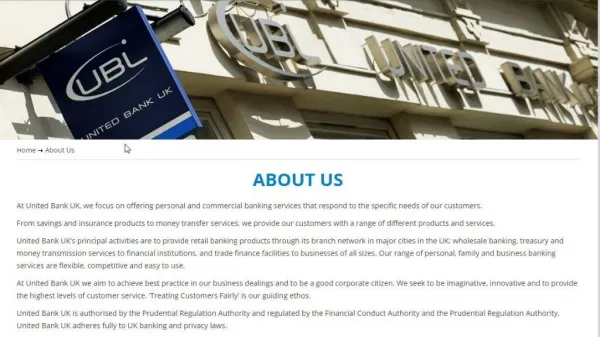

UBL- The Best Banking Industry

http://www.ubluk.com UBL is one of the most efficient banking institutions incorporated in UK. We are authorized by Prudential Regulation Authority and regulated by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA). We have our headquarters in Pakistan. UBL has emerged as the second largest private bank in Pakistan whose main shareholder is the best way group. With our share holder UBL has the presence across some major financial centers in the world. We offer you wide range of services for the customers in international level. Our main services include personal banking, commercial banking, islamic banking, foreign exchange, loans, currency exchange, online banking which provides the customer a long time benefits in their future endeavors. The personal banking services provided by us are one of the best. We provide you all the personal banking services under a single roof that offers you the assistance to open accounts and access a range of competitive products. All our personal finance services are underpinned by niche market expertise with a highly personalized and supportive customer relationship team. With our commercial banking services we provide you the complete working capital that is required for your business. So banking with us will certainly credit you a lot of offers and benefits in the long run.

221 views • 9 slides