Download

1 / 12

120 likes | 296 Views

Impact of Mortgage Rates on New Home Construction in Rhode Island. Jon Bradner Michael Cancilliere Justin Larson Christopher Vacca. Abstract.

E N D

Impact of Mortgage Rates on New Home Construction in Rhode Island Jon Bradner Michael Cancilliere Justin Larson Christopher Vacca

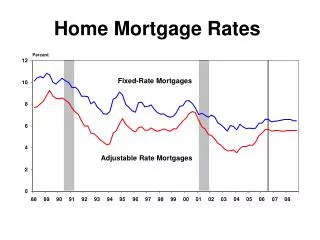

Abstract • Over the past 5 years we have seen massive financial upheaval, shattering of many of our long held beliefs about home ownership and the housing market as a whole. • In October 2007, the U.S. Secretary of the Treasury called the bursting housing bubble "the most significant risk to our economy.“ • Factors that have long been cornerstones of the housing market have undergone significant change. Variables such as household income, unemployment rates, foreclosure rates, and fluctuations in property taxes and mortgage rates have all undergone significant, fundamental changes in the past 5 years. • Our study explores how relevant some previously trusted ‘guides’ are in the new economic landscape. Specifically we will seek to prove the Ho: Mortgage rates continue to have a significant impact on New Home construction rates. • This will be done by using statistical regression to analyze the impact of the above variables against changes in demand for new Home Construction. We will be seeking to prove our Ho, and by doing so begin to build a model that will allow us to identify the variables that impact one of our country’s leading economic indicators: New Home Construction.

Previous Work: Studies & ArticlesBefore 2011 Emrath 2005: Increased study is needed to determine what factors outside of Mortgage rates impact home construction and sales: • Changes in interest rates can significantly impact the ability to afford a house. This presents a conflict of ideas as previously high interest rates suggested an increased demand for housing. • However, in the current market, interest rates may be changed to ward off inflation or as part of other government regulations. Fei Liu & Emrath 2008: The impact of home building on the economy • Household income should impact new home construction in regards to forcasting buying power • it should also be viewed as an indicator of new home construction rates. A decline in new home constructions may correlate with a decline in income (due to loss of construction related jobs and industry), which may further decrease demand and interest rates.

Previous Work: Studies & ArticlesDuring 2011 Dietz & Siniavskaia 2011:On October 1, 2011, some mortgage loan limits and corresponding interest rates for the government-sponsored enterprises dropped from their levels to stricter limits (established in 2008). • This would reduce housing demand and place downward pressure on prices. As home sales are inter-related, this pressure on prices could spill over on other homes reducing the overall demand for housing • limit the willingness of contractors to embark on new home constructions. Emrath 2011: Government regulations can impact new home construction • Increased regulations tend to drive up costs and prices, necessitating a high level of demand to price competitively. • There is not a high demand for homes and there exists a significant glut in supply as millions of homes are in foreclosure and short-sale situations. Quint 2011: Quint projects that homes built as early as 2013 will be smaller and more efficient, which in turn may mean reduced costs for the buyer, yet in turn mean lower profits for the builder or seller. • This is significant as it is another factor that can play into new home construction as well as interest rates as rates appear to be largely governed by demand.

Model Data: Hypothesis: The demand for new home construction can be explained by mortgage rates. • Use ordinary least squares linear regression model. • Unemployment Rate • Mortgage Rate • Average Household Income • Average Property Taxes • Median Home Price • Total Home Sales • Percentage of Foreclosed Homes No Intercept Linear Regression Model b0 = 0 P-Value of Intercept = .205 Y=b1x1i + b2x2i + b3x3i + e • Y = Number of new home constructions (Dependent Variable) • X1 = Mortgage Rates • X2 = Total Home Sales • X3 = % of Homes Foreclosed • E = Standard Error

Results • Mortgage rates and Total Home Sales have positive parameters. • Percentage of Foreclosed Homes has negative. • P Value = 0.00001 • F Value = 69.19 • R-Squared = 82%

Results • One of the four regression assumptions is the absence of the collinearity or that independent variables must be independent from other independent variables • The test for the multicollinearity is determined by the value for VIF with a value below at least 10 but preferred to be below 5 indicating an absence of collinearity • Average VIF – 1.333

Results • White’s test for homoscedasticity = 15.648 • P-Value for White’s test = 0.07461

Results Variables Mortgage Rates Total Home Sales % of Home Foreclosures Elasticity • 1.683 • 0.377 • -0.546 • As demand for new homes increase so do mortgage rates • As demand increase so does total homes • % of home foreclosures decreases when the demand for new homes increase

Conclusion The production of new home construction is correlated to mortgage rates: • The hypothesis proves to be correct, that mortgage rates have a significant impact on production. • The higher the mortgage rate, the more demand there is for new home construction. • Basically, the more demand there is for financing, the higher interest rates will rise. More studies could be done to determine what other economic indicators would be appropriate to hedge against mortgage rates for new construction.

Policy Rhode Island was one of the hardest hit states in terms of foreclosures. • As mortgage rates stay low, or go down, the state should create incentives for purchasing homes that have been abandoned/foreclosed because it would be economically inefficient for new construction. • However, without new home construction jobs, Rhode Island will also need to create a similar job market for those skilled in new home construction. • As mortgage rates rise, the state should encourage tear downs of abandoned/foreclosed homes, in order to maximize new construction income

Bibliography • How Government Regulation Affects the Price of a New Home., Emrath, Paul, Ph.D. Economics and Housing Policy Group, National Association of Home Builders: http://www.nahb.org/generic.aspx?sectionID=734&genericContentID=161065&channelID=311 • Interest Rates and House Prices: the “Priced Out” Effect., Emrath, Paul, PhD. Housing Policy, March 2011: http://www.nahb.org/generic.aspx?genericContentID=37153 • GSE and FHA Loan Limit Changes for 2011: Scope of Impact, Dietz, Robert, Ph.D., and Siniavskaia, Natalia Ph.D., 2011., Economics and Housing Policy Group, National Association of Home Builders: • The Direct Impact of Home Building and Remodeling on the U.S. Economy., Helen Fei Liu, Helen and Emrath, Paul. October 2008 • The New Home in 2015., Quint, Rose, Economics and Housing Research, Freddie Mac: http://www.freddiemac.com/news/finance/ • Interventions in Mortgage Default: Policies and Practices to Prevent Home Loss and Lower Costs, Cutts, Amy and Merrill, William A., March 2008., Freddie Mac Working Paper #08-01: http://www.freddiemac.com/news/pdf/interventions_in_mortgage_default.pdf • The Housing Landscape for America’s Working Families 2005, Lipman, Barbara J., New Century Housing Vol. 5, Issue 1, April 2005, • Freddie Mac Website: http://www.freddiemac.com/news/finance/