Download

1 / 10

110 likes | 304 Views

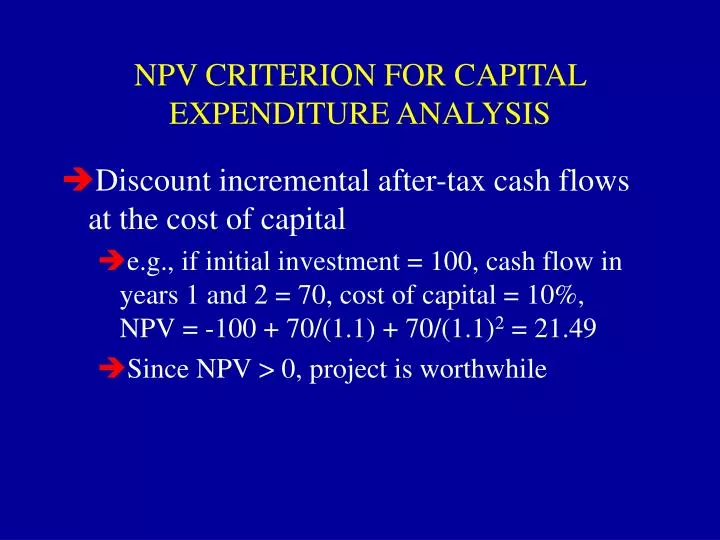

NPV CRITERION FOR CAPITAL EXPENDITURE ANALYSIS. Discount incremental after-tax cash flows at the cost of capital e.g., if initial investment = 100, cash flow in years 1 and 2 = 70, cost of capital = 10%, NPV = -100 + 70/(1.1) + 70/(1.1) 2 = 21.49 Since NPV > 0, project is worthwhile.

E N D

NPV CRITERION FOR CAPITAL EXPENDITURE ANALYSIS • Discount incremental after-tax cash flows at the cost of capital • e.g., if initial investment = 100, cash flow in years 1 and 2 = 70, cost of capital = 10%, NPV = -100 + 70/(1.1) + 70/(1.1)2 = 21.49 • Since NPV > 0, project is worthwhile

NPV AND SHAREHOLDER WEALTH • Firm has no debt • Existing assets generate cash flows of 100 per year forever • Discount rate = 10% • Firm has 20 mil shares currently selling at $50 per share

NPV AND S/H WEALTH (CONT.) • Now firm plans to invest $120 in new project • Project will generate $20 CF per year forever • Firm will issue n new shares at price P* to finance project

NPV AND S/H WEALTH (CONT.) • Equating sides of post-project bal. sheet: 100/.10 + 20/.10 = 20P* + nP* • But from original bal. Sheet: 100/.10 = 20x50 = nP • And since we need to raise 120 for project: 120 = nP* • Thus: 20x50 +20/.10 = 20P* + 120

NPV AND S/H WEALTH (CONT.) • Rearranging: 20/.10 - 120 = 20 x (P* - 50) • Or: [20/.10 - 120]/20 = (P* - 50) • Or: NPV per share = change in wealth for original shareholders

COST OF CAPITAL What is it? • Appropriate discount rate • Minimum acceptable rate of return for investors • Investors’ opportunity cost • Required compensation for risk borne by investors

COST OF CAPITAL (all-equity financing) What rate of return will shareholders demand? Two possible answers from stock market: • Capital Asset Pricing Model rE = rf + (rM - rf) (shareholders demand compensation for systematic risk) • Dividend Discount Model rE = D1/P0 + g

COST OF CAPITAL (with debt and equity) E = equity mkt. value ATOCF = after-tax operating cash flow rD = cost of debt rE = cost of equity D = value of debt T = corporate tax rate

COST OF CAPITAL (debt and equity cont.) Cross-multiplying by V, we derive a discount rate for the company as a whole Note that debt ratio is measured at market value

COST OF CAPITAL FOR A PROJECT • For a project, the cost of capital is project specific, not company-specific (Would a risky project be any less risky if undertaken by a currently safe company?) • Cost of capital should reflect business risk of this project • Cost of capital should reflect long-run financing mix for this project