Download

1 / 77

780 likes | 980 Views

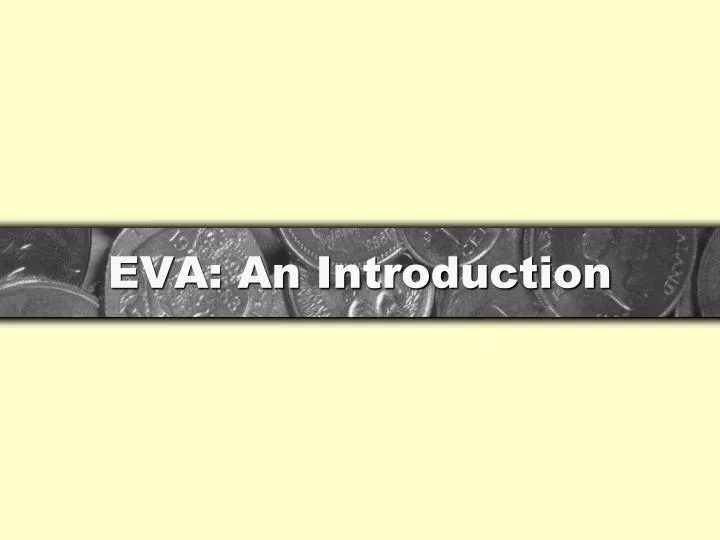

EVA: An Introduction. How Much Systemic Waste Is There In A Supply Chain?. 11.4%. A benchmark comparison. of programs to reduce. incoming materials cost. PPI. Cumulative U.S. Cumulative U.S. Producer Price. Producer Price. Index. Index. 7.56%. 7.56%. 7.1%. 7.0%. Experience of a.

E N D

How Much Systemic Waste Is There In A Supply Chain? 11.4% A benchmark comparison of programs to reduce incoming materials cost PPI Cumulative U.S. Cumulative U.S. Producer Price Producer Price Index Index 7.56% 7.56% 7.1% 7.0% Experience of a Experience of a well well - - regarded U.S. regarded U.S. 3.3% .7% manufacturing firm manufacturing firm 1/92 1/92 1/92 1/92 1/93 1/92 1/92 1/94 1/92 1/92 1/95 1/92 1/96 1/92 1/92 1/92 1/97 1/92 1/92 1/98 1/92 A benchmark comparison of programs to reduce incoming materials cost FIN 591: Financial Fundamentals/Valuation

A Great Deal More Than Most People Recognize! 11.4% A benchmark comparison of programs to reduce incoming materials cost PPI Cumulative U.S. Cumulative U.S. Producer Price Producer Price Index Index 7.56% 7.56% 7.1% 7.0% Experience of a Experience of a well well - - regarded U.S. regarded U.S. 3.3% .7% manufacturing firm manufacturing firm .7% .7% .7% .7% - - .2% .2% 1/92 1/92 1/92 1/92 1/93 1/92 1/93 1/92 1/94 1/92 1/94 1/92 1/95 1/92 1/95 1/92 1/96 1/96 1/92 1/92 1/92 1/97 1/92 1/97 1/98 1/98 1/92 1/92 - - - - 3.1% 3.1% 3.1% 3.1% Results from Results from Honda of America Honda of America program program - - - - 7.9% 7.9% 7.9% 7.9% A benchmark comparison of programs to reduce incoming materials cost - - - - 16% 16% 16% 16% - - - - 19% 19% 19% 19% FIN 591: Financial Fundamentals/Valuation

Honeywell’s Stock Price Where to from here? FIN 591: Financial Fundamentals/Valuation

How Value is Created • Management makes decisions, hopefully, with benefits exceeding costs • Benefits may be near or distant future • Costs should include direct investment costs + cost of capital • True source of value-enhancing projects • Firm’s comparative or competitive advantage. FIN 591: Financial Fundamentals/Valuation

Comparative Advantage • Advantage one firm has over another in terms of • Cost of producing or • Distributing goods/services • Example: • Wal-Mart invested in regional warehouses and distribution system • Reduces the need for retail inventory • Replenish store inventory quickly. FIN 591: Financial Fundamentals/Valuation

Competitive Advantage • Advantage one firm has over another because of structure of the markets in which they operate • Barriers to entry • Patents • Capital requirements • Regulation • Influence over suppliers • Influence over buyers Must be sustainable to be a true competitive advantage FIN 591: Financial Fundamentals/Valuation

Fuzzy Finance FIN 591: Financial Fundamentals/Valuation

Return on Investment • Compare benefits (numerator) with resources (denominator) affecting that benefit • Basic earning power ratio • EBIT / Total assets • Return on assets • Net income / Total assets • Return on equity • Net income / Book value of equity Measured relative to what? FIN 591: Financial Fundamentals/Valuation

Effective SCM:Increased Shareholder Value Shareholder value • Greater customer service (higher market share, increased gross margins). • Greater product availability • Lower cost of goods sold, transportation, warehousing, material handling and distribution management costs • Lower raw materials and finished goods inventory • Shorter ‘order-to-cash’ cycles • Fewer physical assets (e.g. trucks, warehouses, material handling equipment) Revenue Profitability Costs Working capital Invested capital Fixed capital FIN 591: Financial Fundamentals/Valuation

Pro’s & Con’s • Benefits of these ratios • Ease of calculation & interpretation • Decompose to reveal sources of changes • Downside of these ratios • Sensitive to choice of accounting method • Accumulation of monetary values from different periods • Backward looking • Fail to consider risk. FIN 591: Financial Fundamentals/Valuation

Honeywell’s Performance NetRevenues NetIncome Earnings / Share FIN 591: Financial Fundamentals/Valuation

EPS: Opiate of the Executive Suite • EPS is such an unreliable measure of value that managers often make “dumb” decisions to increase it • Prompts managers to misallocate capital • Treats retained earnings as a free source of capital • Promotes retaining capital and using it wastefully. FIN 591: Financial Fundamentals/Valuation

EPS… • Accounting rules discourage EPS-manic managers from spending capital on value enhancing investments in intangibles like brands, research and training • Why? • GAAP requires outlays to be written off immediately against earnings. FIN 591: Financial Fundamentals/Valuation

EPS… • EPS focus may cause management to refrain from issuing equity at times when the company really needs it • Fabricate EPS gains by using more debt than prudent • Both on and off the balance sheet • Accept weak projects that happen to be financed with debt. FIN 591: Financial Fundamentals/Valuation

EPS… • Earnings manipulation often used • Establish reserves • Invest pension funds in equities • Extreme cases, make up numbers as you go • Worldcom and HealthSouth. FIN 591: Financial Fundamentals/Valuation

EPS… • Today’s market perception: “Management that aims to boost earnings at the expense of quality will be more certainly penalized then ever before with a lower stock price and a sullied reputation.” FIN 591: Financial Fundamentals/Valuation

Performance vs. Valuation • Performance measurement • Relies on actual results • Historical • GAAP vs. GAP • Valuation • Relies on forecasts • A firm’s stock price relies on investors’ expectations, not historical performance. FIN 591: Financial Fundamentals/Valuation

Statement of Cash Flows • SCF combines balance sheet and income info • Eliminates the “sins of accrual accounting” • SCF consists of: • Operating cash flows • Investing cash flows • Financing cash flows. Free cash flow FIN 591: Financial Fundamentals/Valuation

Cash Flow Not the Answer • Cash flow has problems as a valid performance measure • So long as investments in projects earn a return higher than shareholders could earn by investing on their own, then the more investment a company makes and the more negative its cash flow becomes, the higher its share price will be. • Think Wal-Mart. FIN 591: Financial Fundamentals/Valuation

Better Than Some Alternatives • Accounting profits versus cash operating profits • Cash flow frequently defined as: Net income + depreciation or as EBITDA • Poor definition • Honeywell’s trend... FIN 591: Financial Fundamentals/Valuation

Free Cash Flows • Definition: • After-tax operating earnings + non-cash charges - investments in operating working capital, PP&E and other assets • It doesn’t incorporate financing related cash flows • Represents cash flow available to service debt and equity. • When used in capital budgeting proposals • Based on expectations. FIN 591: Financial Fundamentals/Valuation

FCF & Capital Budgeting • FCF is the method of choice of most firms for evaluating capital budgets • Identify incremental • Investment in PP&E + working capital • Revenues • Costs (excluding financing) • Depreciation tax shields. FIN 591: Financial Fundamentals/Valuation

Common Techniques • Evaluation techniques: • Payback • Accounting rate of return • DCF analysis • Consists of NPV and IRR • DCF analysis is not a problem in theory • Only in practice. FIN 591: Financial Fundamentals/Valuation

NPV Methodology • Net present value (NPV) • Estimate of change in the value of equity if the firm invests in the project • Forward looking • If NPV>0 • Investment is expected to add value • If NPV<0 • Investment is expected to erode value • Decision rule • Invest in projects expected to enhance value. FIN 591: Financial Fundamentals/Valuation

A Capital Budgeting Example Excellent NPV and IRR Accept the project! FIN 591: Financial Fundamentals/Valuation

NPV(Using FCF) Profile NPV of FCF = $125.86 Significant info revealed? FIN 591: Financial Fundamentals/Valuation

Internal Rate of Return • Practice is to compare IRR with weighted average cost of capital • Problem: • IRR fails to measure scale or growth • It sees no difference between earning a 20% return on a $1 million investment or a $1 billion investment • These two projects are very different with distinctly different NPVs. FIN 591: Financial Fundamentals/Valuation

IRR Profiles(New Example) Mn IRRATL =36.53% • IRRNE=19.63%

Conflicts: NPV & IRRWhich to Choose? NPV Marketing Campaign IRR = 16.35% Discount rate 10% 10.7% Product development IRR = 13.24% Select project with higher NPV (product development project)

Value Enhanced? • Once a project is applied, the investment becomes buried in the balance sheet • How is its contribution measured? • No idea whether project generates value • Accounting measure relied upon • EBITDA and EPS generally increase • Means Bonuses probably will be paid • Motivation: • Get your hands on as much capital as possible. FIN 591: Financial Fundamentals/Valuation

Buried in the Balance Sheet FIN 591: Financial Fundamentals/Valuation

Focused Finance FIN 591: Financial Fundamentals/Valuation

EVA & Shareholder Value • What is the best way to measure shareholder value? • Fortune 500 sales? • Earnings per share? • Business Week survey of market value of equity? • Stock market share price? • Market value added? FIN 591: Financial Fundamentals/Valuation

EVA & Other Measuresof Performance FIN 591: Financial Fundamentals/Valuation

EVA & Wealth Creation • Warren Buffet: We feel noble intentions should be checked periodically against results. We test the wisdom of retaining earnings by assessing whether retention, over time, delivers shareholders at least $1 of market value for each $1 retained. • Translation: Ultimate litmus test of any company’s success lies in increasing its market value by more than it increases its capital. FIN 591: Financial Fundamentals/Valuation

View of the Firm • Value of firm = Value of debt + value of stock • Market value of a company reflects: • Earning power of invested assets • Present value of current operations • Present value of expected improvement in operating performance. Market Valued Balance Sheet Assets Debt Equity FIN 591: Financial Fundamentals/Valuation

What is Required to Focus? • Tie performance methods to capital budgeting techniques: • Economic value added (EVA) • Market value added (MVA) • Want to gauge management’s performance • Focus on: • Decisions made in the past to help project the future. Links to NPV FIN 591: Financial Fundamentals/Valuation

What is MVA? • MVA = Market value of capital - book value of capital Honeywell’s MVA = ? • Key elements: • Calculation of market value of capital • Market value of debt + market value of equity • Calculation of capital invested • Accounting adjustments necessary • MVA Related to EVA. FIN 591: Financial Fundamentals/Valuation

Market Value Added Market value added Premium Total market value Debt & equity capital Investment FIN 591: Financial Fundamentals/Valuation

Also, Market Value Added Expected improvement in EVA MVA = Present value of all future EVA • MVA Total market value Debt & equity capital Current level of EVA FIN 591: Financial Fundamentals/Valuation

EVA & Market Value • Market value of a company reflects: • Value of invested capital • Value of ongoing operations • Present value of expected future economic profits • Captures improvement in operating performance • EVA related to market value by: • Measuring all the capital • Seeing what the firm is going to do with the capital • Turn FCF forecasts into EVA forecasts • Discount EVA. FIN 591: Financial Fundamentals/Valuation

What is EVA? • EVA = Economic profit • Not the same as accounting profit • Difference between revenues and costs • Costs include not only expenses but also cost of capital • Economic profit adjusts for distortions caused by accounting methods • Doesn’t have to follow GAAP • R&D, advertising, restructuring costs, ... • Cost of capital accounted for explicitly • Rate of return required by suppliers of a firm’s debt and equity capital • Represents minimum acceptable return. FIN 591: Financial Fundamentals/Valuation

Advantages of EVA • Annual EVA is easy to interpret • Correlations between market value and various measures: • Standardized EVA 0.50 • ROE 0.35 • Fortunes “Most admired firms” 0.24 • Cash flow growth 0.22 • EPS growth 0.18 • Dividend growth 0.16 • Sales growth 0.09 • 50% of change in market value explained by standardized EVA (Standardized EVA = EVA / Capital). FIN 591: Financial Fundamentals/Valuation

Components of EVA • NOPLAT • Net operating profit after tax • Operating capital • Net operating working capital, net PP&E, goodwill, and other operating assets • Cost of capital • Weighted average cost of capital % • Capital charge • Cost of capital % * operating capital • Economic value added • NOPLAT less the capital charge. FIN 591: Financial Fundamentals/Valuation

What is NOPAT? Net sales 150,000 Cost of sales 135,000 Depreciation 2,000 SG&A 7,000 Net Operating profit 6,000 Taxes @ 40% 2,400 NOPAT 3,600 Excludes financing charges FIN 591: Financial Fundamentals/Valuation

What is Operating Capital? • Capital: Net operating assets adjusted for certain accounting distortions • Asset write-downs, restructuring charges, … • Net operating assets: • Cash, receivables, inventory, prepaids • Trade payable, accruals, deferred taxes • Net property, plant, and equipment • Exclude non-operating assets: • Marketable securities, investments,... FIN 591: Financial Fundamentals/Valuation