Download

1 / 18

190 likes | 486 Views

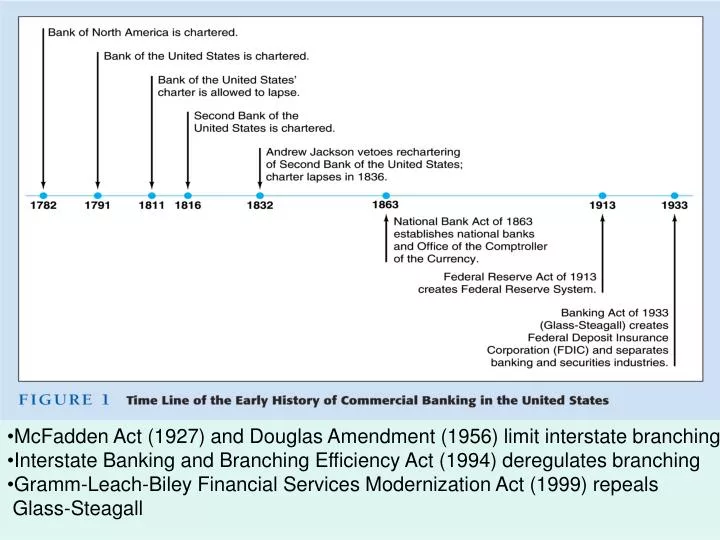

McFadden Act (1927) and Douglas Amendment (1956) limit interstate branching Interstate Banking and Branching Efficiency Act (1994) deregulates branching Gramm-Leach-Biley Financial Services Modernization Act (1999) repeals Glass-Steagall. Regulating Finance. Lots of bases to cover

E N D

McFadden Act (1927) and Douglas Amendment (1956) limit interstate branching • Interstate Banking and Branching Efficiency Act (1994) deregulates branching • Gramm-Leach-Biley Financial Services Modernization Act (1999) repeals • Glass-Steagall

Regulating Finance • Lots of bases to cover Cover one by regulation or deregulation Unintended Consequences • Reactions to regulatory policies frustrate regulator intent Regulate bank balance sheets off-balance sheet activities Emplace a safety net bankers become skydivers • Regulation spreads to cover innovations complexity ineffectiveness Win by gaming the system

Primary Supervisory Responsibility of Bank Regulatory Agencies • Comptroller of the Currency—national banks chartered by Federal government since 1863 • Federal Reserve and state banking authorities—state banks that are members of the Federal Reserve System • Fed also regulates bank holding companies • FDIC—insured state banks that are not Fed members • State banking authorities—state banks without FDIC insurance

Innovations: Response to Interest Rate Volatility • Adjustable-rate mortgages • Financial Derivatives Innovations: Response to Information Technology • Bank credit and debit cards • Electronic banking • ATM/Home banking/ABM/Virtual banking • Junk bonds • Commercial paper market … backed by banks • Securitization Innovations:Avoiding Regulation/Loophole Mining • Sweep accounts … reserve requirements • Money Market Mutual Funds … Regulation Q

Decline of Traditional Banking • Decline in cost advantages in acquiring funds (liabilities) • Rising inflation rise in interest rates and disintermediation • Low-cost source of funds, checkable deposits, declined in importance • Decline in income advantages on uses of funds (assets) • Information technology less need for banks to finance short-term credit • and issue loans • IT lower transaction costs for other financial institutions • Bank Responses: • Riskier Lending … Commercial real estate, leveraged buyouts, takeovers • Off balance sheet activities

Size Distribution of Insured Commercial Banks, September 30, 2008 ???? 3,046 4,039 486 86 7,640 39.9 52.9 6.1 1.1 1.3 9.7 10.0 79.0

Ten Largest Non – US Banks, December 30, 2008 • Ten Largest Banks in the World, 2007 $ Revenues • ING Group, Netherlands 6. BNP Paribas, France • Fortis, Belgium/Netherlands 7. Credit Agricole, France • Citigroup, US 8. Deutsche Bank, Germany • Dexia Group, Belgium 9. Bank of America, US • HSBC Holdings, UK 10. UBS, Switzerland

Bank Consolidation Interstate Banking and Branching Efficiency Act, 1994 • Skirting branch restrictions • ATMs, Bank Holding Cos. • Skirting branch restrictions • ATMs, Bank Holding Cos. Geographic deregulation • Pre-Crisis Findings: • Net interest margin up • ROA, ROE up for big • banks • Intrastate deregulation • more positive for all but • big banks • Interstate deregulation • helps big banks most • Non-performing loans • down for biggest banks • but up for smaller banks • State of economy has • stronger impact on bank • performance than • branching deregulation • Benefits of bank consolidation • Increased competition close inefficient banks • Efficiencies from economies of scale and scope • Lower chance of failure -- diversified portfolios • Costs • Fewer community banks less lending to small business • Banks in new areas increased risks/failures

The U.S. regulatory regime: In need of reform? Sources: Financial Services Roundtable (2007), Milken Institute.

Asymmetric Information and Bank Regulation Government safety net • Deposit insurance and FDIC • Short circuits bank failures and contagion effect • Payoff method • Purchase and assumption method • Fed as lender of last resort: Too BIG to Fail • Financial consolidation Exacerbates Too Big to Fail • Safety net extended to non-bank financial institutions Safety Net Moral Hazard Problems • Depositors don’t impose discipline of marketplace • Banks have an incentive to take on greater risk Safety Net Adverse Selection Problems • Risk-lovers find banking attractive • Depositors have little reason to monitor bank

Attempted solutions: Constrain banks from taking too much risk • Promote diversification • Prohibit holdings of common stock • Set capital requirements … Capital as cushion • Minimum leverage ratio • Basel Accord: risk-based capital requirements … but there’s regulatory arbitrage Prompt corrective action: Close ‘em down when capital inadequate • Monitor … CAMELS • Capital adequacy • Asset quality • Management • Earnings • Liquidity • Sensitivity to market risk • Disclosure requirements … mark-to-market issue • Restrictions on competition … make banking boring

Failed Banks Update Year Number • 2000 2 • 2001 4 • 2002 11 • 2003 3 • 2004 4 • 2005/2006 0 • 2007 3 • 2008 QI+Q2 4 • 2008 Q3 10 • 2008 Q4 12 • 2009 Q1 21 • 2009 Q2 24 • 2009 Q3 50

1980s S&L and Banking Crisis • Financial innovation increased risk taking • Increased deposit insurance moral hazard • Deregulation • Lack of management expertise • Rapid growth in new lending: real estate • Activities expanded in scope • Regulators at FSLIC lacked expertise • High interest rates/recession increased incentives for moral hazard

1980s S&L and Banking Crisis: • Regulatory forbearance by FSLIC • Insufficient funds to close insolvent S&Ls • Established to encourage growth • Did not want to admit agency was in trouble • Zombie S&Ls taking on high risk projects and attracting business from healthy S&Ls • Politicians lobbied by S&L interests • Competitive Equality in Banking Act of 1987 • Inadequate funding • Continued forbearance

The Financial Institutions Reform, Recovery, and Enforcement Act of 1989 • Regulatory apparatus restructured • Federal Home Loan Bank Board relegated to the OTS • FSLIC given to the FDIC • RTC established to manage and resolve insolvent thrifts • Cost of the bailout approximately $150 billion • Re-restricted asset choices • Increased core-capital leverage requirements • Imposed same risk-based capital standards as those on commercial banks • Enhanced enforcement powers of regulators • Did not resolve underlying moral hazard and adverse selection problems