Download

1 / 31

330 likes | 454 Views

Explore the nature of industry, market structures, implications of perfect competition, normative properties, and the farm problem. Learn about concentration ratios, market classifications, and indices to assess industrial competitiveness.

E N D

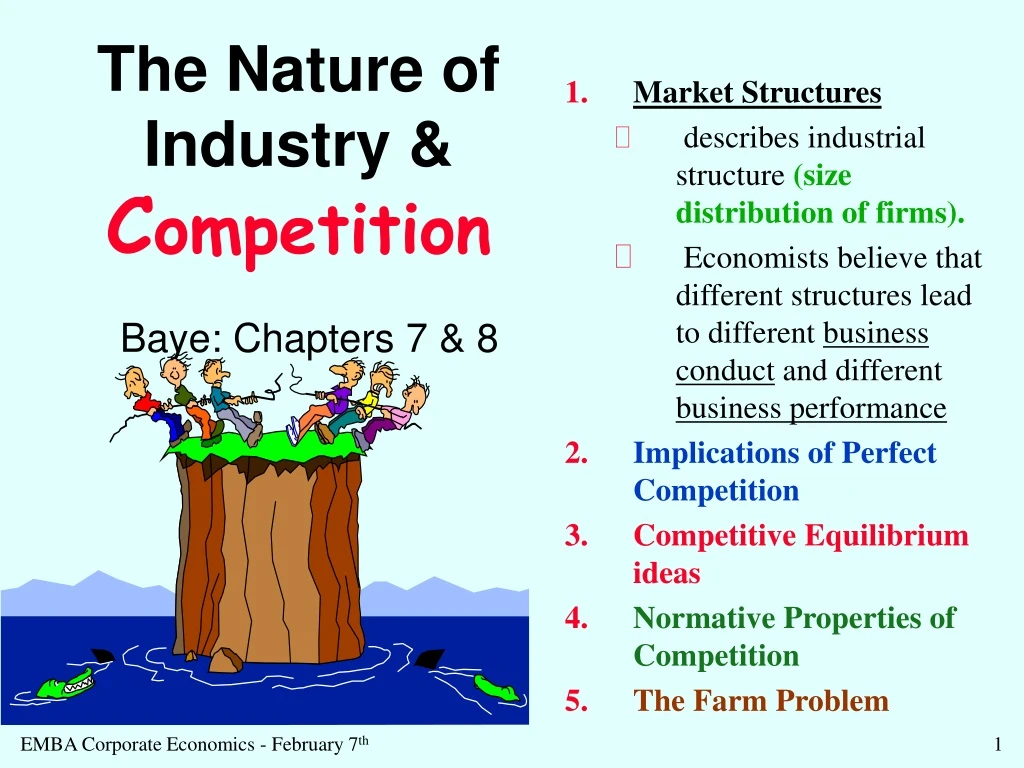

The Nature of Industry & Competition Baye: Chapters 7 & 8 Market Structures describes industrial structure (size distribution of firms). Economists believe that different structures lead to different business conduct and different business performance Implications of Perfect Competition Competitive Equilibrium ideas Normative Properties of Competition The Farm Problem

Baye Chapter 7 The Nature of Industry • A market is a group of economic agents that interact in a buyer-seller relationship. • The nature of that relationship is affected by the number and size distribution of both buyers and sellers. Size is most measured by annual sales or by market capital (outstanding shares*market price) • A popular measure of seller concentration is the percentage of an industry comprised of the top 4 firms. • Similarly, the top 4 buyers is a popular measure of buyer concentration.

Incomplete Measures of Industry Concentration • Providing all the market shares can reveal too much • Partial measures use only some of the market shares • 4, 8, 20 & 50 firm Concentration Ratios • Share of top 4 firms, as in 4CR = 60 • Problem of two industries in terms of SALES where weights for each is Salest/SalesT A has shares of 60, 10, 5 & 5 B has shares of 20, 20, 20 & 20 • The knowledge of each share is hidden or obscured in partial measures of concentration in an industry Both A& B are 4CR=80

Other Market Concentration Measures Complete Measures • Know the market shares of all of thefirms • Herfindahl Index:H = S wi2ranges 0 to1 Note: 1/H is the equivalent number of equal sized firms. If H = .2, then this is like a 5-firm industry. • HHI = 10,000*S wi2goes from 0 to 10,000

Industrial and firm classifications • North American Industrial Classification System (NAICS)of the US Department of Commerce replaced SIC’s in 1997. Industry Classifications • 2-digit sectors: 32 Manufacturing sector • 3-digit sub-sectors: • 322Paper Manufacturing Sub-sector • 4-digit industry groups: • 3221 Pulp, Paper, and Paperboard Mills • 5-digit industry in North America: • 32212 Paper Mills • 6-digit industry in US, Canada, or Mexico: • 322121 Paper Mills in the US except newsprint • CUSIP:Committee on Uniform Security Identification Procedures -- American Bankers Association: unique security identification system To compare NAICS to SIC see: http://www.census.gov/epcd/naics/naicstb1.txt

Rothschild Index • R = ET / EF • Where ET is the price elasticity of the total market, as in the price elasticity of paper is -1.5 • Where also is the price elasticity of the firm, as in the price elasticity of Fort Howard is -1.7 • R = -1.5 / -1.7 = .88, and ranges from 0 to 1. • The closer the Rothschild Index is to zero, the more competitive the industry Lerner Index: L = -1/Ep Good for comparing two industries w.r.t. potential market power • Note: P (1 + 1/E) = MC, will be optimal pricing, so it turns out that L = (P - MC)/P & P = (1/(1-L)) MC, a markup factor • As Lerner index rises, ability to exercise monopoly power increases (usually 0 to 1). Zero is no markup is competition.

Conditions of Market Structure 4 Basic Conditions 1. The number of sellers & their size distribution 2. The number of buyers & their size distribution 3. Product differentiation or heterogeneity 4. Entry and exit conditions

Baye: First half of Chapter 8 Perfect Competition Our chief interest will be the effect of structure on PRICE Assumptions of Perfect Competition A S S U M P T I O N S • Many buyers & many sellers (or many firms) • 2. Homogeneous or undifferentiated • product (or standardized, homogeneous) • Buyers & sellers have perfect information • 4. There are no transaction costs • 5. Free entry & exit (no barriers) Page 266

IMPLICATIONS: 1. Firms are PRICE TAKERS Suppose P1 < P2. But then, no one buys from firm 2. Ergo, one price. P d d firm’s demand curve MC Q 2. A firm’s demand curve isperfectly elastic at the competitive price

3. Profit Maximization implies each firm produces at a quantity where P = MC Maxp= P•Q - TC(Q) p /Q = 0 implies that: P = MC 4.The firm’s MC curve is the firm’s SUPPLY CURVE MC { prices As price changes, the optimal amount SUPPLIED changes quantities

Equilibrium Price in a Competitive Market • Equilibrium for each firm if P = MC. Each firm is “happy” • Equilibrium for the industry if: Demand equals Supply at the going price • When both occur, the market is in a Competitive Equilibrium MC MC AC D a firm the industry CAN EARN ECON PROFITS IN THE SHORT RUN

A Competitive Equilibrium Implies: 1. Competitive firm can earneconomic profitsin SR 2. In LR, entry forces price down to the minimum of the AC curve 3.If Price < AVC, firm will shut down. The “shut down price” is at minimum AVC. MC See Figure 8-5 on Page 273 AC P AVC The shut down price

NORMATIVE PROPERTIES of Competitive Markets: 1. The Division of Output Among Firms is EFFICIENT Suppose 2 firms with different MC curves MC MC firm 1 firm 2 If firm 2 expands and firm 1contracts production, TC rises.

2. The total output of the Industry is CORRECT, i.e., Maximizes the Sum of Consumer & Producer Surplus supply CS Consumer surplus is area Below demand and Above price PS demand Producer surplus is area Below price and Above supply Correct output Too little output Too much output

3. In the LR, each firm produces at the lowest point of their AC curves MC AC PLR Q (at least cost point) 4. Political Decentralization 5. Price signals the true cost to society 6. Economic profits are zero in the LR

LR Supply Curve for a Firm • Expect to see a region of declining cost • Constant cost • And increasing cost IRS LR firm supply DRS CRS MES minimum efficient scale Q

LRSupply for an Industry in Competitive Markets • The LR Supply curve can be flat, rising, or falling. • Constant Cost Industries • Input prices are constant and CRS • Every firm has identical costs • Increasing Cost Industries • Rising factor prices (factor-price effect) • Or Heterogeneous firm efficiencies • Or Decreasing Returns to Scale • Decreasing Cost Industries • Either Declining Factor prices or IRS LRS Q LRS Q LRS Q

Two Theories on Competition & Price • The MORE firms there are, the greater is competition, and the lower is price • Contestable Markets -- Potential Entry as well as actual number of firms, so the number of actual firms empirically may not matter PRICE of Air Travel no impact after a certain number of firms N = number of firms

Dorothy in The Wizard of Oz, may be taken from Mary Lease of Kansas, in 1890s, who called for less corn and more hell. Price declines since the Civil War exacerbated the ‘Farm Problem’ Economic hardship in agriculture sent millions to the cities for work Policy choices include: Tariffs, but led to tariff war and the Great Depression Farm-price support, but leads to widening excess supply Acreage restrictions, but benefits other countries the most Ethanol requirements, but less fuel efficient as it take oil to make ethanol Or, phase out subsidies altogether as in New Zealand Raising Less Corn and More HellMBN Chapter 21 Depression era pp. 132-138

The Case of Agricultural Markets • Long run supply shifted out faster than demand, exemplified by Idaho Potatoes versus Canadian potatoes, and a potato glut. • Declining employment, but improved incomes for the remaining • The ‘Good/Bad Paradox’ is that a bad year for crop growth can be a good year for farmer incomes

Potato Industry and Individual ProducerPrices per 100 lb. S1 MC A A $8 $8 ATC S2 $2 AVC B B $2 D D Q2 Q1 Q1 Q2

The Long-Run Decline in Farm PricesThough we’ve seen a jump in prices due to Ethanol. S1 S2 • Demand grows from D1 to D2 • But Supply shifts out from S1 to S2 • The end result, the price is lower and the quantity greater • Lower employment in this sector • Paradox of Composition – What is good for one isn’t necessarily good for all • Move from point 1 to point 2 can be “bad news” when demand is inelastic P 1 3 2 D1 D2 bu. KC #2 Hard Winter Wheat = $6.15/bu In Jan ’09 but was at a record $10/bu in Feb ‘08. In 2005, the same bushel sold for $4.00/bu.

Agricultural Markets & Risks • Price risk (can be hedged) • Marketing risk(part of price risk) • Weather and pest-related risks • Lean years and rich years • Mis-timing of revenue and expenses • Difficulty of forming marketing granges to restrict quantity • SO: the solution is get the Government to intervene • Farmers are never happy - too sunny, too cloudy, etc. • Neither are teachers! • Perfectly competitive, we’d suppose • Price takers with thousands of farmers • Yet government intervenes in ag-markets • Historically, the improvements in seed and agricultural methods increased supply • Demand grew less dramatically

The Dynamics of Corn & Soybeans • Suppose both corn and soybeans are used to make vegetable oil. • If foreign demand for US corn declines, corn prices decline. This is partial equilibrium. • In general equilibrium, if one market has a shock, it spills over on the other market. • Lower corn prices leads to changes (reverberations) in supply of corn, supply of soybeans, and the equilibrium price of soybean • Ethanol mandates raise corn prices, but other crops too. Why?

Political Action • Policies that raise the price of wheat • Help farmers • Hurt everyone else • Farmers are helped a lot by price supports • Everyone else hurt a little. • GENERAL RULE: the small grouped helped a lot will organize for their benefit, whereas the silent majority does nothing about the hurt to them • US Senate was designed to help farmers • It has led to a bias in favor of more farmer-protection laws than was good for our economy

An S&D way to view Farm Supports S’ S • Regulation to set price at P1, a price floor • At point 1, Farmers helped some, but prefer 2, 3, or 4 below • Reward supply reduction • Land Bank (at point 1) • Reward purchases to add demand • Food stamps for food • at point 3 • Buy up the excess • Costly storage (purchase the difference of amount supplied and demanded at P1) 1 2 3 P1 D’ Pe D QD QE QS

Longer Run Consequencesof Farm Aid • Price supports reduces the risks of farming • We encourage expansion of existing farms, worsening the problem of excess supply • The myth of the farming as idyllic, something that MUST be preserved • International subsidies compete, as each nation rewards its own farmers leading to worldwide glut of crops

Agricultural Policy and Analysis of Governmental Failure • Milton Friedman: “Thank God, we don’t get all the government we pay for.” • Economists love to tinker with social policies, sometimes for good, often for ill • Policies are the realm of ‘welfare economics,’ that is, What is best for society as a whole? • Must recognize a problem • Have the will to do something about it • And have the ability to improve the situation, not just mess it up

Normative Economics • Can make statements of what “ought to be” • Taking from Peter to pay Paul can also be justified on an ‘efficiency criterion’ that the gains outweigh the losses. • What action is best overall? • Line up the pros and cons, or benefits & costs • Willingness to pay shows the strength of one’s preferences • On Iraq: Pro-war demonstrators and anti-war demonstrators show their resolve in the snow and rain

Vilfredo Pareto-“Pareto Optimal” • Actions that help some without hurting anyone should be undertaken • Policies can be Pareto improvements, if some are helped without harming others • The Problem of Envy, however, makes even this hard to accomplish • Would helping agriculture be Pareto Optimal? • Who is helped and who hurt? • Is removing price supports Pareto Optimal? 1848-1923